Traditional bank financing has a ceiling, and most serious investors hit it faster than they expect. Tightening debt-service coverage requirements, slow approval timelines, and rigid underwriting criteria make it nearly impossible to scale beyond a handful of properties through conventional channels alone. If you want to truly expand your real estate portfolio with private capital, you need a different playbook. This guide breaks down exactly how private capital works, how to structure your growth strategy around it, and how to execute deals that compound your portfolio over time.

Table of Contents

- Key takeaways

- Expand your real estate portfolio with private capital

- Building a diversified portfolio expansion strategy

- Executing deals: sourcing, evaluating, and investing

- Scaling and managing your portfolio over time

- My honest take on private capital and portfolio growth

- How Gannlending can accelerate your next acquisition

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Private capital fills the gap | When bank financing stalls, private equity, mezzanine debt, and preferred equity layers unlock deals that traditional lenders won't touch. |

| Diversification is non-negotiable | Spreading capital across sponsors, property types, and geographies protects against localized downturns and operator risk. |

| Liquidity planning determines success | Aligning your cash flow needs with fund timelines prevents costly early redemptions and forced sales. |

| Reinvestment discipline compounds growth | Spending distributions slows portfolio growth; reinvesting them over a decade can build a $10M portfolio from $500K. |

| Speed matters in deal execution | Fast-close private lending solutions let you capture time-sensitive acquisitions that slow conventional financing would cause you to miss. |

Expand your real estate portfolio with private capital

The phrase "private capital" covers a lot of ground, and understanding what it actually means in a real estate context is the first step toward using it effectively. At its core, private capital refers to funding that comes from non-bank sources: private equity firms, family offices, high-net-worth individuals, private debt funds, and syndication networks. These sources operate outside the regulatory constraints of traditional lenders, which means they can move faster, accept more complex deal structures, and fund assets that banks simply won't consider.

The capital stack is where this gets practical. A typical commercial real estate deal layers senior debt at 60 to 75% of the capital structure, mezzanine debt at 15 to 20%, preferred equity at 5 to 10%, and common equity at 10 to 25%. Each layer carries a different cost and return expectation. Senior debt is cheapest because it has first claim on assets. Mezzanine and preferred equity fill the gap between what a bank will lend and what the deal actually requires. Common equity sits at the bottom of the stack and demands the highest internal rate of return because it absorbs losses first.

Private capital most often enters at the mezzanine, preferred equity, or common equity layers. This is where you as an investor have the most flexibility to increase real estate investments without being constrained by a bank's loan-to-value limits. Understanding which layer you are investing in, or raising capital for, determines your risk exposure, your return expectations, and your liquidity timeline.

The main private capital vehicles you will encounter include:

- Syndications: A lead sponsor acquires a property and raises equity from passive investors. You receive a share of cash flow and appreciation without managing the asset.

- Private equity real estate funds: Pooled vehicles that deploy capital across multiple assets. Closed-end funds typically run 7 to 10 years; open-end or evergreen funds offer periodic redemption windows.

- Joint ventures: Two or more parties co-invest in a specific deal, sharing both equity and decision-making authority. This is common in larger acquisitions.

- Preferred equity and mezzanine positions: Debt-like instruments that sit above common equity in the stack, offering fixed or preferred returns with less upside but stronger downside protection.

Pro Tip: When evaluating which private capital vehicle fits your goals, map your personal liquidity needs against the vehicle's exit timeline before committing. A mismatch here is one of the most common and expensive mistakes investors make.

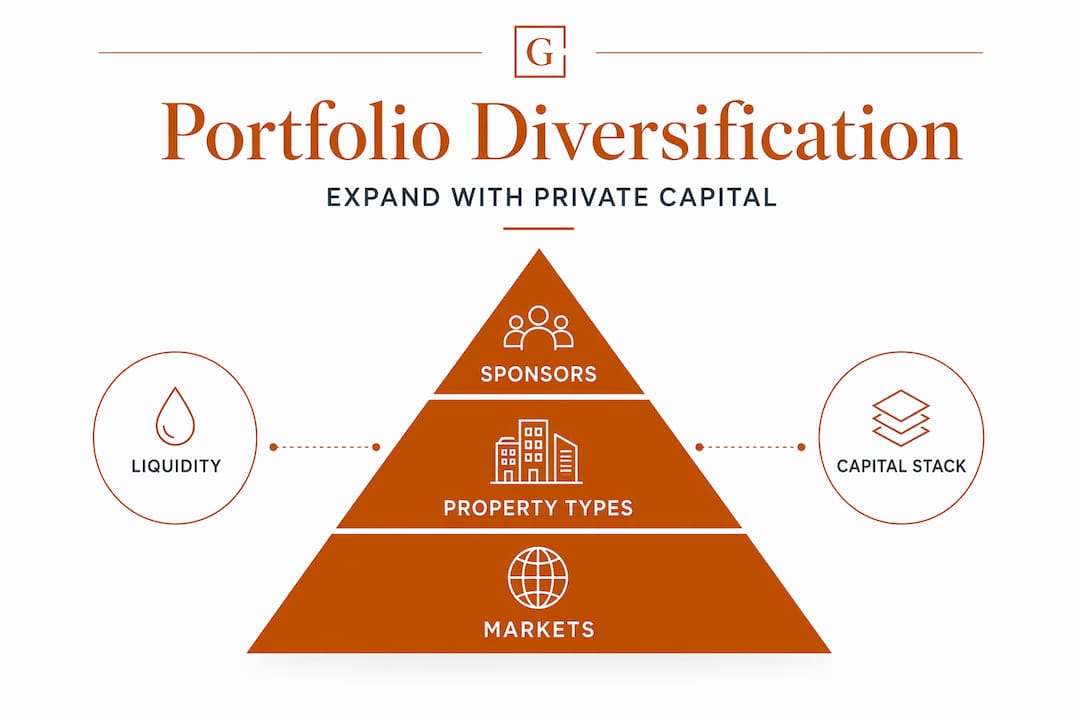

Building a diversified portfolio expansion strategy

Knowing what private capital is matters far less than knowing how to deploy it systematically. The investors who build durable portfolios don't just chase the next deal. They build a framework that governs how capital gets allocated, when it gets reinvested, and what concentration limits they will not cross.

Disciplined syndication investing can build a $10M real estate portfolio over 10 to 15 years starting with $500K to $1M in initial capital. The math only works if you diversify across sponsors, property types, and geographies, and if you reinvest distributions rather than spending them. That second part is where most investors fall short.

Here is how to structure a resilient diversification plan:

| Dimension | What to diversify | Why it matters |

|---|---|---|

| Sponsors | Invest across 4 to 6 operators with different specializations | Reduces single-operator risk and exposes you to different deal sourcing networks |

| Property types | Mix multifamily, industrial, medical office, and retail | Different asset classes perform differently across economic cycles |

| Geographies | Spread across 3 to 5 metro markets | Protects against regional downturns, regulatory changes, and local vacancy spikes |

| Capital stack position | Hold both equity and debt positions | Balances upside potential with downside protection |

Liquidity planning deserves its own attention. Private real estate funds often follow a buy-hold-liquidate lifecycle with fundraising periods of 4 to 5 years and hold phases around 10 years. If you commit capital to a closed-end fund and then need liquidity in year three, you are either paying redemption fees or selling at a discount in a secondary market. Neither is a good outcome.

The fix is simple in theory but requires discipline in practice. Before committing to any vehicle, map out your expected cash needs for the next 5 to 7 years. Keep a portion of your capital in semi-liquid vehicles or shorter-duration deals so you are never forced to exit a long-term position early.

Pro Tip: The middle years of a syndication investment, roughly years 4 through 10, are when discipline is tested hardest. Distributions start flowing and the temptation to spend rather than reinvest is real. Reinvesting those distributions is what separates investors who reach $10M from those who plateau at $3M.

Executing deals: sourcing, evaluating, and investing

Finding the right private capital deals is not about having access to a deal platform. It is about knowing what to look for and what to walk away from. The execution phase is where strategy meets reality, and the investors who scale successfully are the ones who build repeatable due diligence processes.

There are three primary ways to source private capital opportunities:

- Sponsor networks: Build relationships with 4 to 6 operators who specialize in specific asset classes. Quality sponsors send deals to investors they know first. Relationship-building here is not optional.

- Private real estate platforms: Digital platforms now offer accredited investors access to diversified real estate exposure. Heron Finance's 2026 platform launch gives investors exposure to 70-plus assets across three funds on a single interface, showing how accessible private real estate has become.

- Direct joint ventures: For investors with operational experience, co-investing directly with a sponsor on a specific deal gives you more control and often better economics than a pooled fund.

When evaluating any deal, your due diligence checklist should cover these areas:

- Sponsor track record: How many deals has this operator completed? What were the actual returns versus projected returns? Have they navigated a downturn?

- Deal structure and capital stack: Where does your capital sit? What are the waterfall mechanics? Who gets paid first in a downside scenario?

- Legal documentation: A properly structured private capital deal requires at least 11 core documents, including a private placement memorandum, limited partnership agreement, subscription agreement, and Form D filing. Missing or sloppy documentation is a red flag, not a minor detail.

- Market and asset fundamentals: Vacancy rates, rent growth trends, comparable sales, and local demand drivers should all support the underwriting assumptions.

- Exit timeline and return expectations: Does the projected IRR match the risk you are taking? A 12% preferred return in a mezzanine position is very different from a 12% projected IRR in a common equity deal.

The scale of private capital deployment at the institutional level shows where the market is heading. Realty Income raised its 2026 investment target to $9.5B, expanding private capital efforts through joint ventures and funds totaling nearly $2.7B. Individual investors who understand how to use the same tools at a smaller scale have a significant edge.

Scaling and managing your portfolio over time

Getting into private capital deals is the first challenge. Scaling a portfolio systematically over years is the harder, longer work. Most investors who plateau do so not because they ran out of deal flow, but because they lost discipline in how they managed concentration risk, reinvestment timing, and capital call obligations.

A few principles that separate investors who scale from those who stall:

- Monitor concentration regularly. If one sponsor, one market, or one asset class represents more than 30% of your total portfolio, you are exposed to concentrated risk. Rebalance by directing new capital toward underweight areas rather than selling existing positions.

- Understand capital call mechanics. Many private funds have the right to call additional capital from investors during the investment period. If you are not prepared for a capital call, you may face penalties or dilution. Always reserve 10 to 15% of your committed capital as a buffer.

- Adjust your capital stack as the portfolio grows. Higher LTV senior and whole loan solutions combined with mezzanine or preferred equity layers are increasingly used in 2026 to fill leverage gaps that bank financing leaves open. As your portfolio grows, engineering the capital stack on individual deals becomes a lever for accessing larger acquisitions without proportionally more equity.

- Track the fund lifecycle. Closed-end funds move through distinct phases: fundraising, deployment, management, and liquidation. Knowing where each of your fund investments sits in that cycle helps you anticipate when capital will be returned and when you can redeploy it.

Operator specialization matters enormously at scale. Kayne Anderson's $5.12B oversubscribed fund in 2026 targeted specific sectors like medical office, seniors housing, and industrial, not a generic mix of everything. The lesson for individual investors is the same: depth of expertise in specific sectors beats shallow exposure to all of them.

My honest take on private capital and portfolio growth

I've watched a lot of investors approach private capital the same way they approached their first rental property: with too much optimism and not enough structure. The assumption is that more capital access automatically means more portfolio growth. It doesn't.

What I've found is that the investors who actually scale are the ones who treat liquidity planning as seriously as deal selection. You can have a perfectly structured capital stack and a great sponsor, but if your cash flow doesn't support a capital call in year two, that deal becomes a liability. I've seen investors forced to sell positions at a loss not because the deal was bad, but because they didn't plan for the timing.

The other thing I'd push back on is the idea that diversification means spreading thin. In my experience, having deep relationships with two or three specialized operators outperforms having shallow exposure to ten. You get better deal access, better communication when things go sideways, and better alignment on exit timing. The discipline of reinvesting distributions rather than spending them is the single biggest differentiator I've seen in investors who reach meaningful portfolio scale versus those who stay stuck.

Private capital is a tool. Like any tool, it rewards the people who understand it deeply and punishes those who use it carelessly.

— Brian

How Gannlending can accelerate your next acquisition

When a deal moves fast, your financing has to move faster. That's where Gannlending delivers something traditional lenders simply can't match. Gannlending specializes in hard money loans built specifically for real estate investors who need capital in days, not months.

With funding in as few as 5 to 7 business days, no appraisal required, and financing up to 75% LTV across residential and commercial properties, Gannlending removes the bottleneck that causes most investors to lose deals to better-capitalized buyers. With over $50 million funded, Gannlending has the track record to back up the speed. Whether you are acquiring your next investment property, protecting an asset from foreclosure, or executing a time-sensitive joint venture, Gannlending gives you the private capital access to act when it counts. Visit gannlending.com to get started.

FAQ

What is private capital in real estate investing?

Private capital in real estate refers to funding from non-bank sources such as private equity firms, family offices, syndications, and private debt funds. It fills the financing gap that traditional lenders leave open, especially for complex or time-sensitive deals.

How do I diversify a real estate portfolio using private capital?

Spread capital across multiple sponsors, property types, and geographic markets while holding positions in different capital stack layers. Diversifying across sponsors and geographies reduces concentration risk and improves long-term compounding potential.

What documents are required for a private real estate capital raise?

A properly structured raise requires at least 11 core documents, including a private placement memorandum, limited partnership agreement, subscription agreement, and a Form D filing with the SEC within days of the first investor commitment.

How long is capital typically locked up in private real estate funds?

Private real estate funds typically follow a buy-hold-liquidate lifecycle with fundraising periods of 4 to 5 years and hold phases of around 10 years. Early redemptions often trigger fees or secondary market discounts.

How fast can I close a deal using private hard money lending?

With a lender like Gannlending, hard money loans can close in as few as 5 to 7 business days, with no appraisal required and financing up to 75% LTV. This speed makes private lending the go-to option for time-sensitive acquisitions.