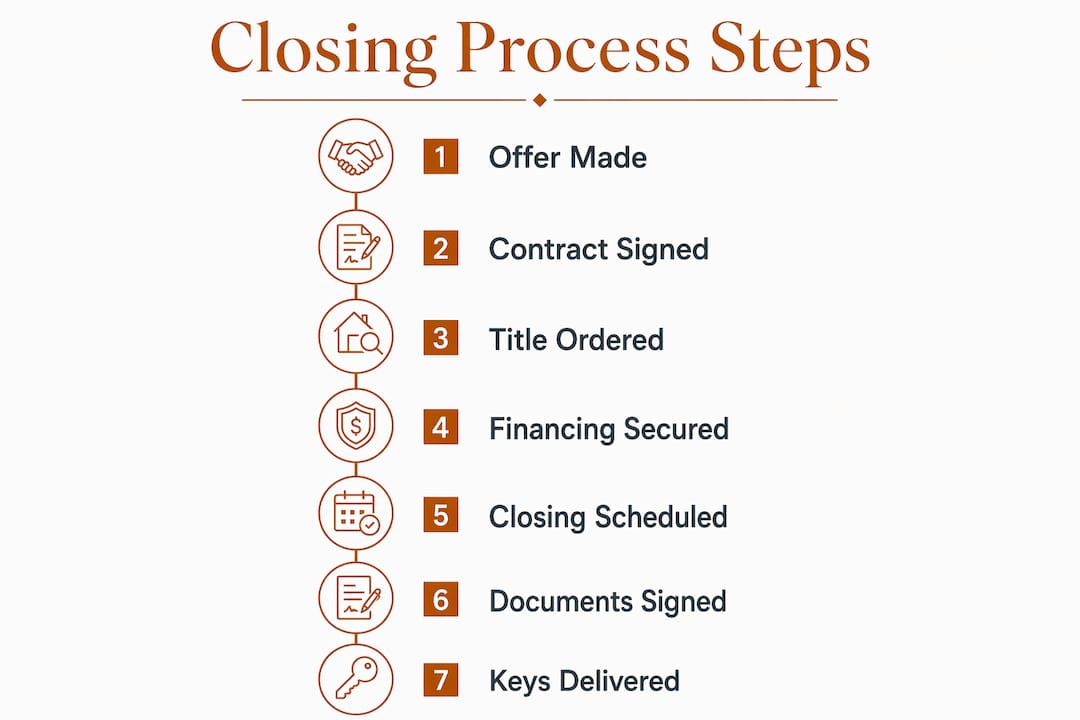

Closing a real estate deal fast is defined as completing the full transaction process, from contract execution to funded settlement, in significantly less time than the conventional 40 to 45 days that traditional mortgage closings typically require. For investors competing in foreclosure auctions, bidding wars, or time-sensitive acquisitions, the difference between a 14-day close and a 45-day close can mean the difference between winning a deal and losing it entirely. Federal regulations, specifically the TRID rule requiring a mandatory 3-business-day Closing Disclosure review period, set a hard floor on how fast any financed deal can close. Understanding that floor, and building your process around it, is the foundation of every fast closing strategy covered in this guide.

What are the critical factors that affect real estate deal closing speed?

Speed in real estate closings is not random. Specific, identifiable bottlenecks determine whether your deal closes in two weeks or two months, and most of them are controllable.

The single most misunderstood constraint is regulatory. The TRID rule, formally known as the TILA-RESPA Integrated Disclosure rule, mandates that buyers receive their Closing Disclosure at least 3 business days before consummation. This is a hard legal minimum. No amount of preparation eliminates it. If the lender issues a revised disclosure due to a rate change, fee adjustment, or loan product switch, the three-day clock resets entirely. That single error can push a closing back by a week.

Beyond regulation, the following factors most directly control your timeline:

- Financing type. Cash purchases can close in 7 to 14 days because they skip mortgage underwriting and appraisal contingencies entirely. Conventional loans average 40 to 45 days. FHA and VA loans often run longer.

- Title search and survey. Title companies need time to research ownership history, liens, and encumbrances. Ordering this work the moment a contract is signed compresses the timeline. Waiting even 48 hours costs you days.

- HOA and condo estoppel letters. In states like Florida, HOA estoppel letters can legally take up to 15 business days to deliver. That is three calendar weeks. If you request them late, you cannot close on time regardless of everything else being ready.

- Inspection and appraisal contingencies. Both require scheduling, completion, and review. Appraisals ordered late or returning below contract price trigger renegotiation cycles that add weeks.

- Buyer financial readiness. Closing costs typically run 3% to 6% of the loan amount. Buyers who have not confirmed their cash-to-close figure in advance often scramble at the last minute, delaying funding.

The pattern across all these factors is the same: delays are almost always caused by late starts, not by the tasks themselves being slow.

How can buyers use financing options to close a deal faster?

Financing choice is the single largest lever buyers control when trying to speed up real estate closing. The right financing structure can cut weeks off your timeline before you even sign a contract.

Cash is the fastest option by a wide margin. Without a lender involved, there is no underwriting, no appraisal requirement, and no Closing Disclosure waiting period. A well-organized cash buyer working with a responsive title company can close in under two weeks. Cash offers also carry negotiating power. Sellers frequently accept slightly lower prices from cash buyers because the certainty and speed of closing has real financial value to them. That is a concrete trade-off worth calculating before you make your offer.

For buyers who need financing, the gap between a prepared borrower and an unprepared one is enormous. Pre-underwriting, which is different from standard pre-approval, means the lender has already verified income, assets, employment, and credit before you find a property. When you go under contract, the underwriter only needs to approve the specific asset. Programs like Gustan Cho's 21-day loan program use this front-loaded approach to deliver conditional approvals before contract signing, compressing post-contract processing to days rather than weeks.

Pro Tip: Get pre-underwritten, not just pre-approved, before you start making offers. Standard pre-approval is a credit check and income estimate. Pre-underwriting is a full file review. The difference in closing speed can be two to three weeks.

The trade-offs of fast financing routes are real and worth naming directly:

- Hard money and private lending carry higher interest rates than conventional loans, typically in the 9% to 13% range, but they fund in days rather than weeks.

- Waiving appraisal contingencies speeds the process but transfers valuation risk entirely to the buyer.

- Skipping inspection contingencies to accelerate closing exposes buyers to undisclosed property defects.

Speed and risk move together in real estate financing. The key is choosing the trade-off deliberately, not accidentally.

What operational steps should you take right after contract signing?

The contract signing date is not the finish line. It is the starting gun. Every hour you delay ordering third-party services after contract execution is an hour added to your closing date. Most buyers and even some agents treat the first few days after signing as administrative downtime. That is the single most common reason deals close late.

Here is the sequence that compresses timelines for buyers who want to close quickly:

- Order title work on Day 1. Contact your title company the same day the contract is executed. Starting title work immediately uncovers liens, ownership disputes, and encumbrances early, when there is still time to resolve them without delaying closing.

- Request HOA and condo estoppel letters at contract signing. Do not wait until week two. With a statutory window of up to 15 business days for responses, a Day 1 request means you might receive the letter by Day 15. A Day 7 request means you will not have it until Day 22 at the earliest.

- Submit the fully executed contract to escrow immediately. Title and escrow companies cannot open a file or begin work without a signed contract. Delays in submission are pure dead time.

- Schedule inspections within 24 to 48 hours. Most inspection contingency windows run 7 to 10 days. Booking on Day 1 or Day 2 leaves time to renegotiate or request repairs without blowing the contingency deadline.

- Confirm earnest money delivery on schedule. Late earnest money deposits are a breach of contract in most states and can give sellers grounds to cancel. Confirm the wire or check is delivered on the exact date specified in the contract.

- Run tasks in parallel, not in sequence. Title work, inspections, HOA letters, and lender document collection should all be happening simultaneously. Treating them as a sequential checklist adds weeks to your timeline.

Pro Tip: Create a shared task tracker, using a tool like Google Sheets or Notion, that lists every third-party deliverable with its deadline and the person responsible. Share it with your agent, title company, and lender on Day 1. Visibility prevents the "I thought you ordered that" conversations that kill closing timelines.

The most predictable closing delays are self-inflicted. Early submission of contracts, timely earnest money, and immediate title and HOA orders prevent the stalls that buyers later blame on the process.

What practical tips help speed up closing day execution?

Closing day itself rarely fails because of a single catastrophic problem. It fails because of accumulated small errors: a document missing a signature, a wire that arrived 30 minutes after the cutoff, a buyer who made a large purchase on credit the week before closing and triggered a re-underwrite.

The following practices protect your closing date once you are inside the final week:

- Review the Closing Disclosure the moment it arrives. You have three business days to review it, but reviewing it within the first hour lets you flag errors immediately. A corrected disclosure resets the three-day clock, so catching mistakes early is far better than catching them on Day 2.

- Freeze your financial profile. Do not open new credit accounts, make large purchases, change jobs, or move significant sums between accounts between contract signing and closing. Any of these can trigger a lender re-verification that delays funding.

- Use digital closing platforms where available. CrossCountry Mortgage's use of Blend Close technology with remote online notarization cut average signing appointments from roughly two hours to under 30 minutes. eNotes and electronic signatures eliminate the physical document courier delays that still plague traditional closings.

- Align schedules with the seller in advance. Confirm the closing time with all parties at least 72 hours out. Last-minute schedule conflicts on closing day are more common than they should be and can push funding past the lender's daily wire cutoff.

The Closing Disclosure 3-day rule is designed to protect buyers, not frustrate them. Treat it as a built-in review window, not a bureaucratic obstacle. Use those three days to verify every fee, confirm your cash-to-close figure, and prepare your wire transfer. Buyers who use this window well close on time. Buyers who ignore it scramble.

For investors handling quick property transactions across multiple deals simultaneously, building a standardized closing checklist and a reliable team of title, escrow, and lending professionals is the real multiplier. The process knowledge compounds across deals.

Key takeaways

Closing a real estate deal fast requires parallel task execution from Day 1, the right financing structure chosen before contract signing, and strict financial discipline through the final week.

| Point | Details |

|---|---|

| Regulatory floor is fixed | The 3-business-day Closing Disclosure rule cannot be waived; build your timeline around it, not against it. |

| Cash closes fastest | Cash purchases close in 7 to 14 days by eliminating underwriting, appraisal, and lender disclosure timelines. |

| Front-load all third-party orders | Order title, HOA estoppel letters, and inspections on Day 1 to prevent statutory wait times from extending your close. |

| Pre-underwriting beats pre-approval | Full pre-underwriting before contract signing can compress financed closings to 21 days or fewer. |

| Protect your financial profile | Any credit or financial change between signing and closing can trigger re-underwriting and reset your closing date. |

What I've learned about closing speed after watching hundreds of deals

Most buyers focus on the signing appointment as the closing event. After working through dozens of real estate transactions, I can tell you the signing appointment is almost never the problem. The deals that close late almost always trace back to a decision made in the first 72 hours after contract execution, specifically, what was not ordered, not submitted, or not confirmed.

The investors I have seen close deals in under two weeks share one habit: they treat Day 1 like a fire drill. Title order goes out within hours. HOA letters get requested before the ink is dry. Inspections are booked before the agent even sends the congratulations email. That front-loading is not urgency for its own sake. It is the only way to stay ahead of the statutory and regulatory timelines that nobody can compress.

Cash offers are underrated as a negotiating tool, not just a speed tool. I have watched buyers win deals at prices 5% to 8% below competing financed offers simply because the seller valued certainty. A cash offer's speed advantage is real, but its negotiating leverage is often worth even more than the time saved.

The honest caution I would add: technology is improving closing speed, but it is not eliminating the human coordination failures that cause most delays. Digital notarization and eNotes help. They do not fix a buyer who forgets to wire earnest money or a title company that gets a late contract submission. Process discipline still matters more than any platform.

— Brian

Close faster with Gannlending's private lending solutions

Real estate investors who need to close quickly cannot always wait 40 days for a conventional lender to catch up with the opportunity in front of them.

Gannlending specializes in hard money loans built specifically for investors who need speed and flexibility. With funding available in as few as 5 to 7 business days and no appraisal requirement, Gannlending removes two of the biggest timeline bottlenecks in financed deals. Financing covers up to 75% LTV across residential and commercial properties, and the approval process focuses on the asset rather than a paperwork marathon. Gannlending has funded over $50 million in deals, including time-sensitive foreclosure situations where conventional financing was simply not an option. If your next deal requires a fast close, explore your options with Gannlending before the opportunity moves on.

FAQ

How fast can you realistically close a real estate deal?

Cash buyers can close in 7 to 14 days. Financed buyers using pre-underwriting programs can close in as few as 21 days, though the mandatory 3-business-day Closing Disclosure review period applies to all financed transactions regardless of preparation.

What is the biggest cause of closing delays?

Most closing delays are operational, not regulatory. Late title orders, delayed HOA estoppel requests, and slow earnest money delivery are the most common causes, all of which are preventable with Day 1 action after contract signing.

Does a cash offer always close faster than a financed offer?

Yes, in nearly every case. Cash purchases skip mortgage underwriting, appraisal contingencies, and the lender-triggered Closing Disclosure waiting period, which together account for the majority of time in a conventional closing timeline.

What is the Closing Disclosure 3-day rule and can it be waived?

The Closing Disclosure must be delivered to the buyer at least 3 business days before closing under federal TRID rules. It cannot be waived. If the disclosure is revised due to fee or rate changes, the three-day clock resets from the date of the new disclosure.

How does pre-underwriting differ from pre-approval for closing speed?

Pre-approval is a preliminary credit and income check. Pre-underwriting is a full file review completed before a property is identified, meaning the lender only needs to approve the specific asset after contract signing. This can cut post-contract processing from several weeks to just days.