Preferred equity in real estate sits in a category that trips up even experienced investors. It looks like debt. It pays like debt. But legally, it is equity. Understanding what is preferred equity real estate financing actually means can change how you structure deals, evaluate risk, and allocate capital across a project. Whether you are a sponsor trying to fill a funding gap or an investor weighing yield against protection, this guide cuts through the confusion and gives you the full picture on how preferred equity works, where it fits, and when it makes sense.

Table of Contents

- Key takeaways

- What is preferred equity in real estate?

- How preferred equity works in real estate deals

- Legal rights and enforcement in default scenarios

- Tax considerations for preferred equity investors

- When to use preferred equity in your financing strategy

- My honest take on preferred equity

- Fast capital for real estate investors

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Hybrid capital position | Preferred equity sits above common equity but below all debt in the capital stack, combining features of both. |

| No creditor rights | Preferred equity investors hold membership interests, not secured claims, so foreclosure is not an available remedy. |

| Priority returns | Investors receive preferred returns before common equity holders, typically ranging from 10% to 14% annually. |

| Tax complexity | Phantom income and guaranteed payment treatment can create tax liability even when no cash is distributed. |

| Contract-driven protections | Investor rights depend entirely on the operating agreement, making due diligence on legal documents non-negotiable. |

What is preferred equity in real estate?

The preferred equity definition starts with its position in the capital stack. It is an ownership interest in the entity that owns the property, typically a joint venture LLC or limited partnership, not a direct loan secured by the asset itself. That distinction matters more than most investors initially realize.

In a standard real estate deal, the capital stack runs from senior debt at the bottom (most protected) up through mezzanine debt, then preferred equity, and finally common equity at the top (least protected, most upside). Preferred equity investors receive priority returns before common equity holders, but they take on considerably more risk than senior lenders because they hold no lien on the property.

Here is how the four main layers compare:

| Capital layer | Security | Return type | Risk level |

|---|---|---|---|

| Senior debt | First lien on property | Fixed interest | Lowest |

| Mezzanine debt | Pledge of equity interests | Fixed interest | Moderate |

| Preferred equity | Membership interest, no lien | Preferred return | High |

| Common equity | Residual ownership | Profit participation | Highest |

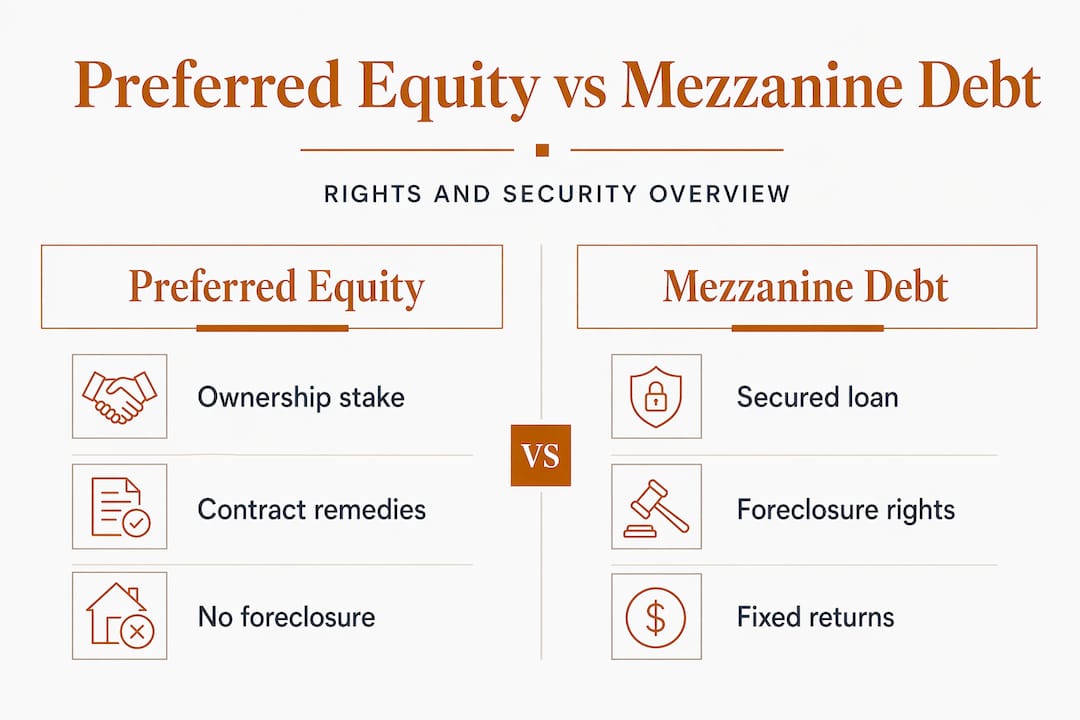

The core difference between preferred equity and mezzanine debt is enforcement power. A mezzanine lender can foreclose on the borrower's equity interest in a UCC sale if there is a default. A preferred equity investor lacks those creditor rights and must rely on contractual remedies written into the operating agreement. That is not a small distinction in a distressed scenario.

How preferred equity works in real estate deals

Most development projects, particularly multifamily, face a predictable financing gap. Senior debt covers roughly 60% to 70% of total project costs. Sponsors rarely have enough equity to fund the rest themselves. Preferred equity fills that funding gap, with preferred returns typically ranging from 10% to 14% annually, depending on deal risk and market conditions.

Here is how a typical structure plays out in practice:

- Senior lender funds 65% of project costs through a construction loan secured by a first mortgage on the property.

- Preferred equity investor contributes 15% to 20% in exchange for a membership interest in the JV LLC, with priority economic rights over the sponsor's common equity.

- Sponsor contributes the remaining equity, retaining common equity and operational control of the project.

- Preferred equity investor receives distributions first, up to the agreed preferred return rate, before the sponsor sees a dollar of profit.

- Liquidation preference applies if the property is sold or refinanced, giving the preferred equity investor priority recovery of their capital before common equity participates.

Pro Tip: When reviewing a preferred equity term sheet, pay close attention to whether the preferred return is cumulative or non-cumulative. A cumulative preferred return accrues if unpaid and must be satisfied before any common equity distributions. Non-cumulative returns do not carry over, which shifts risk significantly toward the investor.

Using preferred equity allows sponsors to complete capital stacks without giving up controlling interests or diluting their economics through co-general partner structures. For sponsors with strong projected returns, layering preferred equity beneath their common equity position preserves upside while solving the funding gap.

Legal rights and enforcement in default scenarios

This is where preferred equity's hybrid nature gets complicated, and where many investors get burned by assumptions they should not have made.

Preferred equity is economically debt-like with fixed returns and priority distributions, but it carries none of the creditor status that protects lenders in distress. No foreclosure. No acceleration. No lien to enforce. If a sponsor defaults on their obligations to a preferred equity investor, the remedies available are entirely contractual.

What preferred equity investors typically have available after a default:

- Rate step-ups: The preferred return rate increases automatically upon default, adding financial pressure on the sponsor.

- Enhanced governance rights: Investors may gain the ability to remove the sponsor or take over management decisions.

- Blocking rights: Preferred equity holders can veto major decisions like refinancing, additional borrowing, or asset sales.

- Forced buyout provisions: Some agreements require the sponsor to buy out the preferred equity position at a defined price.

Preferred equity holders' influence over sponsors arises contractually rather than through creditor protections. The quality of that contract is everything. A poorly drafted operating agreement can leave an investor with theoretical rights and no practical way to enforce them.

In bankruptcy, the gap between preferred equity and mezzanine debt becomes even more pronounced. Preferred equity holders remain junior to all debt holders in a restructuring. A mezzanine lender can foreclose on the equity pledge and take control of the asset before bankruptcy proceedings even begin. A preferred equity investor is waiting in line behind every creditor in the capital stack.

The practical takeaway: due diligence on contractual remedies after a default is not optional. The operating agreement, the LLC agreement, and any side letters define your actual position. Assumptions about secured claims will not protect you.

Tax considerations for preferred equity investors

The tax treatment of preferred equity investing surprises a lot of investors who expect it to behave like a debt instrument. It does not.

Preferred equity investors can face phantom income and guaranteed payment taxation even when they have not received any cash distributions. In a partnership structure, if the preferred return is treated as a guaranteed payment, the investor owes ordinary income tax on that amount regardless of whether cash actually changed hands. That creates a real cash flow problem if the deal is not distributing.

Pro Tip: Before committing to a preferred equity investment, confirm whether the partnership agreement includes tax distribution provisions. These provisions require the entity to distribute enough cash to cover each investor's estimated tax liability on allocated income. Without them, you could owe taxes on income you never actually received.

The economic and tax outcomes diverge significantly depending on how preferred returns are structured. Cumulative preferred returns that accrue without cash payment create timing mismatches between taxable income and actual distributions. Non-cumulative structures may reduce phantom income exposure but shift economic risk to the investor.

Investors with tax-exempt status, like pension funds or certain endowments, face different considerations entirely. Unrelated business taxable income rules may apply, making preferred equity through a standard LLC structure a poor fit without additional structuring. Always review the partnership agreement with a tax advisor who knows real estate partnership taxation before signing.

When to use preferred equity in your financing strategy

Preferred equity is not the right tool for every deal. Knowing when it fits and when it does not is what separates disciplined capital allocation from expensive mistakes.

Situations where preferred equity makes strong strategic sense:

- Senior debt is maxed out and the sponsor needs additional capital without bringing in a co-GP who would dilute control and economics.

- The project has strong projected returns that can absorb the 10% to 14% cost of preferred equity and still deliver meaningful common equity upside.

- The sponsor has a track record that gives preferred equity investors confidence in execution and governance.

- Speed matters and the sponsor needs capital that can move faster than institutional equity processes typically allow.

Situations where preferred equity is likely a poor fit:

- Projected returns are thin and the preferred return cost will squeeze common equity to near zero, removing the sponsor's incentive to perform.

- The sponsor is unproven and lacks the operating history that justifies the governance risk preferred equity investors are taking.

- The deal structure is so complex that the operating agreement cannot adequately define enforcement rights and remedies.

Preferred equity terms are highly contract-dependent with no market standardization. Every term sheet is negotiated from scratch. Key features to scrutinize include the preferred return rate and accrual mechanics, liquidation preference structure, governance rights triggered by default, and any promote or profit participation provisions that affect total return.

The governing documents define economic seniority and investor protections, which makes reading every line of the operating agreement a non-negotiable part of the diligence process. Do not rely on summaries or term sheet representations alone.

My honest take on preferred equity

I have seen preferred equity pitched as a safe, debt-like alternative for investors who want yield without the volatility of common equity. That framing is incomplete, and in some cases, it is outright misleading.

The "debt-like" label creates a false sense of security. Yes, you get priority distributions. Yes, you have a liquidation preference. But when a deal goes sideways and the senior lender moves to protect their position, preferred equity investors discover very quickly that contractual rights and creditor rights are not the same thing. I have watched investors assume their governance protections would give them real leverage over a sponsor in distress, only to find that a poorly drafted operating agreement gave them the right to complain but not much else.

What actually protects preferred equity investors is the quality of the legal documents and the sponsor's track record. A well-structured operating agreement with clear default triggers, meaningful governance rights, and enforceable buyout provisions is worth more than any preferred return rate. Tax surprises are also real. Phantom income on a deal that is not yet distributing cash is a problem investors consistently underestimate until they get their K-1 in March.

My advice: treat preferred equity as its own asset class with its own risk framework. Do not map it onto debt assumptions or common equity assumptions. Understand exactly what your contractual remedies are before you commit, and make sure your tax advisor has reviewed the partnership structure. The returns can be compelling. The risks are real and specific.

— Brian

Fast capital for real estate investors

When you are structuring a deal and need capital that moves at the speed of real estate, Gannlending is built for exactly that scenario. Gann Private Lending provides hard money loans that close in as few as 5 to 7 business days, with no appraisal required and financing up to 75% LTV across residential and commercial properties. Whether you are filling a gap in your capital stack, protecting a property from foreclosure, or moving fast on an acquisition, Gann's asset-focused approval process cuts through the delays that sink deals. With over $50 million funded, Gannlending is a proven partner for investors who cannot afford to wait on traditional lender timelines.

FAQ

What is preferred equity in real estate?

Preferred equity is an ownership interest in the entity that holds a real estate asset, sitting above common equity but below all debt in the capital stack. Investors receive priority distributions and liquidation preferences but hold no lien on the property itself.

How does preferred equity differ from mezzanine debt?

Mezzanine debt is a secured loan with foreclosure rights over the borrower's equity interests, while preferred equity is a membership interest with only contractual remedies available in a default. That enforcement gap makes preferred equity riskier in distress scenarios.

What returns do preferred equity investors typically earn?

Preferred equity investors typically earn preferred returns in the range of 10% to 14% annually in multifamily development deals, with distributions paid before any common equity profits are distributed to the sponsor.

What are the tax risks of investing in preferred equity?

Preferred equity investors can owe taxes on phantom income and guaranteed payments even when no cash has been distributed, making tax distribution provisions in the partnership agreement a critical term to negotiate before investing.

When does it make sense to use preferred equity?

Preferred equity works best when senior debt is maxed out, the deal's projected returns can absorb the cost, and the sponsor has a strong enough track record to justify the governance risk that preferred equity investors are accepting.