A commercial rental property is real estate leased for business use rather than private residence, with the primary purpose of generating income through rent or capital appreciation. The term covers everything from a downtown office tower to a neighborhood strip mall to a 20-unit apartment complex. Understanding the commercial real estate definition matters whether you are a first-time investor evaluating your first acquisition or a business owner deciding whether to lease or own your space. The key distinction is use, not form. A building that looks residential can be classified as commercial if it houses five or more units or operates under a commercial lease.

What is a commercial rental property and how is it classified?

A commercial rental property is any income-producing real estate leased to business tenants or used for commercial operations, as opposed to owner-occupied residential housing. The industry term is commercial real estate, often abbreviated as CRE. Both terms refer to the same asset class, and you will encounter them interchangeably in loan documents, lease agreements, and investment prospectuses.

The classification hinges on intended use, not physical appearance. A converted Victorian house operating as a law office is commercial real estate. A glass skyscraper divided into condominiums is residential. Local zoning codes formalize this distinction by designating permitted uses for each parcel of land, and those designations directly affect what financing you can access and what lease structures apply.

Multifamily buildings with more than four units are classified as commercial properties for borrowing and tax purposes, which separates them from smaller residential rentals. This matters practically: a duplex and a six-unit apartment building look similar on the street but are financed, appraised, and leased under entirely different frameworks.

Pro Tip: When evaluating any property, pull the zoning certificate before you analyze the financials. A property operating outside its permitted zoning classification can face forced closure, which destroys cash flow overnight.

What types of properties qualify as commercial rentals?

Commercial real estate covers four major asset types: office, retail, industrial, and multifamily residential. Each behaves differently in terms of lease length, tenant profile, and economic sensitivity. Knowing the differences helps you match the right property type to your investment goals.

- Office: Ranges from Class A skyscrapers in central business districts to suburban professional parks and small medical suites. Office leases tend to run three to ten years, and tenant creditworthiness varies widely from Fortune 500 anchor tenants to solo practitioners.

- Retail: Includes regional malls, neighborhood strip centers, standalone pad sites, and power centers anchored by national chains. Retail performance ties closely to consumer foot traffic and local economic conditions, making location the single most critical underwriting variable.

- Industrial: Warehouses, distribution centers, manufacturing plants, and flex spaces. Industrial has been one of the strongest-performing CRE sectors in recent years, driven by e-commerce demand for last-mile logistics space.

- Multifamily (5+ units): Apartment complexes above four units cross into commercial territory. They offer more predictable cash flow than other CRE types because residential demand remains relatively stable even during economic downturns.

- Mixed-use and specialty: Properties combining retail, office, and residential floors in a single building. Specialty categories include self-storage facilities, medical office buildings, hospitality assets like hotels, and data centers.

Understanding essential real estate investment terms before you commit to any asset class will save you from costly misunderstandings in due diligence.

How do commercial leases differ from residential leases?

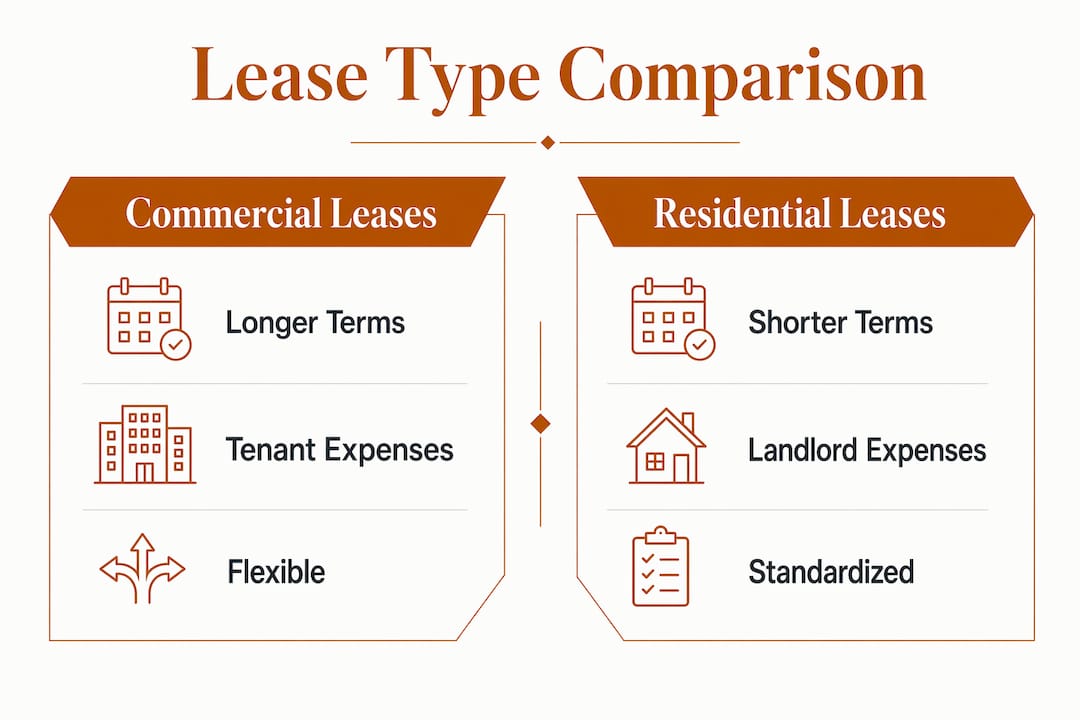

Commercial lease agreements are structurally different from residential leases in three critical ways: term length, expense allocation, and negotiation flexibility. Residential leases typically run one year with standardized state-mandated terms. Commercial leases commonly run three to ten or more years and are negotiated individually, meaning no two deals are identical.

The most consequential difference is how operating expenses get divided between landlord and tenant. There are four primary lease structures you need to know:

| Lease type | Who pays operating expenses |

|---|---|

| Gross lease | Landlord covers taxes, insurance, and maintenance; tenant pays flat rent |

| Net lease | Tenant pays base rent plus some operating costs (taxes, insurance, or maintenance) |

| Triple net (NNN) | Tenant pays base rent plus all three: taxes, insurance, and maintenance |

| Modified gross | Costs are split by negotiation; hybrid of gross and net |

Net leases shift operating expense risk to tenants, which gives landlords more predictable cash flow but requires tenants to budget carefully for variable costs. A triple net lease on a single-tenant retail building occupied by a national pharmacy chain, for example, can function almost like a bond: fixed income with minimal landlord obligations.

The critical lesson from lease expense allocation is that the headline rent number tells you very little. Two leases at $25 per square foot can produce dramatically different net income depending on whether the landlord or tenant absorbs property taxes and common area maintenance. Always model the net operating income, not the gross rent.

Pro Tip: Negotiate a rent escalation clause into every commercial lease you sign as a landlord. A 2% to 3% annual increase protects your purchasing power over a ten-year term without triggering tenant resistance at renewal.

What should investors know about financing and managing commercial rentals?

Financing a commercial rental property works differently from buying a single-family home, and the options available to you depend heavily on the asset type, your experience level, and how quickly you need to close.

- Direct ownership with a commercial mortgage: Traditional bank loans for CRE typically require 25% to 35% down, strong debt service coverage ratios, and extensive documentation. Approval timelines run 45 to 90 days, which can cost you a deal in a competitive market.

- Hard money and private lending: Asset-based lenders like Gannlending focus on the property value rather than borrower paperwork. Funding can close in five to seven business days, which is decisive when you are competing for off-market deals or need to act before a foreclosure deadline.

- Real estate investment trusts (REITs): Publicly traded REITs let you invest in commercial real estate without direct ownership. They offer liquidity but remove your control over lease terms and property management decisions.

- Syndications and private equity: Pooling capital with other investors through a syndication structure lets you access larger assets. Returns depend on the sponsor's underwriting discipline and the quality of the underlying leases.

Investment value depends on cash flow stability, lease structures, occupancy, and tenant creditworthiness. A fully leased industrial building with a ten-year NNN lease to a publicly rated logistics company is worth far more than the same building with month-to-month tenants, even if the square footage and location are identical.

Tenant quality and lease length strongly influence valuation and your ability to refinance. Lenders underwrite the income stream, not just the bricks. If your anchor tenant vacates, your property value and your loan terms can both deteriorate simultaneously.

Pro Tip: Build a three-month operating reserve before you close on any commercial property. Vacancy periods between tenants, roof repairs, and HVAC replacements arrive without warning, and running out of cash forces you into distressed refinancing at the worst possible moment.

How do zoning and regulatory classifications affect commercial rentals?

Zoning is the legal framework that determines what a property can be used for, and it directly controls whether a building qualifies as a commercial rental property. Local authorities use zoning to enforce land use designations, and those designations affect financing options, permitted tenant types, and legal compliance obligations.

Here is what zoning means in practice for investors and tenants:

- Permitted use restrictions: A property zoned C-1 (neighborhood commercial) may allow a coffee shop but prohibit a manufacturing operation. Placing the wrong tenant in a space can trigger code violations and lease termination.

- Financing implications: Lenders classify loans based on zoning, not just physical use. A building zoned residential but operating as a short-term rental business may not qualify for commercial financing, leaving you with fewer and more expensive options.

- Mixed-use complexity: Mixed-use buildings require careful evaluation to confirm which portions qualify under commercial use definitions. A building with retail on the ground floor and apartments above may carry split financing requirements.

- Variance and rezoning risk: If you acquire a property based on a current use that depends on a variance rather than base zoning, that variance can be revoked. Always verify that the intended use is permitted by right, not by exception.

- Tax and depreciation treatment: Commercial zoning affects how the IRS classifies your property for depreciation purposes. Residential rental property depreciates over 27.5 years; commercial property depreciates over 39 years. That difference compounds meaningfully over a long hold period.

Pairing zoning research with a commercial property loan calculator helps you model the real cost of financing before you commit to an acquisition.

Key takeaways

Commercial rental property investing rewards investors who understand lease structures, tenant quality, and zoning before they write a check.

| Point | Details |

|---|---|

| Use defines classification | A property is commercial based on its intended use and zoning, not its physical form. |

| Lease structure drives returns | Gross, net, and triple net leases allocate expenses differently, directly affecting net operating income. |

| Tenant quality is the core asset | Creditworthy tenants on long leases produce stable cash flow and support higher valuations. |

| Zoning controls your options | Permitted use designations affect financing, tenant eligibility, and tax treatment simultaneously. |

| Financing speed matters | Hard money lenders can close in five to seven days, giving investors a real edge in competitive markets. |

Why most investors underestimate the lease before they buy

After working with real estate investors across dozens of commercial transactions, the single most consistent mistake I see is treating the lease as a formality rather than the actual product being purchased. When you buy a commercial rental property, you are not buying a building. You are buying a cash flow stream secured by a building. The lease is the instrument that defines that stream.

I have reviewed deals where investors focused entirely on cap rate and price per square foot while glossing over expense reconciliation clauses buried on page 14 of a 40-page lease. Those clauses determined whether the landlord or tenant absorbed a $60,000 HVAC replacement. That is not a footnote. That is the deal.

The other pattern I see repeatedly is overconfidence in occupancy at acquisition. A fully leased building feels safe. But if three of your five tenants have leases expiring within 18 months and the local market has softened, you are not buying stability. You are buying a lease rollover problem. Lease rollover risk and operating expense reconciliation are the two variables that separate experienced CRE investors from people who learned an expensive lesson.

My practical advice: read every lease in full before you submit a letter of intent. Model the worst-case scenario where your largest tenant vacates on day one. If the property still pencils at 60% occupancy, you have a real investment. If it does not, you have a speculation. Know which one you are buying.

You can expand your real estate portfolio significantly once you develop the discipline to underwrite leases rather than just properties.

— Brian

Finance your next commercial property with Gannlending

Gannlending provides hard money loans built specifically for real estate investors who cannot afford to wait 60 days for a bank decision. When a commercial rental opportunity surfaces, whether it is a retail strip center, an industrial warehouse, or a multifamily complex, Gannlending funds deals in as few as five to seven business days with financing up to 75% LTV. The approval process focuses on the asset, not your paperwork stack. Gannlending has funded over $50 million in real estate transactions, and their team understands the speed and flexibility that commercial deals demand. Explore your commercial lending options and get your next deal funded before the competition does.

FAQ

What is the difference between commercial and residential rental property?

The primary difference is use. Commercial property is leased for business operations to generate income, while residential property is leased for private living. Multifamily buildings with five or more units are classified as commercial for financing and tax purposes.

What are the main types of commercial rental properties?

The four core types are office, retail, industrial, and multifamily residential (five or more units). Specialty categories include self-storage, medical office, hospitality, and mixed-use buildings that combine commercial and residential space.

How long are commercial rental agreements?

Commercial leases typically run three to ten years or longer, compared to the standard one-year residential lease. Longer terms benefit landlords through income predictability and benefit tenants through rent stability and negotiating leverage.

What is a triple net lease in commercial real estate?

A triple net lease requires the tenant to pay base rent plus property taxes, building insurance, and maintenance costs. This structure gives landlords highly predictable income because most variable operating expenses transfer to the tenant.

How do I start investing in commercial rental properties?

Start by identifying your target asset type, then analyze local zoning, lease structures, and financing options. Hard money lenders like Gannlending offer fast closings that let you act on time-sensitive deals while you build your track record in commercial real estate.