Repairing a rental property with a private loan is the fastest way for investors to fund renovations without depleting cash reserves or waiting months for bank approval. Private loans, known in the industry as hard money loans or bridge loans, give landlords access to capital based on the asset's value rather than personal income documentation. Investors using the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat) rely on these loans to move quickly on distressed properties. Gannlending and similar private lenders can close in as few as 5 to 7 business days, making them the go-to option when a furnace fails in January or a roof needs replacing before a tenant moves in.

What types of private loans are available for repairing rental properties?

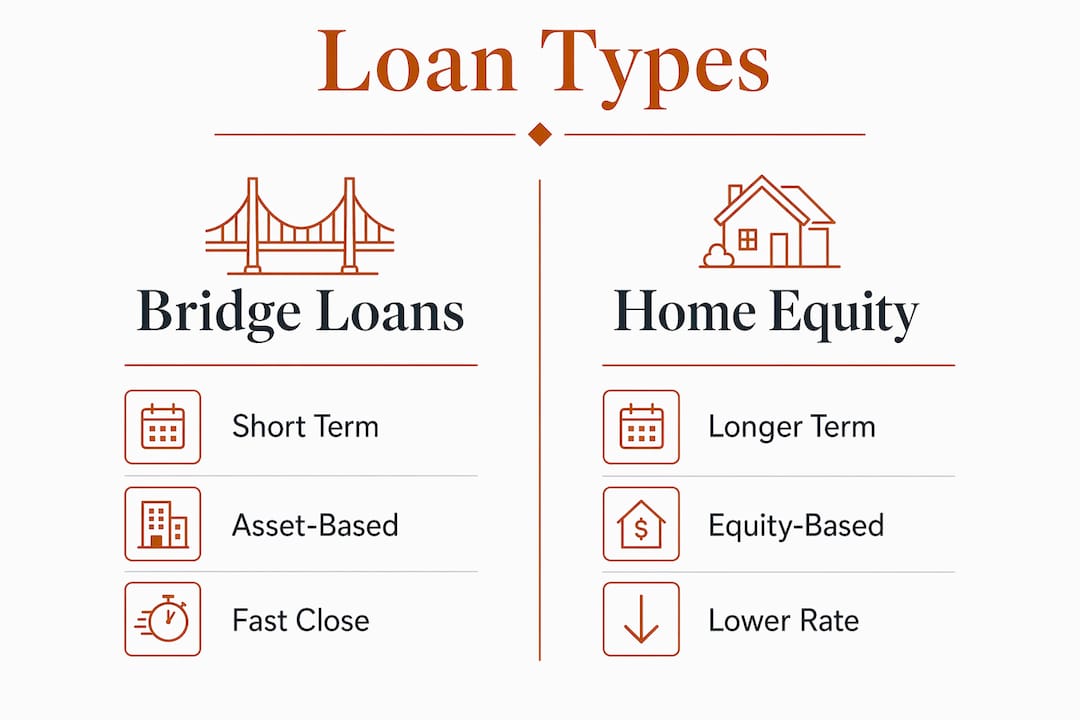

Private lending for rental repairs is not a single product. It is a category of short-term, asset-based financing with several distinct structures, each suited to different investor scenarios.

Bridge loans and fix and flip loans are the most common tools for financing rental property repairs. Private bridge loans can cover up to 92.5% of the total loan-to-cost, with interest rates starting at 9.99% and terms of 6, 9, 12, or 18 months. That coverage ratio means an investor with a solid project plan can enter a deal with relatively limited upfront capital. These loans are underwritten on the property's after-repair value (ARV), not the borrower's W-2.

Rehab-to-rental loans combine purchase and renovation funding into a single package. Rather than taking out two separate loans, the investor draws from one facility to buy the property and fund the repairs. This structure reduces closing costs and simplifies the paper trail, which matters when you are managing multiple projects simultaneously.

Home equity loans and HELOCs are a third option, particularly for landlords who already own properties with significant equity. The tax treatment here is worth noting: interest on home equity loans used for rental property improvements may be deductible on Schedule E, unlike interest on primary residence improvements. The tradeoff is that your primary home serves as collateral, which adds personal financial risk.

| Loan Type | Loan-to-Cost | Typical Rate | Term | Key Requirement |

|---|---|---|---|---|

| Bridge / Fix and Flip | Up to 92.5% | From 9.99% | 6–18 months | ARV, scope of work, exit plan |

| Rehab-to-Rental | Up to 85% | 10–12% | 12–24 months | Lease-up plan, DSCR projection |

| HELOC / Home Equity | Up to 80% CLTV | Prime + margin | 10–20 years | Primary home equity |

| DSCR Refinance | Up to 75–80% | 7–9% | 30 years | Signed lease or rent analysis |

Pro Tip: When comparing home improvement loans for rentals, always calculate the total cost of capital, not just the interest rate. A 12% bridge loan that closes in 5 days is often cheaper than a 7% bank loan that takes 60 days and costs you two months of vacancy.

The right loan type depends on your timeline, equity position, and exit plan. Most investors using private capital for portfolio growth default to bridge loans for speed and rehab-to-rental products for larger, more complex projects.

How to qualify and prepare to apply for a private repair loan

Qualifying for a private loan for landlord repairs is less about your credit score and more about your project. Private lenders evaluate three things above all: the property's ARV, the investor's equity contribution, and the clarity of the exit strategy.

Here is what a strong application looks like, step by step:

-

Calculate your equity contribution. Investors must generally provide 25 to 35% equity as a down payment or through existing property equity. This is the lender's primary risk buffer. If you are buying a distressed property at a discount, the purchase price discount can count toward this contribution.

-

Build a detailed scope of work. Lenders want line-item contractor bids, not ballpark estimates. A scope of work that lists materials, labor costs, and a realistic timeline signals that you have done the homework. Vague renovation budgets are the fastest way to get a loan declined or underwritten at a lower amount.

-

Support your ARV with comparable sales. Your after-repair value must be backed by recent sales of similar properties within a one-mile radius. Lenders will order their own valuation, but coming in with your own comps demonstrates credibility and speeds up the process.

-

Define your exit strategy in writing. Private lenders require a clear plan for how you will repay the loan. The two most common exits are a refinance into a long-term DSCR loan or a property sale. Vague answers here raise red flags.

-

Gather your asset documentation. Private lenders often do not require W-2s or pay stubs, which is a significant advantage for self-employed investors or those with complex tax profiles. You will typically need bank statements, a list of owned properties, and proof of funds for the down payment.

Pro Tip: Have at least three to six months of liquid reserves beyond your down payment before you close. Draw-based disbursement means you will be advancing renovation costs out of pocket before the lender reimburses you. Running out of cash mid-project is the most common reason renovations stall.

Understanding LTV and equity ratios before you apply puts you in a stronger negotiating position and helps you avoid surprises at the closing table.

What is the private loan application and funding process?

The application process for a private repair loan moves faster than most investors expect. A complete submission to funding can happen in under two weeks with the right lender. Here is what the process looks like in practice.

You submit your application with the property address, purchase price or current value, renovation budget, scope of work, and basic borrower information. The lender reviews the deal, orders a drive-by or desktop valuation, and issues a term sheet. Once you accept the terms, the loan moves to underwriting and closing.

The less obvious part of the process is what happens after closing. Private lenders release rehab funds incrementally through a draw schedule rather than as a lump sum. Each draw requires an inspection confirming that the prior stage of work is complete. This protects the lender but creates a cash flow challenge for the investor, who must fund each stage before receiving reimbursement.

Best practices during the renovation funding phase:

- Keep a dedicated renovation account separate from your operating accounts to track draws clearly.

- Schedule lender inspections proactively rather than waiting for the lender to initiate them. Delays in inspections are delays in your draw.

- Document every completed stage with photos and receipts before requesting a draw.

- Communicate scope changes to the lender immediately. Undisclosed changes can freeze your draw access.

- Maintain a cash buffer of at least 10 to 15% of the total renovation budget for unexpected costs.

Pro Tip: Build your contractor's payment schedule around the lender's draw timeline, not the other way around. Contractors who expect payment before the draw is released will create cash flow pressure that compounds quickly on larger projects.

Fast approval strategies for private bridge loans often come down to how complete and organized your submission package is on day one.

What are effective exit strategies after repairing a rental property?

The exit strategy is not an afterthought. It is the plan you build before you close the loan. Getting this wrong costs more than any renovation overrun.

The most common exit for investors who repair rental properties with private loans is a refinance into a DSCR loan. DSCR loans qualify based on rental income rather than personal tax returns, making them ideal for investors with multiple properties or non-traditional income. To qualify, the property must be stabilized: a signed lease or a documented market rent analysis is required. This means your renovation and lease-up timeline must align with your bridge loan maturity date.

The second exit is a straight sale of the property. This works well for fix and flip investors but is less common for landlords who want to hold the asset. A sale exit requires accurate ARV projections from the start, since the profit margin depends entirely on the spread between total cost and sale price.

A timing mismatch between bridge loan payoff and stabilization can trigger seasoning delays, forcing investors to carry expensive short-term debt longer than planned. Some DSCR lenders require 3 to 6 months of seasoning after a purchase or refinance before they will underwrite a new loan. Plan your renovation and lease-up timeline backward from that seasoning window.

| Exit Option | Best For | Key Advantage | Main Risk |

|---|---|---|---|

| DSCR Refinance | Buy and hold investors | Qualifies on rental income, not personal income | Seasoning delays if not stabilized in time |

| Property Sale | Fix and flip investors | Immediate capital recovery | Market timing risk, transaction costs |

Pro Tip: Sign your tenant lease before you apply for the DSCR refinance, not after. Lenders want to see an executed lease, not a letter of intent. A signed lease can shorten your underwriting timeline by weeks.

Emergency refinancing options exist for investors who find themselves in a timing bind between their bridge loan maturity and their refinance readiness.

Key takeaways

Using a private loan to repair a rental property works best when investors align their renovation timeline, lease-up schedule, and exit strategy from the start.

| Point | Details |

|---|---|

| Private loans close fast | Bridge loans and hard money loans can fund in 5 to 7 business days, far faster than conventional financing. |

| Equity contribution matters | Lenders require 25 to 35% equity, so calculate your contribution before submitting an application. |

| Draw schedules require cash reserves | Funds are released in stages after inspections, so maintain liquid reserves to bridge each phase. |

| DSCR loans are the primary exit | Refinancing into a DSCR loan qualifies on rental income, not personal tax returns, supporting long-term holds. |

| Seasoning delays are a real risk | Plan your renovation and lease-up timeline to meet DSCR lender seasoning requirements before your bridge loan matures. |

Why I think most investors underestimate the cash management side of private loans

Most conversations about how to fund property renovations focus on rates and loan-to-cost ratios. That is the wrong place to focus first. In my experience, the investors who run into trouble with private repair loans are not the ones who got a slightly higher rate. They are the ones who did not model their cash flow through the draw schedule.

Draw-based disbursement is a feature, not a flaw. It protects both the lender and the investor from contractors who front-load payments and disappear. But it means you are effectively pre-financing each stage of the renovation. On a $80,000 rehab, you might need $20,000 to $25,000 in accessible cash at any given time just to keep the project moving while you wait for inspection and reimbursement.

The second thing most investors underestimate is the seasoning window. Transitioning from bridge loans to DSCR financing requires a stabilized property, and stabilization takes time. If your renovation runs two weeks long and your lease-up takes an extra month, you may hit your bridge loan maturity date before you are eligible to refinance. That forces an extension, which costs money.

The investors I have seen scale successfully with private loans treat the exit strategy as the first decision, not the last. They know exactly which DSCR lender they are refinancing with before they close the bridge loan. They have already confirmed that lender's seasoning requirements, minimum DSCR ratio, and documentation checklist. That level of preparation is what separates investors who use private loans as a growth tool from those who use them as a last resort.

Private loans for landlord repairs are genuinely one of the most effective tools available for building a rental portfolio quickly. The BRRRR method works because of these loans. But the method only works if you treat the financing as a system, not a transaction.

— Brian

How Gannlending funds rental property repairs fast

Investors who need to repair a rental property and cannot wait for a traditional bank have a direct path forward with Gannlending.

Gannlending specializes in hard money loans for real estate investors, with closings in as few as 5 to 7 business days and no appraisal requirement. Their process focuses on the asset and the project plan, not your tax returns or employment history. Whether you are executing a BRRRR strategy, rehabbing a distressed rental, or funding urgent repairs to protect an existing tenancy, Gannlending has funded over $50 million in deals across residential and commercial properties. Visit Gannlending to get a quote and see how quickly your repair project can move from application to funded.

FAQ

What is a private loan for rental property repairs?

A private loan for rental property repairs is a short-term, asset-based loan issued by a non-bank lender, typically called a hard money or bridge loan. It funds based on the property's after-repair value rather than the borrower's income or credit score.

How fast can I get funded with a private repair loan?

Private lenders like Gannlending can close in 5 to 7 business days with a complete application package. Traditional bank loans for the same purpose typically take 30 to 60 days.

Do I need good credit to qualify for a private landlord repair loan?

Credit score requirements are flexible with most private lenders. Private lenders often skip W-2 and pay stub requirements, focusing instead on the property's value, your equity contribution, and your exit strategy.

What is a draw schedule and how does it affect my renovation?

A draw schedule is the process by which lenders release rehab funds incrementally after inspecting completed stages of work. Investors must advance costs from their own cash before each reimbursement, so liquid reserves are critical.

What is the best exit strategy after using a private repair loan?

Refinancing into a DSCR loan is the most common exit for buy-and-hold investors. DSCR loans qualify on rental income rather than personal income, making them well-suited for investors with multiple properties or non-traditional tax profiles.