A secure bridge loan in real estate is a short-term, collateral-based financing tool that gives investors and property owners fast access to capital when timing is everything. Unlike conventional mortgages, bridge loans are underwritten primarily on the property's value and your exit plan, not your tax returns or credit history. In 2026, rates typically run 9%–14%, reflecting the higher risk lenders absorb in exchange for speed. Whether you're racing to close an acquisition, funding a renovation, or stopping a foreclosure, understanding how this financing works is the difference between seizing an opportunity and losing it.

What qualifies you for a secure bridge loan in real estate?

Bridge loan eligibility centers on the asset, not the borrower. Lenders underwrite primarily on collateral value and your exit strategy, which means a strong property can carry a weaker personal credit profile further than it would with a conventional bank.

Collateral and loan-to-value requirements

Most bridge lenders cap financing at 50%–75% LTV, depending on property type and condition. A distressed commercial asset might get approved only at 50% LTV, while a stabilized residential property in a liquid market could reach 75%. The lower the LTV, the more equity you're putting up as a buffer for the lender.

Credit score and documentation standards

Some private lenders require no personal tax returns or FICO scores when collateral and exit plans are strong. Traditional bridge lenders typically want a credit score in the mid-600s or higher. The documentation you should prepare includes:

- A current property appraisal or broker price opinion

- A signed purchase contract if you're acquiring a new property

- A written exit strategy detailing how you'll repay the loan

- Bank statements showing cash reserves

- Debt-to-income documentation if the lender requires it

Why your exit strategy is the real approval factor

A clear, realistic exit plan is the single most important element in your application. Common exit paths include property sale, permanent refinancing, or overlapping mortgage payoff. Lenders who approve a deal without a credible exit are taking on unacceptable risk, and they know it. Your exit strategy should be specific: name the buyer, the refinance lender, or the timeline with market data to back it up.

Pro Tip: If your credit score is below 650, lead with the property's value and your exit plan. A private lender focused on asset-based underwriting will weigh those two factors far more heavily than your FICO number.

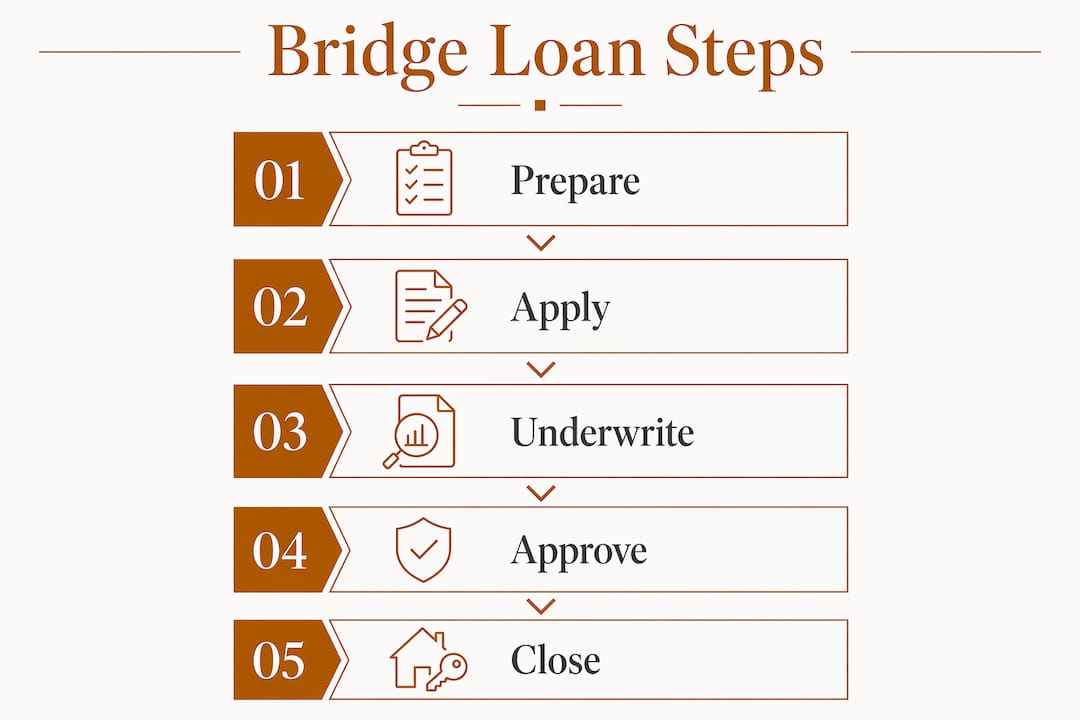

How to apply for real estate bridge financing step by step

The application process for short-term real estate financing moves faster than most investors expect. Bridge loans typically close in 2–4 weeks, compared to the 45–90 days a conventional loan often requires. Here is the process from start to funded.

-

Assess your financing need. Confirm the property qualifies as collateral and calculate how much capital you need versus what the LTV cap will allow. If you need $800,000 and the property appraises at $1,000,000, a 75% LTV lender can cover you. A 60% LTV lender cannot.

-

Gather your documents. Pull together the appraisal, purchase contract, bank statements, and your written exit strategy before you contact a single lender. Lenders move faster when you arrive prepared.

-

Compare lender types. Private lenders and hard money lenders close faster and ask fewer questions than banks. Banks offer lower rates but require full documentation and take longer. For time-sensitive deals, fast-funding strategies from private lenders are often the only viable path.

-

Submit your application with a detailed exit strategy. Do not submit a vague plan. State whether you're selling, refinancing, or paying off with proceeds from another asset. Include a timeline and supporting data.

-

Undergo underwriting. The lender will order an appraisal or desk review, verify the collateral, and stress-test your exit plan. This stage typically takes 5–10 business days with a private lender.

-

Close and receive funds. Once underwriting clears, you sign loan documents and funds are wired. Private lenders can often fund within 5–7 business days of a complete application.

Pro Tip: Submit to two or three lenders simultaneously. Bridge loan terms vary significantly between lenders, and a competing offer gives you real negotiating leverage on rate and fees.

What bridge loan options are available and how do they compare?

Not all bridge loan options are structured the same way. The right product depends on your property type, how much documentation you can provide, and how quickly you need to close.

Residential vs. commercial bridge loans

Residential bridge loans are simpler. They typically cover single-family homes, small multifamily properties, and condos. Commercial bridge loans cover office, retail, industrial, and larger multifamily assets. Commercial and multifamily bridge loans often require more documentation and carry more complex underwriting, including rent rolls, occupancy reports, and operating statements.

Asset-based vs. full documentation loans

Multifamily bridge loans can use a 50% LTV asset-based underwriting approach with no personal income or FICO requirements under certain conditions. Full documentation loans allow higher LTVs, sometimes reaching 75%–80%, but require tax returns, income verification, and a longer approval timeline. The trade-off is straightforward: less documentation means lower LTV and faster closing; more documentation means higher LTV and slower closing.

Here is how the main bridge loan structures compare:

| Feature | Asset-Based Bridge Loan | Full Documentation Bridge Loan |

|---|---|---|

| LTV | 50%–60% | 65%–75% |

| Interest Rate | 10%–14% | 9%–12% |

| Loan Term | 6–12 months | 12–36 months |

| Credit Requirement | None or minimal | Mid-600s or higher |

| Closing Speed | 5–14 days | 3–6 weeks |

| Best Use Case | Distressed assets, foreclosure rescue | Stabilized value-add, acquisitions |

Common use cases worth knowing

Bridge loans finance value-add renovations, lease-up costs, and repositioning of income-producing properties before permanent financing takes over. Beyond renovation, the most common use cases include:

- Stopping a foreclosure when a conventional refinance cannot close in time

- Acquiring a property at auction where a 30-day close is required

- Carrying a new property while waiting for an existing one to sell

- Funding a quick renovation to qualify for agency financing

What are the biggest pitfalls when obtaining bridge loans?

The speed and flexibility of bridge loans come at a real cost. Knowing where investors go wrong protects your deal and your equity.

"A bridge loan is a surgical tool. Use it precisely, with a defined exit, and it solves a real problem. Use it loosely, and the interest clock will punish every delay." — Brian, Gannlending

The risks that catch investors off guard

Higher rates are the most obvious cost, but they are rarely the most dangerous one. The real risk is an exit strategy that fails. If your property does not sell on schedule or your refinance falls through, you face extension fees, default rates, and potentially foreclosure. Bridge loans are best reserved for broken deals, distressed properties, or time-sensitive acquisitions where the speed justifies the premium.

Watch for these specific pitfalls:

- Over-leveraging: Borrowing at the maximum LTV leaves no room for a price drop or appraisal shortfall at refinance.

- Ignoring market absorption rates: If your exit depends on selling, confirm how long comparable properties are sitting on the market before you commit to a 6-month term.

- Underestimating total cost: Add origination fees (typically 1%–3%), interest, and extension fees to calculate the true cost of the loan before signing.

- Weak lender relationships: A lender who has never extended a loan in a tough market is a risk. Ask about their track record with extensions before you close.

For investors facing urgent situations, emergency refinancing options can provide an alternative path when a bridge loan alone is not enough.

Pro Tip: Build your exit strategy around the worst-case timeline, not the best case. If you think the property sells in 90 days, plan for 150. A bridge loan with a 12-month term gives you room to absorb delays without defaulting.

Key takeaways

Securing a bridge loan in real estate requires strong collateral, a credible exit strategy, and a lender matched to your property type and timeline.

| Point | Details |

|---|---|

| Collateral drives approval | LTV ratios of 50%–75% determine how much you can borrow based on property value. |

| Exit strategy is non-negotiable | Name your specific exit path, sale, refinance, or payoff, with a realistic timeline and supporting data. |

| Lender type affects speed | Private and hard money lenders close in 5–14 days; banks take 3–6 weeks with full documentation. |

| Total cost exceeds the rate | Factor in origination fees of 1%–3% and potential extension fees when calculating true loan cost. |

| Asset-based loans skip credit checks | Some private lenders approve deals with no FICO or tax return requirements when collateral is strong. |

Why i think most investors misuse bridge loans

Most investors treat a bridge loan like a backup plan. That is exactly backwards. The investors I have seen use bridge financing most effectively treat it as a primary weapon in a specific, time-bound situation. They know their exit before they know their rate.

The mistake I see repeatedly is borrowing at the maximum LTV because the lender allows it. Just because a lender will go to 75% does not mean you should. Every point of leverage you add is another point of exposure if the market shifts or your refinance takes longer than expected. I have watched deals that looked profitable on paper turn into losses because the investor underestimated how long a renovation would take and burned through their reserves paying bridge interest.

The other thing most articles will not tell you: lender selection matters more than rate. A lender who has funded over $50 million in real estate deals, like Gannlending, has seen every type of deal complication. They know when to extend, when to restructure, and when to push a borrower toward a better exit. A lender you found through a rate comparison site may not have that depth of experience when your deal gets complicated.

Use bridge financing when the opportunity is real, the exit is clear, and the cost is justified by what you stand to gain. Do not use it to paper over a deal that does not work at conventional financing terms.

— Brian

Get funded in 5–7 days with Gannlending

Real estate deals do not wait for slow approvals. Gannlending funds hard money bridge loans in as few as 5–7 business days, with no appraisal delays and financing up to 75% LTV on residential and commercial properties.

Gannlending has funded over $50 million in real estate deals, working with investors who need speed, flexibility, and a lender who understands asset-based underwriting. Whether you are stopping a foreclosure, closing a time-sensitive acquisition, or funding a value-add renovation, Gannlending structures the loan around your property and your exit, not a checklist of paperwork. Contact Gannlending today to get your deal reviewed and funded fast.

FAQ

What is a secure bridge loan in real estate?

A secure bridge loan in real estate is a short-term loan collateralized by property, designed to provide fast capital for acquisitions, renovations, or foreclosure prevention. Loan terms typically run 6–36 months with interest rates of 9%–14%.

How quickly can you close a bridge loan?

Bridge loans close in as few as 5–7 business days with a private lender and typically within 2–4 weeks across the broader market. Conventional loans take 45–90 days by comparison.

Do you need good credit to qualify for a bridge loan?

Not always. Some private lenders approve bridge loans with no FICO score or tax return requirements when the collateral is strong and the exit strategy is credible. Traditional lenders typically want a mid-600s credit score or higher.

What is the maximum LTV on a bridge loan?

Bridge loan LTV caps range from 50% to 80% depending on lender policy, property type, and condition. Asset-based loans for distressed properties often cap at 50%–60%, while full documentation loans on stabilized assets can reach 75%–80%.

What happens if you cannot repay a bridge loan on time?

If your exit strategy fails and you cannot repay on schedule, most lenders offer a paid extension at a higher rate. Without an extension agreement, the loan enters default, which can trigger foreclosure on the collateral property.