Property management company financing is defined as the capital structure that funds acquisitions, covers operating costs, and supports portfolio growth for real estate investors and property managers. The role of property management company financing extends well beyond a simple purchase loan. It shapes how quickly you can close on a company, how lenders assess your income, and how you survive the cash flow gaps that hit every management operation. The median acquisition price for a property management company sits at $567,500, with a 2.9x cash flow multiple. That figure sets the baseline for every equity and debt calculation you will make.

What financing options are available for property management companies?

Property management financing options fall into five main categories, each suited to a different need and timeline.

- SBA 7(a) loans are the most common acquisition tool. They cover the bulk of the purchase price and allow a seller note on full standby to count as equity. This structure reduces the cash you need at closing without violating SBA rules.

- Working capital loans range from $25,000 to $500,000 with terms of 3–24 months. They fund fast operational capital for emergencies, new staff, and portfolio onboarding, often within 24–48 hours of approval.

- Business lines of credit give you revolving access to funds without creating fixed monthly debt. They work best for managing the timing gaps between collecting management fees and paying vendor invoices.

- Equipment financing covers property management software, maintenance vehicles, and office infrastructure. The equipment itself serves as collateral, which keeps approval requirements lower than unsecured loans.

- Merchant cash advances and fast business loans deliver capital within days. The cost is higher, but for an emergency repair that cannot wait, speed outweighs rate.

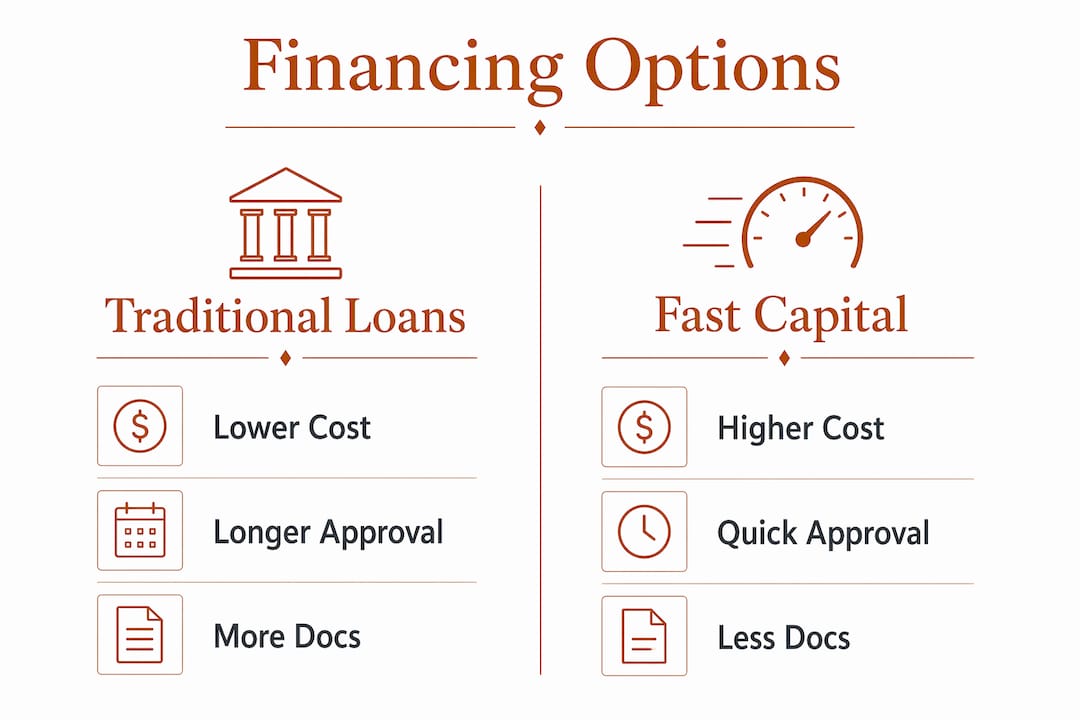

The trade-off across all five is the same: lower cost means slower approval and more documentation. Faster funding means higher rates and shorter terms. Your choice depends on whether the need is planned or urgent.

Pro Tip: Set up a business line of credit before you need it. Lenders approve lines based on healthy financials, not on desperation. Having one in place means you draw from it the day an emergency hits, not three weeks later.

How does property management affect financing and lending decisions?

Property management operations directly shape how lenders calculate your net operating income (NOI) and whether your loan gets approved. The most misunderstood factor is the management fee assumption. Lenders assume management fees at 8–12% of gross rental income when calculating DSCR, even if you self-manage the property. That assumption reflects realistic long-term operating costs and protects the lender from underwriting a deal that only works if you never hire help.

Here is how those assumptions affect a real deal:

| Expense Category | Typical Lender Assumption | Impact on NOI |

|---|---|---|

| Management fees | 8–12% of gross rent | Reduces NOI directly |

| Maintenance reserves | 5–10% of gross rent | Reduces NOI directly |

| Vacancy allowance | 5–8% of gross rent | Reduces effective gross income |

| Example: $3,000 rent | Less $800 total expenses | $2,200 NOI used for DSCR |

These deductions are not negotiable with most lenders. A $3,000 monthly rent unit does not produce $3,000 in qualifying income. After the standard deductions, the lender works with $2,200 or less. That gap determines whether your debt service coverage ratio clears the minimum threshold.

Professional management agreements act as critical underwriting assets. They prove income stability and demonstrate that a qualified operator controls the asset. Lenders treat a signed, long-term management agreement as stronger evidence of income than a lease alone.

Pro Tip: Never submit a loan application for a rental property without attaching the management agreement. A missing agreement forces the underwriter to make conservative assumptions, which almost always lowers your qualifying income.

The most common pitfall is underestimating operating expenses. Investors who project NOI using only mortgage and tax costs get a rude surprise at underwriting. Lenders add back the full expense load regardless of what your spreadsheet shows.

What financial challenges do property management companies face?

Property management companies face a specific set of cash flow problems that general business financing does not always address well.

The biggest is the liquidity trap. Emergency repairs must be paid immediately, but property managers cannot use owner trust funds for that purpose. Trust accounts are legally segregated. The repair bill lands on the management company's operating account, which may not have the cash to cover it. A broken HVAC unit in july can cost $5,000 to $15,000. Without a credit line, that cost either stalls the repair or comes out of the company's own reserves.

Portfolio onboarding creates a second cash crunch. When you win a new management contract covering 50 units, you spend money on inspections, software setup, tenant communication, and staff time before you collect a single management fee. That gap can run four to six weeks. Working capital financing covers that period without forcing you to turn down growth.

Other common pressure points include:

- Technology upgrades: Property management platforms, maintenance tracking software, and tenant portals require upfront investment that pays off over years, not months.

- Staffing expansions: Hiring a leasing agent or maintenance coordinator before revenue catches up is a calculated bet that requires short-term capital.

- Marketing for new clients: Acquiring new property owner clients costs money in advertising, networking, and sales time before any fee income arrives.

Financing gap solutions built for real estate investors address these cycles better than generic small business products, because they account for the trust account structure and fee-based income timing that define the industry.

What are the underwriting and equity requirements for property management acquisitions?

Buying a property management company requires a specific equity structure that differs from standard real estate purchases. The standard is a 10% equity injection, split roughly in half between buyer cash and a seller note on full standby. On a $567,500 deal, that means approximately $28,375 in buyer cash and a matching seller note. Total cash at closing, including fees and working capital reserves, typically runs $40,000–$60,000.

The seller note on full standby is a key detail. "Full standby" means the seller receives no payments on that note during the SBA loan term. Seller notes structured this way count as equity in the SBA's calculation, which reduces the cash you need to bring to closing. It is a legitimate tool, not a workaround.

SBA 7(a) loans cover the remaining purchase price and typically carry interest rates tied to the prime rate plus a lender spread. Documentation requirements are significant. Lenders expect two to three years of business tax returns, a detailed business plan, a management fee schedule, and evidence of the existing client base. The strength of your documentation package directly affects approval speed.

As portfolios grow into larger apartment complexes, financing shifts to commercial underwriting that focuses on management systems, reserves, and execution track record rather than individual property DSCR. That shift rewards investors who built strong operational documentation from the start.

Pro Tip: Build your lender relationship before you find the deal. A lender who already knows your financials and management track record can move in days, not weeks, when the right acquisition appears.

How can investors use property management financing to grow their portfolio?

Financing for property managers is most powerful when used as a growth tool, not just a survival mechanism. The investors who scale fastest treat their credit access as a planned resource, not a last resort.

- Acquire with SBA financing, then refinance. Use an SBA 7(a) loan to acquire a property management company at favorable terms, then refinance into conventional commercial debt once the business shows two years of clean financials. This frees up SBA capacity for the next acquisition.

- Use working capital lines for operational growth. A revolving line of credit lets you onboard new portfolios, hire staff, and upgrade systems without waiting for fee income to catch up. Draw what you need, repay as fees arrive, and repeat.

- Document everything for lender confidence. Every management agreement, lease renewal, and maintenance record strengthens your underwriting file. Lenders reward documentation with better terms and faster approvals. Explore portfolio loan structures once your managed units reach a scale that justifies blanket financing.

- Plan DSCR around realistic vacancy rates. Use the lender's 5–8% vacancy assumption in your own projections. If your actual vacancy is lower, that is upside. If you plan around zero vacancy, you will miss DSCR thresholds and lose deals.

- Match financing term to the asset's purpose. Short-term working capital loans fit operational gaps. Long-term SBA or commercial loans fit acquisitions. Mixing them creates cash flow problems when short-term debt matures before the asset generates enough income to repay it.

Real estate portfolio financing strategies that account for management company income alongside rental income give investors a more complete picture of their borrowing capacity. The two income streams, management fees and rental income, compound each other's value in the right financing structure.

Key Takeaways

Property management company financing works best when investors match each capital product to a specific operational need rather than relying on a single loan type.

| Point | Details |

|---|---|

| Equity injection standard | Plan for 10% equity on acquisitions, split between buyer cash and a seller note on full standby. |

| DSCR expense assumptions | Lenders deduct 8–12% management fees, 5–10% maintenance, and 5–8% vacancy from gross rent before calculating NOI. |

| Liquidity trap risk | Trust account restrictions mean emergency repairs must come from operating cash or a credit line, not owner funds. |

| Documentation drives approval | Management agreements, tax returns, and client records directly affect loan speed and terms. |

| Match product to need | Use working capital loans for short-term gaps and SBA or commercial loans for acquisitions. |

What I have learned about financing property management companies

The biggest mistake I see real estate investors make is treating property management company financing as an afterthought. They find the deal first, then scramble to figure out the capital. That sequence costs them time, money, and sometimes the deal itself.

The investors who close cleanly are the ones who understand their DSCR before they make an offer. They know that a lender will deduct management fees from gross rent even if they plan to self-manage. They have their documentation organized before they need it. And they have a credit line in place before an emergency forces them to find one under pressure.

The enterprise property management finance structure is genuinely complex. It serves owners, lenders, and regulators at the same time. That complexity is not a reason to avoid it. It is a reason to prepare for it. Investors who understand the multi-stakeholder reporting requirements that lenders expect are the ones who get approved faster and at better rates.

My practical advice: treat your management agreements as financial documents, not just operational ones. A well-structured agreement with a long-term client is worth real money in an underwriting file. Lenders see it as proof that your income is stable and that a qualified operator controls the asset. That perception changes what terms you get offered.

— Brian

Gannlending: fast capital for property management investors

Real estate investors who need capital quickly for acquisitions or operational needs have a direct path through Gannlending. Gannlending provides hard money loans with no appraisal requirement and closing in as few as 5–7 business days, covering up to 75% LTV on residential and commercial properties. With over $50 million funded, Gannlending focuses on the asset, not paperwork.

Whether you are acquiring a property management company, funding emergency repairs, or bridging a cash flow gap between fee cycles, Gannlending structures capital around your timeline. Investors facing foreclosure also have access to fast solutions that protect their assets. If you need capital that moves as fast as your deals do, Gannlending is built for that.

FAQ

What is the role of property management company financing?

Property management company financing provides the capital needed to acquire management businesses, cover operating costs, and fund portfolio growth. It supports acquisitions through SBA loans, manages cash flow gaps with working capital lines, and funds emergency repairs that trust accounts cannot cover.

How do management fees affect DSCR loan qualification?

Lenders assume management fees of 8–12% of gross rental income when calculating DSCR, even for self-managed properties. This reduces qualifying NOI and directly affects whether a loan meets the minimum debt service coverage threshold.

How much cash do I need to buy a property management company?

The standard equity injection is 10% of the purchase price, split between buyer cash and a seller note on full standby. On a median deal of $567,500, total cash at closing including fees typically runs $40,000–$60,000.

Why do property management companies need lines of credit?

Property managers face a liquidity gap because emergency repairs must be paid immediately from operating funds, not owner trust accounts. A business line of credit covers these costs without disrupting cash flow or delaying repairs.

What documents do lenders require for property management financing?

Lenders typically require two to three years of business tax returns, a current management fee schedule, signed management agreements, a client roster, and a business plan. Strong documentation shortens approval timelines and improves loan terms.