A property portfolio loan is a single mortgage that covers multiple investment properties under one consolidated financing agreement, replacing the need to manage separate loans for each asset. Also called a blanket mortgage in real estate investing circles, this structure is classified as a non-conforming loan because it does not meet Fannie Mae or Freddie Mac standards. That distinction matters: lenders keep the loan on their own books rather than selling it on the secondary market, which gives them freedom to set custom terms. For investors managing four or more rental properties, understanding what is a property portfolio loan can change how you finance and scale your entire operation.

What is a property portfolio loan and how does it work?

A property portfolio loan consolidates multiple rental properties under one financing facility, eliminating the administrative burden of tracking separate mortgage payments, lenders, and closing dates for each property. Instead of five separate loans for five rentals, you carry one loan with one payment and one lender relationship. That simplification alone is a major operational advantage for landlords managing more than a handful of assets.

Because the lender retains the loan rather than selling it, the underwriting process works differently from a standard mortgage. The lender evaluates the portfolio as a single income-generating unit rather than assessing each property in isolation. This retained risk model gives lenders the authority to customize terms, adjust repayment structures, and weigh borrower circumstances that a conventional loan program would reject outright.

The non-conforming classification also means these loans can reach sizes that standard programs cannot touch. Typical portfolio loans are often jumbo or super jumbo structures, sometimes exceeding $3 million. That scale makes them particularly relevant for investors operating in high-cost markets or managing large mixed-asset portfolios.

How portfolio loan underwriting actually works

Portfolio loan underwriting centers on the Debt Service Coverage Ratio, known as DSCR, calculated across the entire property portfolio rather than any single asset. DSCR measures whether the rental income generated by your properties is sufficient to cover the loan payments. A DSCR above 1.0 means the portfolio earns more than it costs to service the debt. Lenders typically want to see a DSCR of 1.2 or higher before approving a portfolio loan.

The key difference from traditional mortgage underwriting is what lenders do not look at. Portfolio underwriting ignores personal income verification in many cases, skipping the W-2s, tax returns, and debt-to-income ratio calculations that define conventional loan approvals. This is a significant advantage for investors who hold properties in LLCs, earn income through multiple business entities, or show irregular personal income on paper.

Here is what portfolio lenders typically evaluate instead:

- Aggregate rental income across all properties in the portfolio

- DSCR for the combined portfolio, not individual properties

- Property condition and occupancy rates

- Loan-to-value ratio across the consolidated asset base

- Borrower experience and track record as a real estate investor

Pro Tip: Before applying for a portfolio loan, prepare a property-level income and expense summary for every asset in your portfolio. Lenders who use DSCR underwriting will want to see this data organized clearly, and having it ready shortens the approval timeline considerably.

Because lenders retain these loans on their own balance sheets, they can also overlook minor credit blemishes if the portfolio's cash flow is strong enough to offset the risk. That flexibility does not mean credit is irrelevant. It means the portfolio's performance carries more weight than a borrower's personal financial profile.

What do property portfolio loans cost?

Portfolio loans carry a real price premium. Interest rates run 0.5% to 2.0% higher than standard investment property loans, reflecting the fact that lenders absorb all the risk rather than offloading it to the secondary market. On a $2 million portfolio loan, a 1% rate premium translates to $20,000 more in annual interest. That is not a trivial number, and investors need to model it against the administrative savings and flexibility the structure provides.

"Portfolio loans do not conform to Fannie Mae or Freddie Mac standards, which allows lenders to set bespoke terms. That freedom comes at a cost investors must factor into their return calculations before committing."

The table below outlines how portfolio loan costs compare to conventional investment property financing across key dimensions:

| Feature | Conventional investment loan | Portfolio loan |

|---|---|---|

| Interest rate | Market rate | 0.5%–2.0% above market |

| Underwriting basis | Individual borrower credit and DTI | Portfolio DSCR and rental income |

| Loan size | Up to conforming limits | Jumbo and super jumbo available |

| Lender risk | Sold to secondary market | Retained by lender |

| Term flexibility | Standardized | Customizable per borrower |

Fees also tend to be higher on portfolio loans. Origination fees, prepayment penalties, and closing costs reflect the custom nature of the underwriting work. Loan term lengths vary widely because lenders set their own parameters. Some portfolio loans carry 15-year or 20-year amortization schedules with balloon payments, which is a structure investors rarely see in conventional financing. Understanding LTV ratios and how they affect pricing is critical before comparing offers from different portfolio lenders.

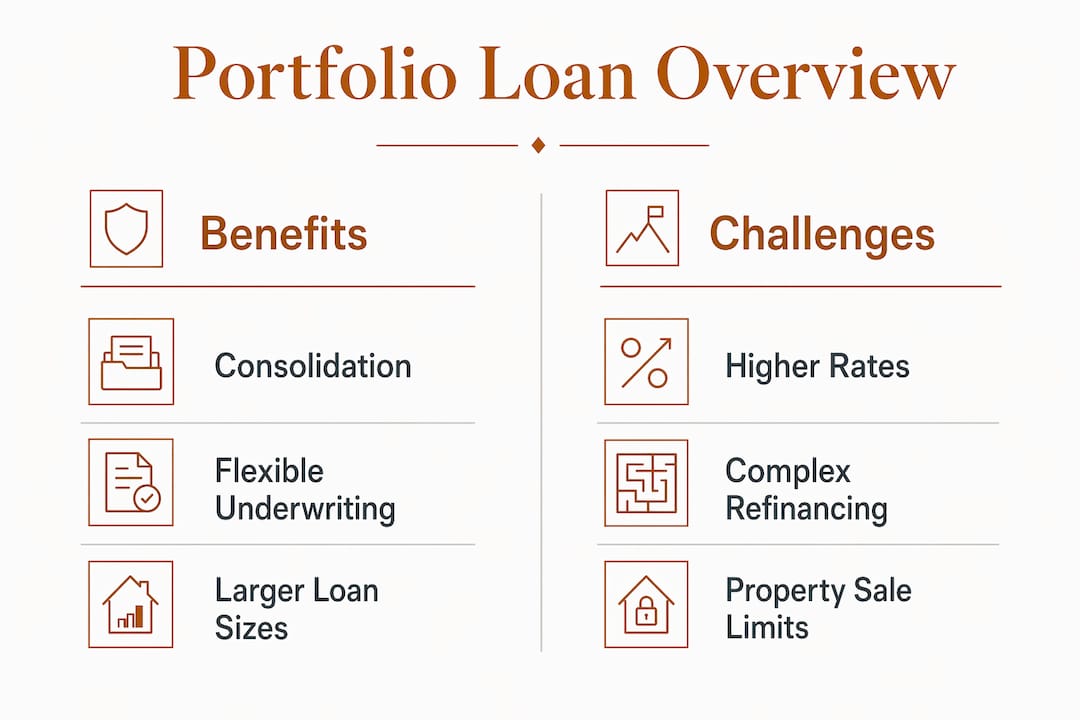

Benefits and challenges of a property portfolio loan

The administrative benefits of a portfolio loan are real and significant. One monthly payment replaces multiple payments across separate lenders. One lender relationship replaces multiple points of contact for questions, modifications, and renewals. Cash flow tracking becomes simpler because all properties feed into one debt obligation rather than several.

- Consolidated payments reduce the risk of missed payments across multiple accounts and simplify monthly bookkeeping.

- Single lender relationship means one point of contact for modifications, payoffs, and future financing conversations.

- Flexible underwriting allows investors with non-traditional income structures to qualify based on portfolio performance.

- Faster scaling becomes possible because adding properties to an existing portfolio loan is often simpler than originating new individual mortgages.

- Access to non-standard assets opens up because portfolio loans can finance fixer-uppers and unique properties that conventional lenders reject.

The challenges are equally real. Refinancing or selling individual properties within a portfolio loan is complicated. Because all assets are bundled under one loan, removing a single property often requires restructuring the entire agreement. That process takes time, costs money, and can create friction when market conditions make selling one asset attractive.

Pro Tip: Before bundling properties into a portfolio loan, identify which assets you might want to sell or refinance independently within the next three to five years. Properties you plan to hold long-term are the best candidates for inclusion. Properties you might exit soon are better kept on separate financing.

Portfolio restructuring also becomes complex when you want to add new properties. Some lenders allow additions with a straightforward amendment. Others require a full re-underwriting of the entire portfolio. Knowing your lender's policy on this before signing is not optional. It is a deal-defining detail.

Who qualifies and when does a portfolio loan make sense?

Most lenders require at least four mortgaged investment properties to qualify for a portfolio loan. That threshold exists because the DSCR underwriting model needs sufficient aggregate rental income to function. A two-property portfolio does not generate enough data or income diversity to justify the structure. Portfolio underwriting is simply not available to new or small-scale investors.

Investors who benefit most from portfolio loans typically fall into one of these categories:

- Scaling landlords with four or more single-family rentals who want to simplify management and free up capacity for additional acquisitions

- Investors with irregular income such as self-employed operators, business owners, or those who hold properties in LLCs where personal income documentation is complex

- High-cost market investors whose portfolios exceed conforming loan limits and need jumbo-level financing

- Investors holding non-standard assets such as mixed-use buildings, fixer-uppers, or properties that conventional lenders decline

Eligible property types typically include single-family rentals, small multifamily buildings, and some commercial assets, depending on the lender. Documentation requirements focus on portfolio income rather than personal financials. Rent rolls, lease agreements, and property-level profit and loss statements replace the W-2s and tax returns that define conventional loan applications.

Investors who are just starting out or who own fewer than four properties are better served by individual investment property loans until their portfolio reaches the threshold. Building your rental portfolio with private lending is one path that helps newer investors accumulate properties faster before transitioning to a consolidated structure.

Key Takeaways

A property portfolio loan is the most efficient financing structure for experienced investors managing four or more rental properties, offering consolidated payments and DSCR-based underwriting in exchange for a rate premium and reduced individual property flexibility.

| Point | Details |

|---|---|

| Core definition | A portfolio loan consolidates multiple investment properties under one mortgage with one lender. |

| Underwriting basis | Lenders use DSCR across the full portfolio, not personal income or individual property metrics. |

| Rate premium | Expect interest rates 0.5%–2.0% above standard investment loans due to lender risk retention. |

| Minimum threshold | Most lenders require at least four mortgaged investment properties to qualify. |

| Key trade-off | Administrative simplicity comes at the cost of flexibility when selling or refinancing individual assets. |

Why I think most investors misread the portfolio loan trade-off

The conventional wisdom on portfolio loans focuses almost entirely on the rate premium. Investors see the higher interest cost and stop there. That framing misses the more important question, which is whether the administrative and underwriting flexibility justifies the cost given your specific portfolio and growth plan.

I have seen experienced investors turn down portfolio loans because the rate was 1.5% higher, only to spend the next two years managing six separate lenders, six renewal cycles, and six sets of covenants. The time and energy cost of that complexity rarely shows up in a spreadsheet, but it is real and it compounds.

The more dangerous mistake is bundling properties without thinking through the exit. Once you consolidate into a portfolio loan, selling one property is not a clean transaction. It requires lender involvement, potential restructuring fees, and sometimes a full re-underwriting. Investors who treat a portfolio loan like a flexible line of credit get burned when they need to move quickly on a sale.

The investors who use portfolio loans well are the ones who have already decided which properties they are holding for the long term. They use the consolidated structure to free up mental bandwidth and capital for new acquisitions, not as a catch-all for every asset they own. Working with a lender who customizes underwriting per portfolio profile, rather than applying a rigid template, makes a significant difference in how the loan performs over time. Loan customization options are worth understanding before you sit down with any lender.

— Brian

Gannlending's approach to portfolio financing

Real estate investors who need fast, flexible financing for multiple properties work with Gannlending for a reason.

Gannlending is a private hard money lender that has funded over $50 million in real estate loans, with closing times as fast as 5–7 business days and no appraisal requirement. Financing covers up to 75% LTV across residential and commercial property types. Underwriting focuses on the asset and the portfolio's performance, not endless personal financial documentation. For investors ready to consolidate, scale, or refinance multiple properties under one structure, Gannlending's private lending solutions offer the speed and flexibility that conventional lenders cannot match.

FAQ

What is a portfolio mortgage in simple terms?

A portfolio mortgage is a single loan that covers multiple investment properties at once, held by the lender rather than sold on the secondary market. It replaces separate mortgages for each property with one consolidated payment and one lender relationship.

How many properties do you need for a portfolio loan?

Most lenders require at least four mortgaged investment properties to qualify for a portfolio loan. This threshold exists because the DSCR underwriting model needs sufficient aggregate rental income to assess risk accurately.

Are interest rates higher on portfolio loans?

Yes. Portfolio loan rates are typically 0.5% to 2.0% above standard investment property loan rates because lenders retain all the risk rather than selling the loan to Fannie Mae or Freddie Mac.

Can you sell a property that is part of a portfolio loan?

Selling an individual property within a portfolio loan is possible but complicated. It usually requires lender approval and may trigger a restructuring of the entire loan agreement, which adds time and cost to the transaction.

Who should use a property portfolio loan?

Portfolio loans work best for experienced investors with four or more long-term rental properties, particularly those with non-traditional income structures or properties that conventional lenders would not finance. New investors or those with fewer than four properties are better served by individual investment property loans.