A stabilized property is defined as a real estate asset that has reached sustained occupancy of 90% or higher over a 6 to 12 month period, with predictable net operating income and normalized operating expenses. In commercial real estate, this threshold signals operational maturity. It tells lenders, investors, and developers that the asset performs consistently and no longer carries the uncertainty of a lease-up or construction phase. Understanding what is a stabilized property is the foundation of sound portfolio strategy, whether you are acquiring your first income property or refinancing a mature commercial asset.

What is a stabilized property? Core definition and benchmarks

A stabilized property meets two conditions simultaneously: it holds occupancy at or above market norms, and it generates consistent, predictable income. The industry standard occupancy threshold is 90%, measured over a continuous 6 to 12 month window. That window matters because a single strong month does not prove stability. Sustained performance does.

Not every market applies the same threshold. An 80% occupancy rate for one full calendar quarter is accepted as stabilization in certain asset classes or softer markets. That lower floor reflects local absorption rates and property type. A suburban industrial park in a secondary market operates under different demand dynamics than a Class A multifamily tower in Manhattan.

Beyond physical occupancy, economic occupancy is the number that actually matters. Physical occupancy counts how many units are leased. Economic occupancy measures how much of the potential rent is actually collected. A building can be 95% physically occupied and still fail the stabilized property definition if tenants are paying below-market rents or receiving free months as concessions.

Pro Tip: Always request a rent roll alongside the occupancy report. Compare in-place rents to current market rates before accepting any stabilization claim at face value.

The income side of the equation requires stable NOI and normalized operating expenses, with no major capital improvements or deferred maintenance outstanding. A property with a leaking roof, aging HVAC systems, or pending tenant improvement obligations is not stabilized, regardless of its occupancy rate.

Key occupancy and income benchmarks to verify:

- Physical occupancy: 90% or higher in most markets, 80% minimum in select asset classes

- Economic occupancy: In-place rents at or near current market rates, with no material concessions

- NOI consistency: Trailing 12 months of net operating income showing a stable or improving trajectory

- Expense normalization: No extraordinary capital expenditures or deferred maintenance items pending

- Measurement period: Occupancy and income sustained over 6 to 12 consecutive months

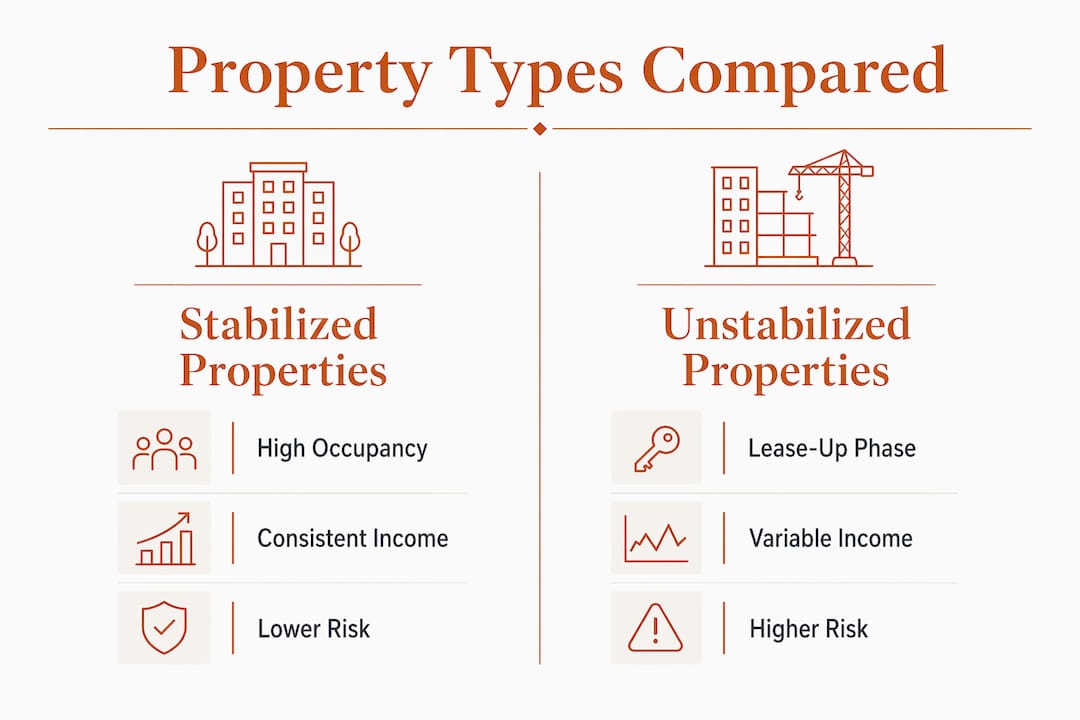

How does a stabilized property differ from value-add and unstabilized assets?

The distinction between stabilized and non-stabilized properties is primarily a question of risk and execution. Stabilized assets reduce execution risk because investors focus on collecting predictable returns rather than solving construction, leasing, or management problems. Value-add and unstabilized properties offer higher potential returns but require active work to get there.

An unstabilized property is typically a new development still in its lease-up phase, a recently acquired asset with high vacancy, or a property recovering from deferred maintenance. The income is uncertain. The expenses are often elevated. Lenders treat these assets as higher risk and price their loans accordingly.

A value-add property occupies the middle ground. It may have acceptable occupancy but below-market rents, outdated units, or management inefficiencies that suppress NOI. The investor's thesis is to close that gap through capital improvements and better operations. Once the improvements are complete and the new rents are in place and sustained, the property can cross into stabilized territory.

| Property Type | Occupancy | Income Predictability | Financing Type | Investor Risk |

|---|---|---|---|---|

| Stabilized | 90%+ for 6–12 months | High, normalized NOI | Permanent loans | Low to moderate |

| Value-add | 70–89%, below-market rents | Moderate, improving | Bridge loans | Moderate |

| Unstabilized | Below 70% or lease-up | Low, variable | Construction or bridge | High |

The financing implications of this table are significant. Lenders prefer stabilized properties for permanent financing because reliable income reduces default risk. That preference translates directly into lower interest rates and better loan terms for investors who hold stabilized assets. Understanding short-term real estate loans and how they transition to permanent financing is a critical part of any development or acquisition strategy.

What operational features keep a property stabilized?

Stabilization is not a permanent label. It is a performance condition that must be actively maintained. A property can lose stabilized status if management neglects operations, vacancies rise unexpectedly, or tenant quality deteriorates. The operational discipline required to maintain stabilization is what separates professional operators from casual landlords.

Four operational practices define a well-maintained stabilized asset:

- Predictable expense management. Operating budgets should reflect actual historical costs, not aspirational projections. Utilities, insurance, property taxes, and maintenance costs must be tracked monthly and benchmarked against prior periods.

- Lease stability and tenant retention. High turnover destroys NOI through vacancy loss, leasing commissions, and tenant improvement costs. Proactive lease renewals, ideally starting 6 to 9 months before expiration, protect occupancy continuity.

- Standardized leasing and maintenance protocols. Consistent lease terms, clear maintenance response standards, and documented inspection schedules reduce surprises and support lender confidence during due diligence.

- Estoppel certificate management. Estoppel certificates signed by tenants confirm lease terms and rent payment status. Lenders require them before closing permanent loans. Operators who maintain current estoppels move through financing faster and with fewer complications.

Pro Tip: Build estoppel certificate collection into your annual lease administration calendar, not just your financing checklist. Current estoppels signal to any future lender or buyer that your operation is professionally managed.

The connection between operational discipline and investor equity is direct. Every dollar of unnecessary expense or preventable vacancy reduces NOI, which reduces property value under the income approach. Operators who treat stabilization as an ongoing practice, not a one-time achievement, protect both their cash flow and their asset's appraised value.

How does stabilization affect valuation and financing?

Stabilization unlocks the most favorable valuation and financing conditions available in commercial real estate. The standard method for valuing a stabilized asset is direct capitalization. Direct capitalization divides trailing 12 months NOI by the market cap rate to produce a value. For example, a property generating $500,000 in NOI at a 5.5% cap rate is valued at approximately $9.1 million. That math only works cleanly when NOI is stable and predictable.

Unstabilized properties require a different approach, typically a discounted cash flow model that accounts for the lease-up period, projected rent growth, and capital expenditure assumptions. Those projections introduce subjectivity and risk, which lenders price into their terms.

The financing transition that stabilization enables is one of the most financially significant events in a property's lifecycle. Stabilization triggers the shift from short-term bridge or construction loans to lower-interest permanent financing. Bridge loans typically carry higher rates and shorter terms. Permanent loans offer fixed rates, longer amortization, and lower debt service. That shift directly improves cash-on-cash returns for investors.

Key financing considerations for stabilized properties:

- Loan-to-value ratios improve when stable NOI supports a higher appraised value. Understanding LTV ratio calculations helps investors model their equity position before and after refinancing.

- Debt service coverage ratios are easier to satisfy with consistent NOI, reducing lender scrutiny.

- Estoppel certificates serve as legal verification of income, giving lenders confidence that the rent roll is accurate and enforceable.

- Cap rate sensitivity means that even a small improvement in NOI or a slight compression in cap rates produces a meaningful increase in property value at stabilization.

The practical implication for investors is clear. Reaching stabilization is not just an operational milestone. It is a financial event that changes the cost of capital, the appraised value, and the return profile of the entire investment.

Key Takeaways

A stabilized property is defined by sustained occupancy at 90% or higher, consistent NOI, and normalized operations, and those three factors together determine its financing eligibility and investment value.

| Point | Details |

|---|---|

| Occupancy threshold | 90% or higher over 6–12 months is the standard; 80% for one quarter applies in some markets. |

| Economic vs. physical occupancy | In-place rents must reflect market rates, not just unit count, to confirm true stabilization. |

| Stabilization can be lost | Poor management, rising vacancies, or deferred maintenance can strip a property of its stabilized status. |

| Valuation method | Direct capitalization on trailing 12 months NOI is the standard approach for stabilized assets. |

| Financing advantage | Stabilization triggers the shift from bridge or construction loans to lower-cost permanent financing. |

Why stabilization is more fragile than most investors realize

I have reviewed enough deals to know that stabilization gets treated as a finish line when it is actually a baseline. Investors buy a stabilized asset, assume the work is done, and then watch occupancy drift or expenses creep up over the next 18 months. The property does not fail dramatically. It just quietly loses the conditions that made it attractive.

The risk I see most often is false stabilization, where a seller has pushed occupancy up with below-market leases or free rent concessions to hit the 90% threshold before listing. The rent roll looks full. The NOI looks acceptable. But when those leases roll over, the income drops and the new owner is left managing a lease-up they did not price into their acquisition.

My advice to any investor evaluating a stabilized asset: pull the actual lease expiration schedule and map it against your hold period. If 40% of leases expire in year two, you are not buying a stabilized property. You are buying a value-add deal at a stabilized price. That is a bad trade.

Seasoned developers use stabilization strategically. They build or reposition an asset, achieve stabilization, refinance into permanent debt, and then either hold for cash flow or sell at a premium. The stabilization event is the value creation moment, not the acquisition. New investors who understand this cycle can use it to their advantage, but only if they verify stabilization rigorously rather than accepting it at face value.

— Brian

Financing your stabilized property acquisition with Gannlending

Acquiring or refinancing a stabilized property requires a lender who understands asset performance, not just credit scores.

Gannlending specializes in hard money loans for real estate investors, with funding available in as few as 5 to 7 business days and financing up to 75% LTV across residential and commercial properties. With over $50 million funded, Gannlending focuses on the asset's income and condition rather than lengthy paperwork processes. Whether you are acquiring a stabilized multifamily property, refinancing after a successful lease-up, or protecting an asset from foreclosure, Gannlending provides the speed and flexibility that traditional lenders cannot match. Reach out to discuss your stabilized property financing needs today.

FAQ

What is the standard occupancy rate for a stabilized property?

A stabilized property typically maintains 90% occupancy or higher over a 6 to 12 month period. In some asset classes or softer markets, 80% occupancy sustained for one full calendar quarter may qualify.

What makes a property stabilized vs. unstabilized?

A stabilized property has consistent occupancy, market-rate rents, normalized operating expenses, and no major capital improvements pending. An unstabilized property lacks one or more of those conditions, usually due to lease-up activity or deferred maintenance.

Can a stabilized property lose its status?

Yes. Stabilization is a performance condition, not a permanent designation. Rising vacancies, poor management, or deferred maintenance can cause a property to fall below stabilization thresholds.

How does stabilization affect property value?

Lenders and appraisers use direct capitalization on trailing 12 months NOI to value stabilized properties. A $500,000 NOI at a 5.5% cap rate produces a $9.1 million valuation, a calculation that only holds when income is stable and predictable.

What are estoppel certificates and why do they matter?

Estoppel certificates are legal documents signed by tenants confirming their lease terms and rent payment status. Lenders require them before closing permanent loans on stabilized properties to verify that the rent roll is accurate and enforceable.