Equity in real estate is defined as the difference between a property's current market value and the total amount of secured debt owed against it. If your home is worth $300,000 and you owe $180,000 on your mortgage, your equity equals $120,000. That number represents your actual ownership stake in the property. For homeowners, it is a measure of personal wealth. For investors, it is the foundation of every financing and exit strategy.

What is equity in real estate and how is it calculated?

Equity is calculated using one straightforward formula: Equity = Market Value minus Total Secured Debts. Total secured debts include your primary mortgage, any home equity line of credit (HELOC), and all other liens on the property. Leaving out a second lien or a tax lien will overstate your equity and lead to bad financial decisions.

Where market value comes from

Market value is the largest variable in any equity calculation. You can estimate it using online tools like Zillow's Zestimate, a comparative market analysis from a licensed real estate agent, or a formal appraisal. Appraisals are the most accurate, but estimated vs. appraised value can differ significantly. A $30,000 gap between an online estimate and a formal appraisal is common in fast-moving markets.

A practical calculation example

The table below shows how equity and equity percentage are calculated at different property values and debt levels.

| Scenario | Market Value | Total Debt | Equity | Equity % |

|---|---|---|---|---|

| New buyer (5% down) | $400,000 | $380,000 | $20,000 | 5% |

| Mid-loan homeowner | $400,000 | $280,000 | $120,000 | 30% |

| Long-term owner | $500,000 | $100,000 | $400,000 | 80% |

| Underwater property | $300,000 | $320,000 | ($20,000) | Negative |

Equity percentage matters as much as the dollar figure. Lenders, appraisers, and investors all use it to assess financial risk and borrowing capacity.

Pro Tip: To calculate your equity percentage, divide your equity by the market value and multiply by 100. A $120,000 equity stake on a $300,000 property equals 40% equity.

What factors influence real estate equity growth or decline?

Equity is not static. It moves up and down based on forces both inside and outside your control.

- Principal repayment. Every mortgage payment you make reduces your loan balance. That reduction directly increases your equity. Early in a standard amortized loan, most of your payment covers interest, so equity builds slowly. It accelerates in later years.

- Property appreciation. When market values rise, your equity grows even if you never make an extra payment. U.S. homeowner equity rose from $8.97 trillion in 2010 to approximately $34.89 trillion in 2024. That growth was driven almost entirely by appreciation, not paydown.

- Property improvements. Renovations like kitchen upgrades, bathroom remodels, or adding square footage can increase market value. Not every dollar spent returns a dollar in equity, but high-ROI improvements consistently add value.

- Market depreciation. Property values can fall. When they fall faster than you pay down your mortgage, equity shrinks. Negative equity occurs when your total debt exceeds the property's market value. Lenders call this being "underwater," and it blocks refinancing and most borrowing options.

- Down payment as starting equity. Your initial down payment is your first equity contribution. A 20% down payment on a $400,000 home creates $80,000 in equity on day one.

Pro Tip: Treat your mortgage payments as forced savings. Each payment builds equity you can access later through refinancing, a home equity loan, or a sale.

Home equity growth through principal repayment and appreciation is the primary reason real estate remains one of the most reliable wealth-building tools available to individual investors.

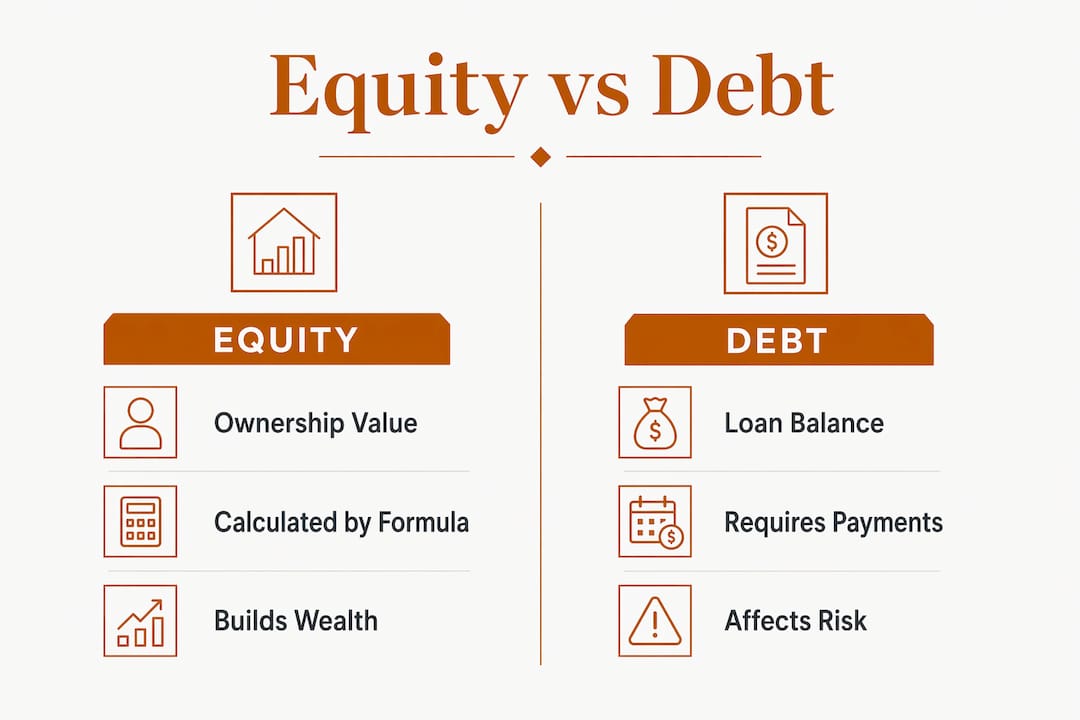

What is the difference between equity and debt in real estate?

Equity and debt are two sides of the same balance sheet. Debt is what you owe. Equity is what you own. Understanding how they interact determines how much financial flexibility you actually have.

| Feature | Equity | Debt |

|---|---|---|

| Definition | Ownership value in the property | Outstanding loan balance secured by the property |

| Nature | Asset (illiquid wealth) | Liability |

| Growth | Increases with paydown and appreciation | Decreases as you make payments |

| Access | Requires selling or borrowing | Already deployed as loan proceeds |

| Risk | Can shrink if values fall | Fixed obligation regardless of market |

Equity is illiquid wealth on paper. You cannot spend it directly. Converting it to cash requires either selling the property or taking on new debt in the form of a home equity loan, HELOC, or cash-out refinance. That conversion always carries costs and risks.

Lenders impose strict limits on how much equity you can borrow against. Most require you to maintain at least 20% equity after any new borrowing. For a $500,000 home, that means the combined loan-to-value across all loans cannot exceed $400,000. Lenders use the combined loan-to-value (CLTV) ratio to enforce this threshold. Understanding CLTV is critical before you apply for any equity-based financing.

Pro Tip: Before applying for a home equity loan or HELOC, calculate your CLTV by adding all existing loan balances and dividing by the current market value. Staying below 80% CLTV gives you the best rates and approval odds.

How can you practically use real estate equity?

Equity is only valuable if you know how to use it. Homeowners and investors have several options for converting paper wealth into working capital.

- Home equity loans. A lump-sum loan secured by your property. The interest rate is fixed, and you repay it in monthly installments. Best for one-time expenses like a renovation or debt consolidation.

- HELOCs. A home equity line of credit works like a credit card secured by your property. You draw funds as needed during a set draw period. Rates are typically variable. Best for ongoing expenses or projects with uncertain costs.

- Cash-out refinancing. You replace your existing mortgage with a larger one and pocket the difference. This resets your loan term and rate. It is the most common way investors pull equity out to fund new acquisitions. For time-sensitive situations, emergency refinancing options can move faster than traditional bank timelines.

- Selling the property. The most complete conversion of equity to cash. You pay off all liens, cover closing costs and commissions, and keep the net proceeds. Realizable equity after a sale is always lower than nominal equity because closing costs, agent commissions, and potential tax obligations reduce your net proceeds.

- Private lending and hard money loans. Investors who need fast access to equity-based financing often turn to private lenders. These lenders focus on the asset value rather than credit history or income documentation, which speeds up the process significantly.

Borrowing against equity exchanges ownership stake for debt. That trade increases your financial risk if property values fall or if income disruptions make payments difficult. Always maintain an equity cushion large enough to absorb a market correction without going underwater.

Key takeaways

Real estate equity is the ownership value you hold in a property, and managing it deliberately is the difference between building wealth and taking on unnecessary risk.

| Point | Details |

|---|---|

| Core definition | Equity equals market value minus all secured debts, including every lien on the property. |

| Equity grows two ways | Principal repayment and property appreciation both increase your ownership stake over time. |

| Negative equity is real | When debt exceeds market value, you lose access to refinancing and most borrowing options. |

| Lenders cap borrowing at 80% LTV | Most lenders require you to retain at least 20% equity after any new loan is added. |

| Conversion always has costs | Selling or borrowing against equity involves closing costs, commissions, and potential tax obligations that reduce net proceeds. |

Why most people misread their own equity position

I have seen homeowners walk into financing conversations with a confident equity number in their head, only to discover the real figure is $40,000 lower than they thought. The gap almost always comes from two sources: an inflated online value estimate and a forgotten second lien or unpaid tax assessment.

The online estimate problem is underappreciated. Automated valuation models like Zillow's Zestimate are useful for a quick ballpark, but they do not account for deferred maintenance, neighborhood micro-trends, or recent interior upgrades. In markets where prices move fast, a six-month-old algorithm estimate can be off by 5–10%. On a $600,000 property, that is a $30,000–$60,000 error in your equity calculation.

The second issue is that people treat equity as a fixed number rather than a range. Your equity is only as accurate as your most recent market value estimate. I recommend getting a formal broker price opinion or a full appraisal before making any major equity-based decision, whether that is a refinance, a home equity loan, or a sale.

The broader point is this: equity is your most valuable financial asset in real estate, but it is also the most frequently miscalculated one. Treat it with the same rigor you would apply to any other balance sheet item. Review it annually, account for every lien, and get a professional valuation before you act on it.

— Brian

Access your real estate equity faster with Gannlending

Real estate equity is only useful when you can access it on your timeline, not a bank's.

Gannlending specializes in private hard money loans that let homeowners and investors tap into property equity without the delays of traditional lenders. Gannlending focuses on the asset value rather than stacks of paperwork, with funding available in as few as 5–7 business days. With financing up to 75% LTV across residential and commercial properties, and over $50 million funded, Gannlending is built for investors who need to move fast. If you are sitting on equity and need capital now, explore your options at Gannlending.

FAQ

What is the simple definition of equity in real estate?

Equity in real estate is the difference between a property's current market value and the total amount of secured debt owed on it. It represents the portion of the property the owner actually controls free of lender claims.

How do you calculate your home equity percentage?

Divide your equity dollar amount by the property's market value, then multiply by 100. A $120,000 equity stake on a $300,000 home equals 40% equity.

What is negative equity in real estate?

Negative equity occurs when the total debt secured by a property exceeds its market value. This is also called being "underwater" and it blocks most refinancing and borrowing options.

What is the difference between equity and debt in real estate?

Debt is the outstanding loan balance you owe to lenders. Equity is the ownership value you hold above that debt. Debt is a liability; equity is an asset, though an illiquid one until you sell or borrow against it.

How much equity do lenders typically require you to keep?

Most lenders require you to retain at least 20% equity after any new borrowing. For a $500,000 property, that means total loans across all liens cannot exceed $400,000.