A short term note in real estate is a legally binding, asset-backed debt instrument that provides financing for property transactions over a period ranging from a few months up to two years. These instruments, formally called real estate notes or mortgage notes, sit at the core of private lending markets. Hard money loans, bridge loans, and promissory notes all fall under this category. Investors use them to fund fix-and-flip projects, construction draws, and acquisitions where conventional bank timelines would kill the deal. With short term note real estate explained clearly, you can decide whether these instruments belong in your portfolio.

What types of short term notes are common in real estate?

Three instruments dominate the short term financing space: hard money loans, bridge loans, and promissory notes. Each serves a distinct purpose and carries different terms, rates, and underwriting logic.

Hard money loans

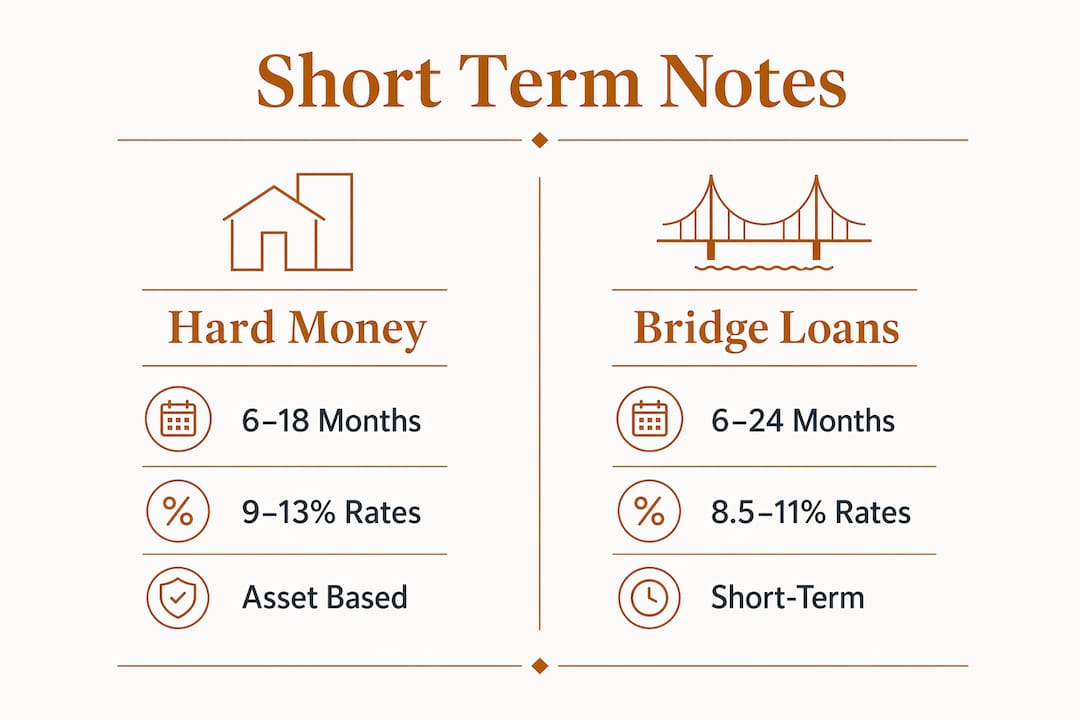

Hard money loans are asset-based loans with terms of 6–18 months, interest rates of 9–13% in 2026, and funding timelines of 7–15 business days. The lender underwrites the deal based on the property value, not the borrower's tax returns. Standard loan-to-value ratios reach up to 75%. That speed and flexibility make hard money the go-to tool for fix-and-flip investors who need to close before a competing cash buyer does.

Bridge loans

Bridge loans carry terms of 6–24 months, with 12 months being the most common. Rates typically run 8.5–11%, and LTV ranges from 55% to 75%. Payments are interest-only each month, with the full principal due as a balloon at maturity. Bridge loans close in 5–15 business days versus 60–90 days for conventional loans. That speed advantage is the main reason investors use them for distressed auctions and time-sensitive acquisitions.

Promissory notes

A promissory note is the legal written promise to repay a loan. It is a separate document from the mortgage, which only secures the debt against the property. Commercial promissory notes commonly mature in 7 days to 1 year. The note specifies the interest rate, payment schedule, and default terms. When investors talk about "buying a note," they mean purchasing the right to receive the payments described in this document.

Side-by-side comparison

| Instrument | Typical term | Rates | Max LTV | Payment structure |

|---|---|---|---|---|

| Hard money loan | 6–18 months | 9–13% | 75% | Monthly interest + balloon |

| Bridge loan | 6–24 months | 8.5–11% | 75% | Interest-only + balloon |

| Promissory note | 7 days–1 year | Negotiated | Varies | Per note terms |

How do investors benefit from short term real estate notes?

Mortgage note investing provides regular income without the operational burden of owning physical property. No tenant calls, no maintenance bills, no vacancy risk. That operational simplicity is the feature most investors underestimate until they have managed both a rental portfolio and a note portfolio side by side.

The core benefits break down as follows:

- Monthly income. Interest payments arrive on a fixed schedule for the life of the note, creating predictable cash flow.

- Portfolio diversification. You can hold notes on properties across multiple states without traveling to inspect them, which is far harder to do with direct ownership.

- Lower capital concentration. Spreading $500,000 across ten notes reduces exposure to any single borrower or market compared to buying one property outright.

- Higher yields than conventional fixed income. Short term real estate notes routinely yield well above Treasury bonds or investment-grade corporate debt.

- Faster capital recycling. A 12-month note returns your principal quickly, letting you redeploy into the next deal.

Typical investors suited for these notes include self-directed IRA holders, private lenders, family offices, and active real estate investors looking to balance active flipping income with passive note income.

Pro Tip: Always check the lien position before you buy. First-position notes give you priority recovery rights in a default. Junior liens can be wiped out entirely in foreclosure, leaving you with nothing.

What risks and underwriting factors should investors know?

Short term notes carry real risks. Understanding them before you commit capital is the difference between a profitable portfolio and an expensive lesson.

The key risk factors are:

- Borrower payment ability. A note is only as good as the borrower's ability to service it. Verify income, credit, and exit strategy before funding.

- Collateral value. The property secures your capital. An inflated appraisal or a declining market can leave you underwater if you need to foreclose.

- Liquidity. Notes are not publicly traded. Selling a note before maturity requires finding a private buyer, which takes time and often means accepting a discount.

- Legal and servicing complexity. Note servicing companies manage payments, escrow accounts, and legal compliance. Skipping professional servicing is a common and costly mistake.

- LTV and exit strategy. A borrower with a clear exit, such as a refinance or sale, is far less likely to default than one with no plan for repaying the balloon.

Lien position is the single most important structural factor in capital protection. First-lien holders foreclose and recover ahead of all junior creditors. Junior lien investors often recover nothing in a distressed sale. The yield premium on a second-lien note rarely compensates for that risk.

Pro Tip: Closing speed is often the deciding factor in winning a deal. Have your proof of funds ready and your scope of work documented before you approach a lender. Deals fall apart when investors show up unprepared.

You can explore short-term loan types in more detail to match the right instrument to your specific project.

How can investors source and evaluate short term real estate notes?

Sourcing quality notes requires knowing where to look and what to check once you find one. The market is fragmented, which creates opportunity for prepared investors.

- Source directly from private lenders. Hard money lenders like Gannlending originate notes and sometimes sell performing loans to free up capital. Building a direct relationship gives you first access.

- Work with note brokers. Brokers aggregate notes from multiple originators and present them with basic due diligence already completed. Expect to pay a spread.

- Use note marketplaces. Platforms focused on private debt connect buyers and sellers of performing and non-performing notes. Inventory varies by market cycle.

- Evaluate the interest rate and discount. Investor returns depend on both the stated interest rate and the price paid relative to the unpaid principal balance. Buying a note at a discount amplifies your effective yield.

- Check documentation quality. A note without a properly recorded mortgage, a clear title, and a signed promissory note is not a secure investment. Verify every document before wiring funds.

- Assess the exit strategy. Ask how the borrower plans to repay the balloon. A fix-and-flip borrower with a signed purchase contract is a stronger credit than one with no buyer in sight.

Real wealth built through debt instruments comes from consistent underwriting discipline, not from chasing the highest stated yield. Investors who skip documentation checks or ignore lien position for an extra point of interest tend to learn that lesson expensively.

Direct individual note investing requires hands-on due diligence. Managed note funds handle sourcing, underwriting, and servicing for you, but they take a fee and reduce your control. New investors often benefit from starting with a fund before moving to direct deals.

Pro Tip: Before committing to any note, verify the lender's track record. Ask for a sample loan file, check state licensing, and confirm the servicing arrangement. A lender who cannot answer those questions quickly is a red flag.

You can also review fast-funding strategies to understand how top investors structure deals to close before competitors.

Key Takeaways

Short term real estate notes are asset-backed debt instruments that deliver monthly income, faster capital recycling, and lower operational burden than direct property ownership, provided investors prioritize first-lien position and thorough due diligence.

| Point | Details |

|---|---|

| Know your instrument | Hard money loans, bridge loans, and promissory notes each carry different terms, rates, and underwriting logic. |

| Lien position determines safety | First-lien notes give priority recovery rights; junior liens risk total loss in foreclosure. |

| Speed wins deals | Closings in 5–15 business days beat conventional loans and let investors capture time-sensitive opportunities. |

| Due diligence is non-negotiable | Verify borrower exit strategy, collateral value, documentation quality, and servicing arrangements before funding. |

| Yield depends on purchase price | Buying a note at a discount to unpaid principal balance increases your effective return beyond the stated rate. |

Why I think most investors overlook the best part of note investing

Most real estate investors I talk to think of notes as a passive fallback, something you do when you cannot find a good property to buy. That framing misses the point entirely.

The real advantage of short term notes is not just the income. It is the underwriting clarity. When you own a property, your return depends on dozens of variables: tenant behavior, maintenance costs, local vacancy rates, and market timing. When you hold a well-structured first-lien note, your return depends on one thing: whether the borrower repays. That simplicity is genuinely powerful for investors who want predictable outcomes.

My strong view is that new investors should start with senior-secured, first-lien notes before touching anything junior. The yield difference rarely justifies the structural risk. I have seen experienced investors lose significant capital on second-lien positions that looked attractive on paper but were wiped out in a straightforward foreclosure.

The market right now favors note investors who can move fast. Borrowers increasingly prefer private lenders over banks because of speed, not rate. That means well-capitalized note investors with a clear process can pick the best deals. The investors who struggle are the ones who take weeks to make a decision on a deal that needs an answer in 48 hours.

Build your due diligence process before you need it. Know your checklist, know your servicing partner, and know your lien position requirements. When a good note crosses your desk, you will be ready to act.

— Brian

How Gannlending can fund your next short term deal

Real estate investors who need fast, asset-based financing have a direct path through Gannlending. Gann Private Lending has funded over $50 million in hard money loans, closing deals in as few as 5–7 business days with no appraisal required. Financing covers up to 75% LTV on residential and commercial properties, with rates in the 9–13% range.

Whether you are funding a fix-and-flip, a bridge position, or a rehab project, Gannlending focuses on the asset, not the paperwork. Investors facing time-sensitive acquisitions or foreclosure situations get the same fast-close process. Visit Gannlending to explore hard money loan options and get your deal funded before the opportunity closes.

FAQ

What is a short term note in real estate?

A short term real estate note is a legally binding debt instrument secured by property, typically maturing in a few months to two years. Common examples include hard money loans, bridge loans, and promissory notes used for acquisitions, renovations, and construction.

How do hard money loans differ from bridge loans?

Hard money loans run 6–18 months at 9–13% and focus on asset value for underwriting. Bridge loans run 6–24 months at 8.5–11% and are commonly used to bridge a financing gap between purchase and permanent financing.

What does lien position mean for note investors?

Lien position determines who gets paid first if a borrower defaults. First-lien note holders have priority recovery rights in foreclosure, while junior lien holders can be wiped out entirely if the sale proceeds do not cover all debts.

How fast can short term real estate notes close?

Hard money and bridge loans close in 5–15 business days when the borrower has proof of funds and documentation ready. That compares to 60–90 days for conventional bank financing.

Where can investors buy real estate notes?

Investors source notes directly from private lenders, through note brokers, and on private debt marketplaces. Evaluating the lien position, documentation quality, and borrower exit strategy before purchase is critical to protecting your capital.