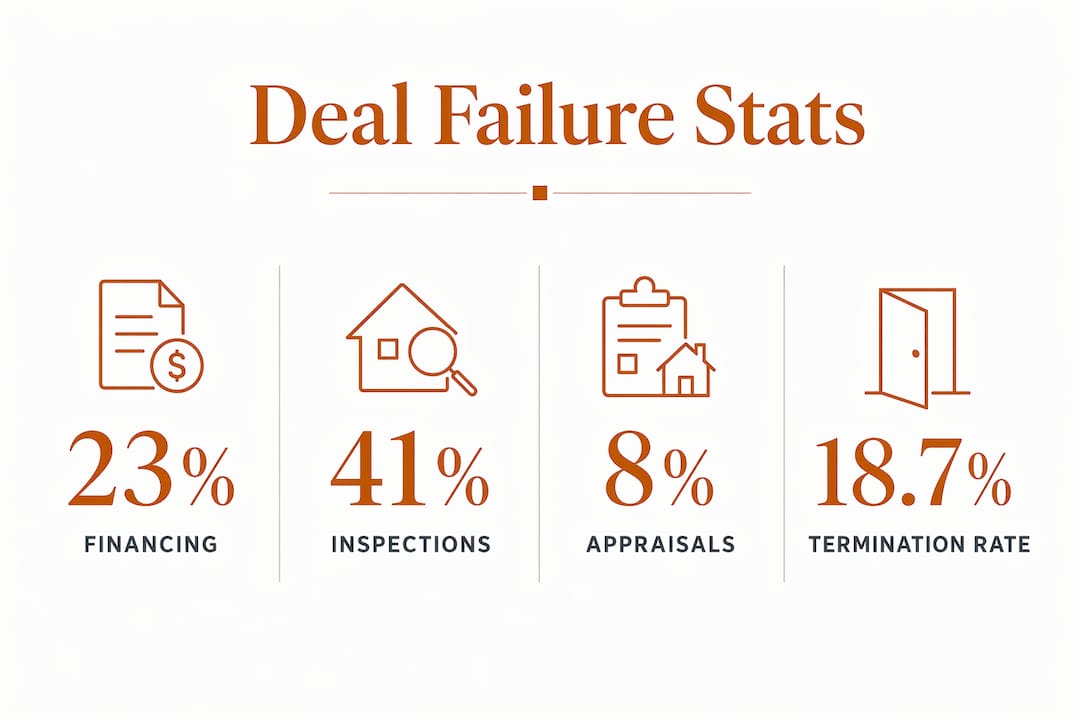

Financing failures, inspection disputes, appraisal gaps, and title defects are the four primary reasons why real estate deals fall through before closing. The contract termination rate surged to 18.7% in 2025–2026, compared to a historical average of just 4–6%. That shift represents a structural change in how transactions collapse, not a temporary blip. For real estate professionals and investors, understanding each failure point with precision is the difference between a closed deal and a lost commission or capital.

Why real estate deals fall through at the financing stage

Mortgage financing is the single most common reason property sales collapse before closing. Mortgage rate volatility accounts for 23% of all contract cancellations in 2026. That number reflects how quickly a qualified buyer can become an unqualified one when rates move.

The math is unforgiving. A 0.5% rate increase raises monthly payments by more than $300 on a $500,000 mortgage. That single shift can push a buyer's debt-to-income ratio past the lender's threshold, triggering automatic disqualification. Many buyers who were pre-approved at the time of offer are no longer financeable by the time closing arrives.

Rate-lock expirations compound the problem. When a transaction drags past the lock period, the buyer must re-lock at current rates. If the market has moved against them, the new payment may no longer fit their budget. Deals that take 60 or 90 days to close are especially exposed to this risk.

Buyer financial changes during escrow are another underappreciated threat. A job change, a new car loan, or even a credit card application can alter a buyer's credit profile enough to trigger underwriting rejection. Lenders re-verify employment and credit shortly before closing, and surprises at that stage are almost always fatal to the transaction.

- Rate-lock expiration forces re-pricing at current market rates

- Debt-to-income ratio changes from new debt or income loss

- Credit score drops from new inquiries or missed payments

- Employment changes flagged during final underwriting verification

- Appraisal shortfalls reducing the loan amount the lender will approve

Pro Tip: Advise buyers to freeze all financial activity from contract signing through closing. No new credit, no job changes, no large purchases. Pair this with a rate-lock strategy that extends at least 15 days beyond the expected closing date to absorb delays.

What role do home inspections play in deal failures?

Inspection-related issues cause approximately 41–42% of contract renegotiations or terminations in 2026. That makes the home inspection the single largest deal-killer by category. Structural defects, roof failures, and mold findings are the most common triggers for buyer withdrawal or aggressive price renegotiation.

The inspection contingency has evolved into something more strategic than its original purpose. Buyers in 2026's buyer's market now use inspections as consequence-free exits. A buyer who develops cold feet after signing can commission an inspection, cite any finding as justification, and walk away with their earnest money intact. This behavior is increasingly common and increasingly difficult for sellers to counter.

Seller-performed repairs create a separate and serious risk. DIY or unverifiable repairs can invalidate contracts at closing. Licensed contractor invoices are not optional documentation. They are the legal evidence that a repair was completed to code and by a qualified professional. Without them, a buyer's attorney can argue the repair condition was not satisfied.

Here are the inspection findings most likely to kill a deal outright:

- Foundation cracks or structural movement indicating active settlement

- Roof damage requiring full replacement rather than patch repair

- Active mold growth in attic, crawl space, or HVAC systems

- Outdated or unsafe electrical panels such as Federal Pacific or Zinsco brands

- Plumbing failures including polybutylene pipe systems or active leaks

- Evidence of unpermitted additions or structural modifications

Pro Tip: Sellers should complete a pre-listing inspection before going to market. Addressing major findings in advance removes the buyer's leverage and eliminates the surprise factor that causes deals to collapse. Always use licensed contractors and retain every invoice.

How do appraisal gaps disrupt real estate transactions?

Appraisal problems contribute to roughly 8% of failed transactions, a figure that understates the psychological damage appraisal gaps cause during escrow. When an appraiser values a property below the agreed purchase price, the lender will only finance based on the appraised value. The buyer must cover the difference in cash or renegotiate.

The table below outlines the three paths available when an appraisal comes in low:

| Scenario | Buyer Action | Seller Action | Likely Outcome |

|---|---|---|---|

| Appraisal gap is small | Covers gap in cash | Holds firm on price | Deal closes |

| Appraisal gap is large | Requests price reduction | Accepts or counters | Renegotiation or cancellation |

| Both parties refuse to move | Exercises appraisal contingency | Relists property | Deal collapses |

In a market where values are declining slowly, appraisers often lag behind the price drops. A property under contract for 45 days may appraise at a value that reflects conditions from two months ago. That creates a gap between what the market now supports and what the buyer agreed to pay. Sellers who refuse to adjust face cancellation. Buyers who refuse to cover the gap lose the deal.

Investors who need to close deals fast despite appraisal challenges often turn to asset-based lending, which bypasses the traditional appraisal requirement entirely. That approach removes one of the most unpredictable variables from the transaction timeline.

Why do title issues and communication failures derail closings?

Title defects from multi-generational ownership, missing signatures, or undisclosed heirs often surface late in the transaction, disrupting closings at the worst possible moment. Inherited properties and estate sales carry the highest risk. A missing heir, an unrecorded deed, or a lien from a deceased owner's creditor can halt a closing and require weeks of legal resolution. Buyers who are unwilling to wait simply cancel.

Poor communication among agents, lenders, and title companies is a silent deal-killer that professionals consistently underestimate. Failures to notify relevant parties of contract changes create compounding problems within the critical 48 hours before closing. A missed addendum, an unacknowledged extension request, or a lender condition that was never relayed to the buyer's agent can unravel a transaction that was otherwise ready to close.

Documentation errors add another layer of risk. A mismatch between a buyer's legal ID and their loan application name, including post-marriage name changes not updated on official records, can stall underwriting in the final days. Even minor discrepancies trigger compliance flags that lenders cannot ignore.

Insurance discovery problems are less discussed but equally damaging. A buyer who cannot obtain homeowner's insurance on a property due to prior claims history, roof age, or flood zone designation may lose financing entirely. Discovering this on the day before closing leaves no time to resolve it.

- Conduct a title search within the first week of contract, not at the end

- Require all parties to confirm receipt of every contract amendment in writing

- Verify buyer ID matches loan application name at the pre-approval stage

- Order homeowner's insurance quotes within the first 10 days of escrow

- Use a shared transaction management platform so all parties see the same document timeline

Pro Tip: Establish a written communication protocol at the start of every transaction. Every update, every condition, every extension goes to all parties simultaneously. This single practice eliminates the majority of last-minute closing failures caused by information gaps.

How do buyer behavior and market conditions influence deal failures?

Buyer psychology is a direct factor in why property sales collapse, and the 2026 market has amplified every hesitation. Economic uncertainty, mortgage rate swings, and declining home values in certain metros have created a buyer population that is more willing to walk away than at any point in recent history. Cold feet are no longer rare. They are a predictable part of the transaction cycle.

In a buyer's market, the power dynamic shifts decisively. Buyers know that inventory is available and that sellers have limited leverage. This knowledge makes it easier to exit a contract without guilt. Inspection contingencies, appraisal contingencies, and financing contingencies all provide legal off-ramps. Buyers in 2026 are using all of them more aggressively than in prior years, as cash offers increasingly skip the contingency process entirely to compete.

Recognizing early signs of buyer hesitancy gives professionals the ability to intervene before a deal collapses. Watch for these behavioral signals:

- Delayed response to inspection reports beyond the contractual deadline

- Requests for excessive seller credits that exceed the cost of actual repairs

- Contract extension requests without a clear stated reason

- Sudden interest in comparable listings after going under contract

- Reduced communication frequency from the buyer's agent

Pro Tip: When you spot hesitancy signals, address them directly and early. A frank conversation about the buyer's concerns is far less costly than a failed closing. Offer to walk through the inspection report together and separate cosmetic issues from genuine deal-breakers.

Key takeaways

Failed real estate transactions in 2026 are driven by financing volatility, inspection disputes, appraisal gaps, and title or communication failures, each requiring a distinct prevention strategy.

| Point | Details |

|---|---|

| Financing is the top risk | Mortgage rate changes account for 23% of cancellations; lock rates early and freeze buyer finances. |

| Inspections drive most failures | Approximately 41–42% of deal failures trace to inspection findings; pre-listing inspections reduce this risk. |

| Appraisal gaps require a plan | Buyers and sellers need a pre-agreed response strategy before an appraisal comes in low. |

| Title defects need early detection | Order title searches in week one to allow time for legal resolution before closing. |

| Communication is a closing tool | A written protocol for all parties reduces last-minute failures caused by missed information. |

What i've learned after watching hundreds of deals fall apart

The deals I've seen collapse most painfully were not the ones with obvious problems. They were the ones where everyone assumed someone else was handling a critical detail. A lender who thought the agent had confirmed the insurance. An agent who thought the title company had flagged the heir issue. A buyer who thought their rate lock was still valid.

The 18.7% termination rate is not just a market statistic. It reflects a systemic failure of coordination across the transaction chain. Every party operates in their own lane, and the gaps between those lanes are where deals die.

What I tell investors and agents consistently is this: treat every transaction as if it will hit every obstacle simultaneously. Build your timeline assuming the appraisal will come in low, the inspection will surface a major finding, and the buyer's lender will ask for one more document at the worst possible moment. When you plan for all of it, none of it catches you off guard.

The inspection contingency shift is the most underappreciated change in the current market. Buyers are not just using it to address legitimate concerns. They are using it as a structured exit option. Sellers and their agents need to recognize this and negotiate contingency language more carefully from the start.

Document everything. Repair invoices, communication confirmations, extension agreements. The deals that survive are the ones where every party has a paper trail that leaves no room for dispute.

— Brian

How Gannlending helps investors close when traditional deals stall

When financing delays, appraisal disputes, or tight timelines threaten a deal, Gannlending provides a direct path forward. As a private hard money lender focused on asset value rather than borrower paperwork, Gannlending funds deals in as few as 5–7 business days with no appraisal requirement.

That speed and structure eliminates two of the most common deal-killers: appraisal gaps and financing delays. With up to 75% LTV across residential and commercial properties, and over $50 million funded, Gannlending gives investors the credibility and capital to compete against cash buyers and close on their terms. Explore fast funding strategies that keep your deals from falling apart at the finish line.

FAQ

What is the most common reason real estate deals fall through?

Financing failure is the leading cause, with mortgage rate volatility alone accounting for 23% of contract cancellations in 2026. Inspection disputes follow closely, responsible for approximately 41–42% of renegotiations or terminations.

How often do pending real estate deals fall through?

The national contract termination rate reached 18.7% in 2025–2026, a dramatic increase from the historical average of 4–6%. In 2023, roughly 247,500 U.S. transactions failed to reach closing.

Can a deal fall through because of a name mismatch?

Yes. A discrepancy between a buyer's legal ID and their loan application name can halt underwriting in the final days before closing. Even a post-marriage name change not updated on official records is enough to trigger a compliance failure.

How do title defects cause real estate deals to collapse?

Title defects from undisclosed heirs, missing signatures, or unrecorded liens require legal resolution that can take weeks. Buyers unwilling to wait exercise their contingency rights and cancel the contract.

What can investors do to avoid deal failures from appraisal gaps?

Investors can use asset-based hard money lending, which bypasses the traditional appraisal requirement entirely. Alternatively, negotiating an appraisal gap coverage clause into the contract before signing gives both parties a clear resolution path if the appraisal comes in low.