A mixed-use hard money loan is a short-term, privately funded bridge loan secured by a property that combines two or more different use types within the same building. To finance mixed-use development with hard money, developers rely on asset-based underwriting rather than personal credit scores or income verification. These loans fund acquisition, construction, and bridge phases where conventional lenders routinely stall or decline. Speed, flexibility, and collateral focus define the product. Loan-to-value ratios, after-repair value assessments, and clear exit strategies drive approval decisions far more than a borrower's tax returns.

What are the key features of hard money loans for mixed-use developments?

Hard money loan terms typically run 6–36 months, with interest rates between 8–15% or higher depending on project complexity and lender risk appetite. That short window is intentional. The loan is designed to carry a project through its most capital-intensive phase, then get replaced by permanent financing once the property stabilizes.

Several structural features define how these loans work in practice:

- Loan-to-value and loan-to-cost ratios: Construction loans for mixed-use developments typically fund at loan-to-cost ratios of 75–80%, requiring developer equity of 20–25%.

- After-repair value (ARV) underwriting: Lenders base their maximum loan amount on what the completed property will be worth, not its current condition.

- Interest-only payments: Borrowers pay interest only during the loan term, preserving cash flow during construction and lease-up.

- Draw schedules: Funds release in stages as construction milestones are met, reducing lender exposure and keeping the project on track.

- Points and fees: Expect 2–4 origination points upfront, in addition to the interest rate. These costs are the price of speed and flexibility.

- Exit strategy requirement: Every lender wants a credible plan for repayment, whether through property sale or refinance into a conventional commercial mortgage.

Pro Tip: Build your exit strategy before you apply. Lenders evaluate your repayment plan as seriously as the property itself. A clear refinance timeline or signed purchase agreement strengthens your file immediately.

Underwriting for mixed-use projects carries added complexity because lenders must assess multiple income streams: retail leases, residential units, and sometimes office or hospitality components. A lender experienced in mixed-use project financing will evaluate each component's marketability separately, then assess the blended risk.

How do hard money loans support mixed-use projects differently than traditional financing?

Conventional lenders treat mixed-use properties as difficult to categorize. A building with ground-floor retail and upper-floor apartments does not fit neatly into residential or commercial loan programs. That classification problem creates delays, additional documentation requirements, and frequent denials at the underwriting stage.

Hard money lenders solve this by focusing on collateral value and exit strategy rather than detailed credit analysis. This asset-based approach allows financing of properties that do not meet conventional mortgage guidelines due to condition, occupancy, or use complexity.

The speed difference is significant. Hard money loans close in as few as 3–10 business days, while conventional commercial construction loans routinely take 60–90 days or longer. For a developer competing for a site in a supply-constrained urban market, that gap is the difference between winning and losing the deal.

Developers rarely rely on a single financing source for mixed-use projects. Capital layering combines hard money or bridge loans for the acquisition and construction phase, followed by permanent financing once stabilized occupancy reaches 85–95%. Hard money fills the gap that conventional lenders will not touch until the property performs.

| Financing type | Approval basis | Typical close time | Best use case |

|---|---|---|---|

| Hard money loan | Asset value, ARV, exit strategy | 3–10 business days | Acquisition, construction, bridge |

| Conventional commercial loan | Income, credit, occupancy history | 60–90+ days | Stabilized, income-producing property |

| Construction loan (bank) | Project plans, credit, reserves | 30–60 days | Ground-up builds with strong borrower profile |

Pro Tip: Use hard money to acquire and build, then refinance into a conventional commercial mortgage once you hit 85–90% occupancy. That transition is your real exit strategy, and planning it from day one keeps your lender confident throughout the project.

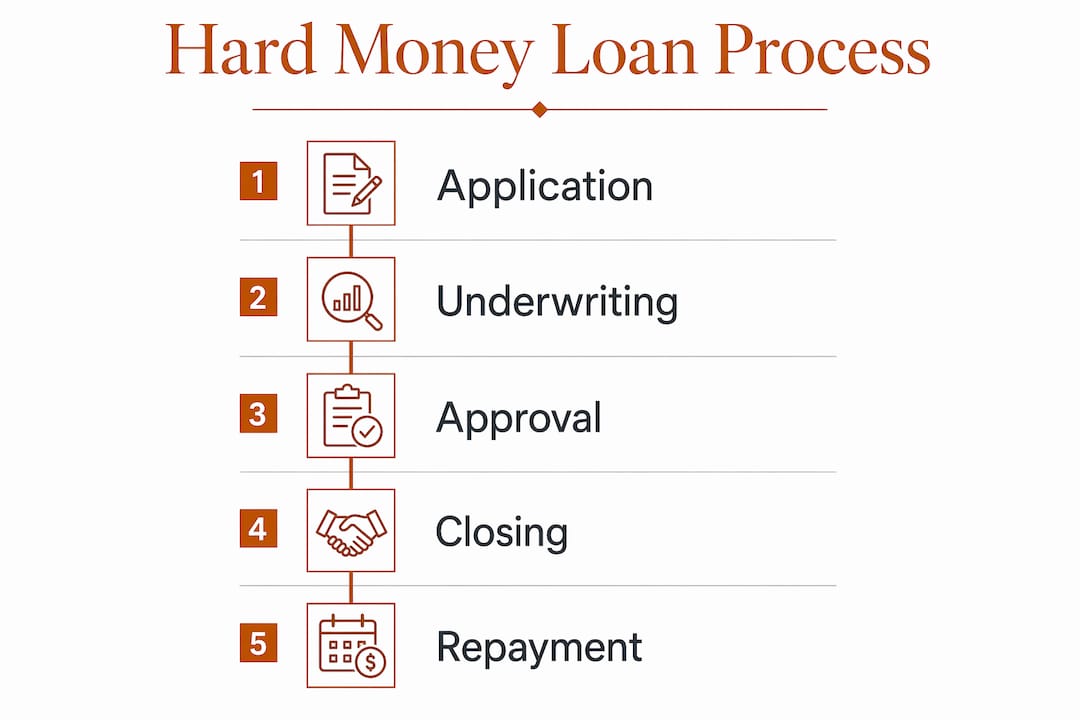

What steps do you need to take to secure a hard money loan for a mixed-use project?

Preparation separates developers who close in a week from those who stall for months. Lenders move fast, but they expect your documentation to be ready before the first conversation.

-

Prepare a detailed project proforma. Your proforma must show projected rents by unit type, vacancy assumptions, operating expenses, and net operating income at stabilization. Realistic numbers build credibility. Inflated projections raise red flags immediately.

-

Assemble a full construction budget. Line-item budgets with contractor bids, contingency reserves, and a draw schedule timeline show lenders you understand the build. A 10–15% contingency line is standard and expected.

-

Document your equity contribution. Lenders require developer equity of 20–25% of total project cost. Bank statements, proof of funds, or a signed equity commitment letter all satisfy this requirement.

-

Gather permits and project plans. Approved permits and architectural drawings confirm the project is shovel-ready or close to it. Lenders price risk based on how far along the entitlement process is.

-

Demonstrate developer experience. A track record of completed mixed-use or commercial projects reduces perceived risk. Provide a portfolio summary with project addresses, costs, and outcomes.

-

Define your exit strategy clearly. State whether you plan to sell, refinance, or hold. If refinancing, identify the target lender type and the occupancy threshold you need to hit.

-

Submit a clean loan package. Thorough documentation including project plans, budgets, permits, proformas, and equity evidence satisfies lender scrutiny and accelerates underwriting.

The underwriting process for a hard money loan on a mixed-use project typically takes 24–72 hours once your package is complete. Closing follows within days. Established borrowers with complete files close even faster because lenders skip the lengthy income verification steps that slow conventional underwriting.

Pro Tip: Call the lender before submitting your package. A five-minute conversation tells you exactly what they want to see and prevents you from submitting an incomplete file that restarts the clock.

What are the main risks of hard money financing for mixed-use developments?

Hard money loans carry real costs and real consequences when projects run long. Understanding these risks before you sign protects both your project and your capital.

- Higher interest costs compress margins. Rates of 8–15% or more accumulate fast on a 12-month construction timeline. Every month of delay adds direct cost to your project budget.

- Short loan terms create refinance pressure. If your project runs over schedule or lease-up takes longer than projected, you may face a maturity date before you qualify for permanent financing.

- Construction cost overruns are common. Material and labor costs shift during a build. A contingency reserve of 10–15% of the construction budget is the standard mitigation tool.

- Lease-up delays affect your exit timeline. Retail tenants in mixed-use buildings often take longer to sign than residential tenants. A slower-than-projected lease-up can push your stabilization date past your loan maturity.

- Liquidity post-closing matters. Lenders want to see that you have reserves beyond the equity contribution. Running out of cash mid-project is the most common cause of hard money loan defaults.

Developers who treat hard money as a permanent solution rather than a bridge tool consistently face the worst outcomes. The loan is designed to be expensive and short. Your job is to execute fast enough that the cost is a small fraction of your total project return, not a drag that erodes your margin. Plan your exit before you close, not after you run into trouble.

Investment risks in mixed-use projects are manageable when you build contingency into both your budget and your timeline. Transparent communication with your lender throughout the project also matters. Lenders who know a project is running slightly long are far more likely to grant a short extension than lenders who learn about problems at maturity.

Key Takeaways

Hard money loans are the fastest and most flexible tool available to finance mixed-use development, but they require a clear exit strategy, realistic proformas, and disciplined liquidity management to succeed.

| Point | Details |

|---|---|

| Asset-based underwriting | Approval depends on property value and ARV, not personal credit or income history. |

| Short loan terms | Terms run 6–36 months; plan your refinance or sale exit before you close. |

| Capital layering works | Use hard money for acquisition and construction, then transition to permanent financing at 85–95% occupancy. |

| Documentation drives speed | Complete files with proformas, budgets, permits, and equity proof close in days, not weeks. |

| Liquidity is non-negotiable | Maintain cash reserves post-closing to cover overruns and protect your refinance timeline. |

What I've learned about using hard money for mixed-use projects

Most developers I talk to make the same mistake: they treat the hard money loan as the finish line instead of the starting block. They close on the acquisition, break ground, and then start thinking about the exit. That sequence is backwards.

The developers who execute well on mixed-use projects treat the permanent financing conversation as part of their pre-closing checklist. They know which bank or agency lender will take out the hard money loan, what occupancy threshold that lender requires, and how long lease-up realistically takes in their submarket. That clarity makes the hard money term feel short because the project is already moving toward the exit from day one.

Proformas also matter more than most developers admit. I have seen lenders pass on strong projects because the numbers looked optimistic without support. A proforma built on actual comparable rents, real contractor bids, and conservative vacancy assumptions tells a lender that you understand your market. That confidence translates directly into faster approvals and better terms.

The other thing worth saying plainly: mixed-use project financing is not a commodity. The lender you choose for a ground-floor retail and upper-floor residential project needs to understand both asset classes. A lender who only knows single-family residential will underwrite your project wrong and price it wrong. Specialize your lender selection the same way you specialize your project.

— Brian

Gannlending: fast hard money for mixed-use developers

Mixed-use projects move fast or they stall. Gannlending specializes in private hard money loans for real estate developers who need capital in days, not months. With closings in as few as 5–7 business days and no appraisal delays, Gannlending focuses on the asset and your exit strategy, not your tax returns. Financing covers up to 75% LTV across residential and commercial property types, with underwriting built for the complexity of mixed-use projects.

Gannlending has funded over $50 million in private real estate loans. If you have a mixed-use acquisition, construction, or bridge financing need, the team is ready to review your project and move quickly. Visit Gannlending to submit your loan scenario and get a same-day response.

FAQ

What is a mixed-use hard money loan?

A mixed-use hard money loan is a short-term privately funded loan secured by a property combining two or more use types, such as retail and residential. Approval is based on asset value and exit strategy, not borrower credit.

How fast can a hard money loan close for a mixed-use project?

Hard money loans close in as few as 3–10 business days when documentation is complete. Established borrowers with ready files close even faster.

What loan-to-value ratio do hard money lenders offer on mixed-use properties?

Most hard money lenders offer LTV ratios up to 75–80% of the property's after-repair value. Developer equity contributions of 20–25% of total project cost are standard.

What are the biggest risks of using hard money for mixed-use development?

The primary risks include higher interest costs, short loan terms that pressure cash flow, and lease-up delays that push back your refinance timeline. Contingency reserves and a clear exit strategy are the standard mitigations.

When should a developer refinance out of a hard money loan?

Developers should target refinancing once stabilized occupancy reaches 85–95%, which is the threshold most conventional commercial lenders require to underwrite permanent financing on a mixed-use property.