A short sale is a lender-approved voluntary sale of your home for less than the outstanding mortgage balance, while foreclosure is a legal process where the lender seizes and sells your property due to missed payments. The difference between foreclosure and short sale comes down to three things: who controls the process, how badly your credit suffers, and what debt you carry afterward. Understanding these distinctions can save you years of financial recovery time. The Fair Credit Reporting Act governs how both events appear on your credit report, and state anti-deficiency laws determine whether your lender can sue you for the remaining balance after either process.

How do foreclosure and short sale affect your credit and future homebuying?

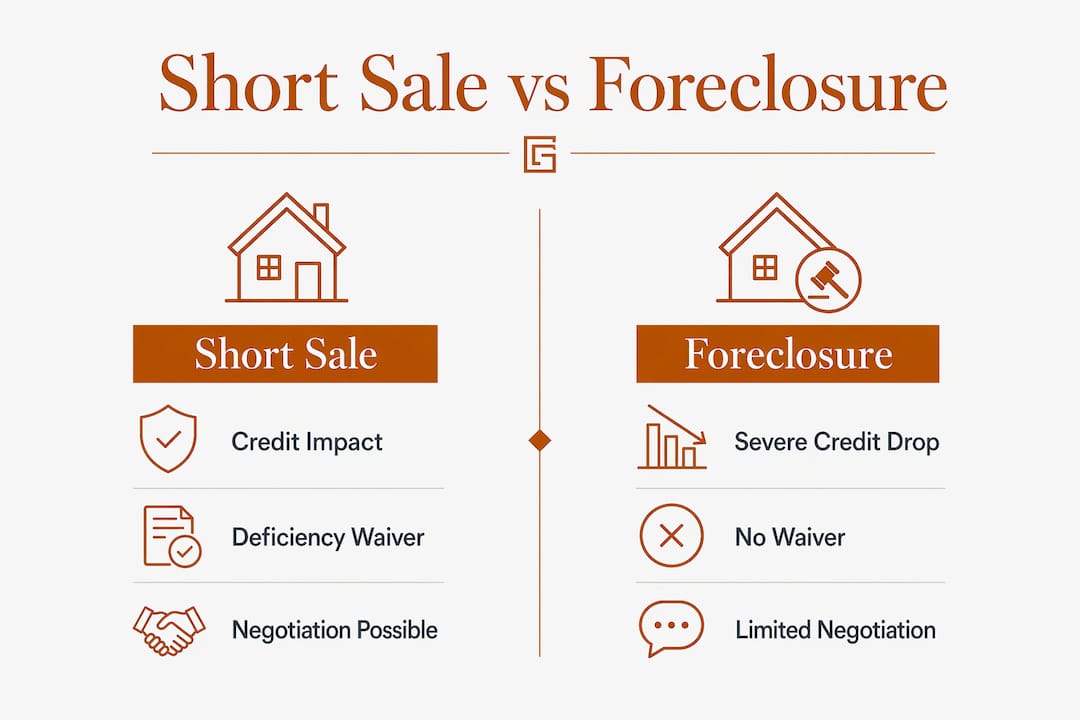

The credit damage from foreclosure is significantly worse than from a short sale. A short sale drops your score by 50–150 points, while a foreclosure causes a drop of 85–300 points depending on your starting credit profile. That gap matters because it determines how quickly you can qualify for a mortgage again.

Homeownership after foreclosure requires a much longer wait. Conventional mortgage eligibility returns in 2–4 years after a short sale but takes approximately 7 years after a foreclosure. That is a difference of three to five years of renting instead of building equity.

Foreclosure also shows up differently on background checks. Lenders, landlords, and employers who run public record searches will see a foreclosure as a court judgment, which carries more weight than a short sale notation. A short sale may appear as "settled for less than owed" on your credit file, which is less alarming to future creditors than a full foreclosure entry.

| Category | Short Sale | Foreclosure |

|---|---|---|

| Credit score drop | 50–150 points | 85–300 points |

| Conventional mortgage wait | 2–4 years | ~7 years |

| Public record visibility | Limited | Court judgment on record |

| Homeowner control | High | None |

Pro Tip: If your credit score is already low before either process, a foreclosure can push you into subprime territory for nearly a decade. A short sale preserves more of your credit floor and gives you a faster path back to conventional financing.

What are the financial risks of deficiency judgments after each option?

A deficiency balance is the gap between what your home sells for and what you still owe the lender. Both short sales and foreclosures can leave you on the hook for this amount, but the risk level differs significantly between the two.

In a short sale, you have the opportunity to negotiate. Securing a written deficiency waiver in your short sale approval letter is the single most important legal protection you can get. Without it, your lender retains the right to sue you for the remaining balance after the sale closes. With it, that debt is extinguished permanently.

Foreclosure offers no such negotiation window. Once the lender takes the property and sells it at auction, they can pursue you for the deficiency in most states without any prior agreement. State laws vary significantly here. California's Code of Civil Procedure §580e, for example, prohibits deficiency judgments after short sales on one-to-four unit residential properties, but that protection does not automatically extend to foreclosure deficiencies.

Second liens complicate both processes. If you have a home equity line of credit or a second mortgage, that lienholder must also agree to the short sale terms. A second lienholder who refuses to release their lien can kill the entire short sale, pushing you toward foreclosure by default.

| Risk Factor | Short Sale | Foreclosure |

|---|---|---|

| Deficiency waiver available | Yes, negotiated upfront | Rarely, no negotiation |

| State law protections | Varies, often stronger | Varies, often weaker |

| Second lien complications | Must negotiate separately | Lender handles, less control |

| Post-sale debt risk | Low with written waiver | High without state protection |

Pro Tip: Never accept a short sale approval letter without reading the deficiency language word for word. If the letter does not explicitly waive the deficiency, ask your attorney to request an amended approval before you sign anything.

What does the short sale process look like compared to foreclosure?

The short sale process is homeowner-initiated and requires active participation. Foreclosure is lender-driven and gives you almost no say once it begins. That distinction shapes every step of each timeline.

A short sale follows this general sequence:

- Verify your equity position. Confirm your home's current market value against your loan payoff amount. Positive equity homeowners may qualify for a traditional sale and avoid loss mitigation entirely.

- Contact your lender's loss mitigation department. Request short sale consideration before you miss payments if possible. Early communication improves approval odds.

- Assemble your financial package. This includes tax returns, bank statements, pay stubs, a hardship letter, and a comparative market analysis. Incomplete documentation is the leading cause of short sale delays and denials.

- List the property and accept an offer. Your lender must approve the buyer's offer, not just you. This review period typically runs 30–90 days.

- Submit electronically. Electronic submission generates a verifiable timestamp and proof of delivery, reducing the risk of lost paperwork and disputes.

- Receive written approval with deficiency waiver. Do not proceed to closing without this document in hand.

Foreclosure follows a legal timeline set by state statute. After a defined number of missed payments, your lender files a notice of default. A notice of sale is then issued, and the property goes to auction on a court-set date. You have little ability to influence the timeline, the buyer, or the sale price once this process begins.

Why do lenders prefer short sales over foreclosures?

Lenders lose less money on short sales than on foreclosures, which is why they approve them. Foreclosure costs lenders through legal fees, property maintenance, insurance, and extended timelines that can stretch 12–18 months or longer. Those costs add up before the property even reaches auction.

The sale price difference reinforces this preference. Foreclosure auctions recover only 60–75% of a property's market value, while short sales typically achieve 85–95%. That 10–35 percentage point gap represents real money the lender recovers by cooperating with you instead of taking the property.

The practical advantages of a short sale for homeowners include:

- Control over timing. You choose when to list and can coordinate your move around the sale.

- Buyer selection. You and your agent select the buyer, which means you can avoid lowball offers that hurt the lender's recovery.

- Potential relocation assistance. Some lenders offer cash for keys programs in short sales to incentivize a smooth transition.

- Less stress. A voluntary, negotiated process gives you agency. Foreclosure strips that away entirely.

- Better lender relationship. Cooperating with your lender's loss mitigation team often results in more favorable terms than going silent and forcing them to foreclose.

Pro Tip: Call your lender's loss mitigation department before you miss a payment if you can. Lenders are far more willing to approve a short sale from a borrower who communicates proactively than from one who has already defaulted without contact.

What steps protect you legally and financially during this process?

Taking the right steps before and during either process protects you from consequences that can follow you for years. Skipping any of these can cost you far more than the home itself.

- Verify your equity first. Get a current market valuation before assuming you need a short sale or foreclosure. A traditional sale may be viable and far cleaner.

- Understand your state's laws. Anti-deficiency statutes vary by state. California, Arizona, and several other states offer stronger protections than others. Know which laws apply to your property before you agree to anything.

- Get the deficiency waiver in writing. A verbal assurance from a lender representative means nothing. The short sale approval letter must explicitly state that the deficiency is waived.

- Do not walk away without legal counsel. Abandoning a property without completing either a short sale or a formal foreclosure can leave you liable for HOA fees, property taxes, and code violations even after you stop living there.

- Consult a HUD-approved housing counselor. The U.S. Department of Housing and Urban Development certifies free counselors who can review your options without a financial conflict of interest.

- Explore emergency refinancing options early. In some cases, a fast refinance or bridge loan can resolve the distress before either process becomes necessary.

Pro Tip: Keep copies of every document you submit to your lender, every email, and every phone call log with date and time. If a dispute arises later, your paper trail is your only defense.

Key Takeaways

A short sale preserves more credit, eliminates deficiency risk through a written waiver, and gives homeowners control that foreclosure permanently removes.

| Point | Details |

|---|---|

| Credit score damage | Short sales drop scores 50–150 points; foreclosures drop 85–300 points. |

| Mortgage waiting period | Short sale allows new mortgage in 2–4 years; foreclosure requires ~7 years. |

| Deficiency waiver | Always secure a written deficiency waiver in the short sale approval letter. |

| Lender recovery rates | Short sales recover 85–95% of market value; foreclosure auctions recover 60–75%. |

| Documentation completeness | Incomplete financial packages are the top reason short sales fail or stall. |

What I've learned from watching homeowners navigate these two paths

Most homeowners I've seen go through this process make the same mistake: they wait too long. They miss two or three payments, feel embarrassed, and avoid calling their lender. By the time they reach out, the foreclosure clock is already running and their options have narrowed.

The homeowners who come out of this in the best shape are the ones who treat it like a negotiation, not a surrender. They call the loss mitigation department early. They get a real estate attorney to review the approval letter before closing. They submit their financial package electronically with every document the lender asks for, and then some.

A short sale is not always possible. If your lender refuses, if a second lienholder won't cooperate, or if market conditions make the math unworkable, foreclosure may be unavoidable. But in my experience, most homeowners who end up in foreclosure could have qualified for a short sale if they had started the process 60–90 days earlier.

The other thing worth saying plainly: a short sale is not a failure. It is a structured exit that protects your credit, eliminates your debt, and lets you move forward. Foreclosure is a legal action taken against you. The difference in how those two things feel, and how they appear on your record, is significant.

If you are facing distress right now, read about selling to avoid foreclosure before you decide anything. The information you gather in the next two weeks will shape the next seven years of your financial life.

— Brian

Gannlending can help you move fast when time is short

When foreclosure is approaching and you need options quickly, speed matters more than almost anything else. Gannlending specializes in hard money loans that close in as few as 5–7 business days, with financing up to 75% LTV on residential and commercial properties. No appraisal is required, and the approval process focuses on the asset rather than mountains of paperwork.

Gannlending has funded over $50 million in real estate transactions and works directly with investors and homeowners who need fast, reliable capital to protect their properties. If a short sale, refinance, or fast acquisition is part of your exit strategy, explore your options with a lender built for exactly this kind of situation.

FAQ

What is the main difference between a short sale and foreclosure?

A short sale is a voluntary, lender-approved sale of your home for less than the mortgage balance. Foreclosure is an involuntary legal process where the lender takes possession of your property after missed payments.

How long does a short sale take to complete?

The lender review period for a short sale typically runs 30–90 days after you submit a complete financial package and an accepted buyer offer. Total timeline from listing to closing often runs 3–6 months.

Can a lender still sue me after a short sale?

Yes, unless your short sale approval letter includes an explicit written deficiency waiver. Without that waiver, the lender retains the right to pursue the remaining balance after the sale.

Is buying a short sale a good deal for buyers?

Buying a short sale can offer below-market pricing, but the process is slower and more uncertain than a traditional purchase because the lender must approve the sale price and terms.

Which is worse for your credit, a short sale or a foreclosure?

Foreclosure causes significantly more credit damage, dropping scores by 85–300 points versus 50–150 points for a short sale, and it extends the wait for a new conventional mortgage to approximately 7 years.