A notice of sale is a legally required document that officially announces the date, time, and location of a foreclosure property auction. It marks the final stage before a lender can sell a property to recover an unpaid debt. The timeframe between issuance and auction typically ranges from 21 to 90 days, depending on state law. Understanding this notice is not just reassuring. It is the first step toward doing something about it before the auction clock runs out.

What is a notice of sale in foreclosure?

A notice of sale is the formal public announcement that a lender has scheduled a property for auction after a borrower has failed to cure a default. The industry also refers to it as a "Notice of Trustee's Sale" in non-judicial states or a "Notice of Sheriff's Sale" in judicial foreclosure states. Both terms describe the same legal trigger: the lender's right to sell the property has been activated. This document is distinct from the earlier notice of default, which simply records that a borrower has fallen behind. The notice of sale moves the process from warning to final disposition.

The notice of sale activates the lender's power of sale clause written into the mortgage or deed of trust. Courts strictly enforce state timelines governing this notice to protect procedural fairness for all parties. Once issued, the property's status changes in public records, which limits refinancing options and alerts creditors and lienholders. That public record change is not a formality. It signals to every financial institution that the property is in distress.

What must a notice of sale include?

A valid notice of sale must contain specific information, and missing even one element can invalidate the entire document. State statutes define these requirements precisely, and courts enforce them without flexibility.

Every legally compliant notice of sale must include:

- Names of all relevant parties: The borrower, the lender or trustee, and any co-borrowers must be identified by full legal name.

- Complete legal property description: The street address alone is not sufficient. The legal description from the deed must appear verbatim.

- Current default amount: The exact dollar amount owed, including principal, interest, and fees, must be stated.

- Exact date, time, and location of the auction: Vague references are not acceptable. The notice must name the specific courthouse, trustee office, or public venue.

- Terms of sale: Some states require minimum bid disclosures or payment terms for the winning bidder.

Omissions or errors in any of these fields can render the notice invalid. That gives homeowners a legal basis to challenge or stop the sale entirely. Courts have vacated foreclosure sales based on a single incorrect date or a missing party name.

Pro Tip: Request a copy of the notice of sale from your county recorder's office and compare every field against your original loan documents. Errors are more common than most homeowners realize.

How is a notice of sale delivered and publicized?

State and federal rules require lenders to use multiple simultaneous delivery channels. A single mailed letter is never enough. The goal is to ensure that the borrower, the public, and all interested parties receive actual notice before the auction occurs.

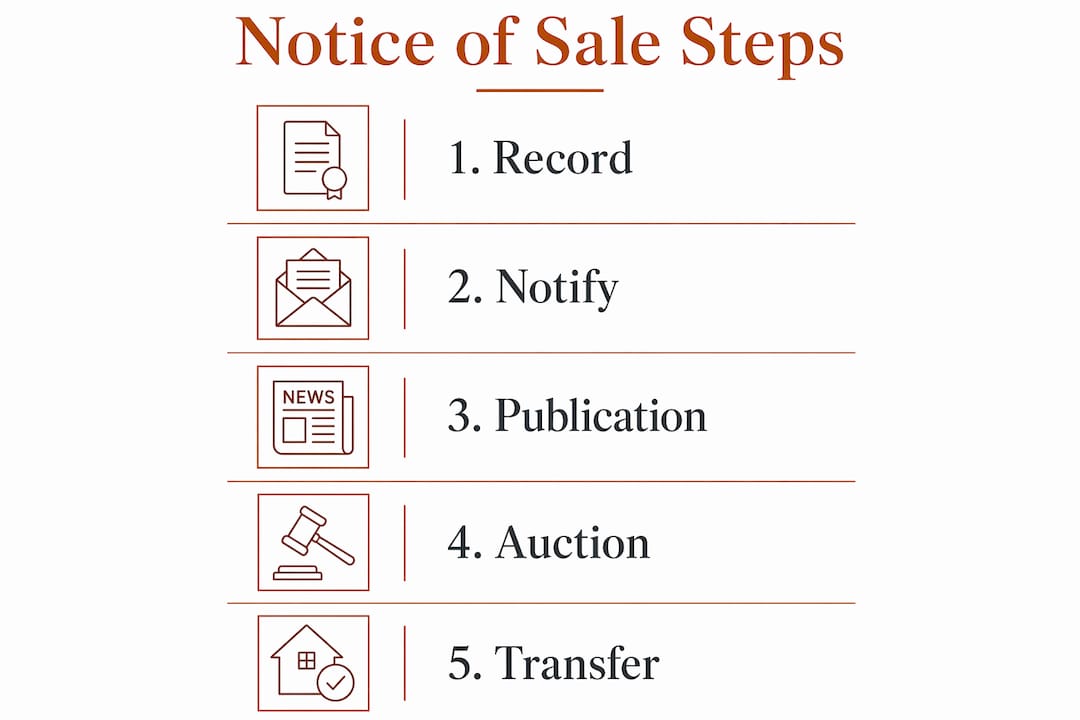

The standard delivery process follows these steps:

- Certified mail to the borrower: The lender must send the notice by certified mail to the borrower's last known address. This creates a documented record of delivery.

- Newspaper publication: Publication typically occurs once a week for three consecutive weeks in a local newspaper of general circulation. No sale can occur before this published notice period expires, and courts can vacate early sales.

- Physical posting on the property: The notice must be posted in a visible location on the property itself, usually on the front door.

- Posting at public venues: Most states require posting at the courthouse door or another designated public building.

- Recording with the county clerk or recorder: The notice must be filed with the county recorder's office to become part of the official public record.

For federally related mortgages, the last newspaper publication must fall between 4 and 12 days before the sale date. That narrow window is a federal requirement, not a suggestion. Missing it forces the lender to restart the entire notice timeline.

| Delivery method | Who it notifies | Timing requirement |

|---|---|---|

| Certified mail | Borrower directly | Sent at time of filing |

| Newspaper publication | General public | 3 consecutive weeks |

| Property posting | Neighbors and occupants | Before sale date |

| County recorder filing | Creditors and lienholders | At time of issuance |

Pro Tip: Check your county recorder's website to confirm the notice was filed on the correct date. If the filing date does not align with the mailing date, that discrepancy may be grounds for a legal challenge.

How does a notice of sale fit into the foreclosure timeline?

Foreclosure follows a defined sequence, and the notice of sale sits near the end of that sequence. Understanding where it falls helps homeowners recognize exactly how much time remains.

The standard foreclosure progression looks like this:

- Missed payments: The process begins after a borrower misses one or more mortgage payments, typically triggering lender contact after 30 days.

- Notice of default: After 90 to 120 days of missed payments in most states, the lender records a notice of default. This is the formal start of foreclosure proceedings.

- Cure period: Most states give borrowers a statutory window after the notice of default to bring the loan current before the next step.

- Notice of sale: Once the cure period expires without resolution, the lender issues the notice of sale and schedules the auction.

- Public auction: The property sells to the highest bidder at the scheduled auction, or the lender takes title if no qualifying bid is received.

Judicial foreclosures require court approval at each stage, which extends the overall timeline significantly. Non-judicial foreclosures, permitted in states like California, Texas, and Arizona, move faster because the lender exercises the power of sale clause without court involvement. The transition from notice of default to notice of sale shifts lender power dramatically under state timelines that courts strictly enforce.

After the notice of sale is recorded, the property's public record status changes immediately. This affects any attempt to refinance, sell, or place new liens on the property. Other creditors receive constructive notice through the public filing, which can trigger additional claims against the property. Understanding the sheriff sale process that follows gives buyers and homeowners a clearer picture of what the auction itself involves.

What options do homeowners have after receiving a notice of sale?

Receiving a notice of sale does not mean the property is already lost. Legal experts confirm that receipt of a notice of sale doesn't mean inevitable loss. Legal and financial tools to delay or stop the sale remain available, but time is short.

- Pay the reinstatement amount: Many states allow homeowners to stop the foreclosure by paying only the past due amounts, interest, and legal fees rather than the entire loan balance. Homeowners often confuse the total payoff amount with the reinstatement amount, and that confusion costs them their homes unnecessarily.

- Negotiate a loan workout: Contact the lender directly to request a forbearance agreement, loan modification, or repayment plan. Lenders often prefer this over the cost and delay of a full auction.

- Sell the property before the auction: A pre-auction sale can pay off the mortgage, preserve the homeowner's credit, and potentially return equity. Reviewing a guide to selling before foreclosure outlines the specific steps and timing required.

- Pursue a short sale: If the property is worth less than the outstanding balance, a lender may approve a short sale. This requires lender consent but avoids the public auction record.

- Challenge procedural defects: Minor procedural errors in delivering the notice of sale, such as improper posting timing or failure to record, can legally void a foreclosure sale. An attorney can review the notice for defects that create grounds to vacate or delay the sale.

The notice of sale is the "concrete sign" the foreclosure has moved to final disposition. Homeowners who ignore this stage frequently miss last-minute opportunities that were still available to them.

Pro Tip: Contact a HUD-approved housing counselor immediately after receiving a notice of sale. These counselors provide free advice and can help you identify reinstatement options your lender may not volunteer.

Key Takeaways

A notice of sale is the legally binding announcement of a foreclosure auction, and procedural errors in its delivery can void the entire sale.

| Point | Details |

|---|---|

| Definition and timing | A notice of sale schedules a foreclosure auction, with 21–90 days between issuance and sale date. |

| Required content | The notice must name all parties, describe the property legally, state the default amount, and specify the auction details. |

| Delivery channels | Lenders must use certified mail, newspaper publication, property posting, and county recording simultaneously. |

| Homeowner options | Reinstatement, loan workouts, pre-auction sales, and procedural challenges can all stop or delay the auction. |

| Reinstatement vs. payoff | Most states allow stopping the sale by paying arrears and fees only, not the full loan balance. |

What most people get wrong about a notice of sale

The most damaging misconception I see is that a notice of sale is the end of the road. It isn't. The notice is a deadline, not a verdict. Every stage of the foreclosure process carries procedural requirements, and the notice of sale stage carries more of them than any other. Lenders must restart the entire timeline if they miss a single filing date or skip a required publication week. That is real leverage for a homeowner who knows where to look.

The second thing people miss is the reinstatement distinction. I have watched homeowners walk away from properties they could have kept because they assumed they needed to pay off the entire mortgage to stop the auction. In most states, you only need to cover the arrears, fees, and interest. That is a very different number, and it is often within reach.

The third issue is timing. The window between notice of sale and auction is short, typically 21 to 90 days. Waiting even two weeks to consult an attorney or housing counselor can eliminate options that were available on day one. The notice of sale is not a document to set aside and revisit later. It is a countdown that started the moment it was recorded.

— Brian

Private lending options when foreclosure is on the line

Facing a notice of sale creates pressure that traditional bank timelines simply cannot accommodate. Banks take 30 to 60 days to process loan applications. That pace doesn't work when an auction date is already on the calendar.

Gannlending provides hard money loans that close in as few as 5–7 business days, with financing up to 75% LTV on residential and commercial properties. The approval process focuses on the asset, not paperwork, which matters when time is the constraint. Gannlending has funded over $50 million in real estate transactions, including situations where homeowners needed fast capital to reinstate a loan or close a sale before the auction date. If a notice of sale has already been issued, speed is the only variable that still matters.

FAQ

What is the difference between a notice of default and a notice of sale?

A notice of default records that a borrower has fallen behind on payments and formally starts the foreclosure process. A notice of sale comes later and announces the specific date, time, and location of the public auction.

Can a homeowner stop a foreclosure after a notice of sale is issued?

Yes. Homeowners can stop the sale by paying the reinstatement amount, negotiating a loan workout, selling the property, or challenging procedural defects in the notice. Time is limited, typically 21 to 90 days from issuance.

What makes a notice of sale legally invalid?

Errors in required content, such as a wrong party name, incorrect property description, or missed publication deadline, can invalidate the notice. Courts have vacated foreclosure sales based on a single procedural defect.

How long does a lender have to wait before holding the auction?

State law governs the waiting period, which typically ranges from 21 to 90 days after the notice of sale is issued. For federally related mortgages, the final newspaper publication must occur between 4 and 12 days before the sale date.

Does a notice of sale affect a homeowner's ability to refinance?

Yes. Once the notice of sale is recorded with the county, the property's public record status changes. That filing signals financial distress to lenders and makes refinancing significantly harder to secure before the auction date.