Private financing for multi-unit rental properties is defined as capital sourced from non-bank lenders, including private individuals, family offices, and asset-based lending firms, rather than conventional mortgage institutions. When you need to finance multi-unit rental property privately, you gain access to faster closings, negotiable terms, and qualification standards that focus on the property's income rather than your personal tax returns. The three most common instruments are private money loans, DSCR loans, and hard money loans. Each serves a different investor profile, and choosing the wrong one costs you time, money, and deals.

What are the main private financing options for multi-unit rental properties?

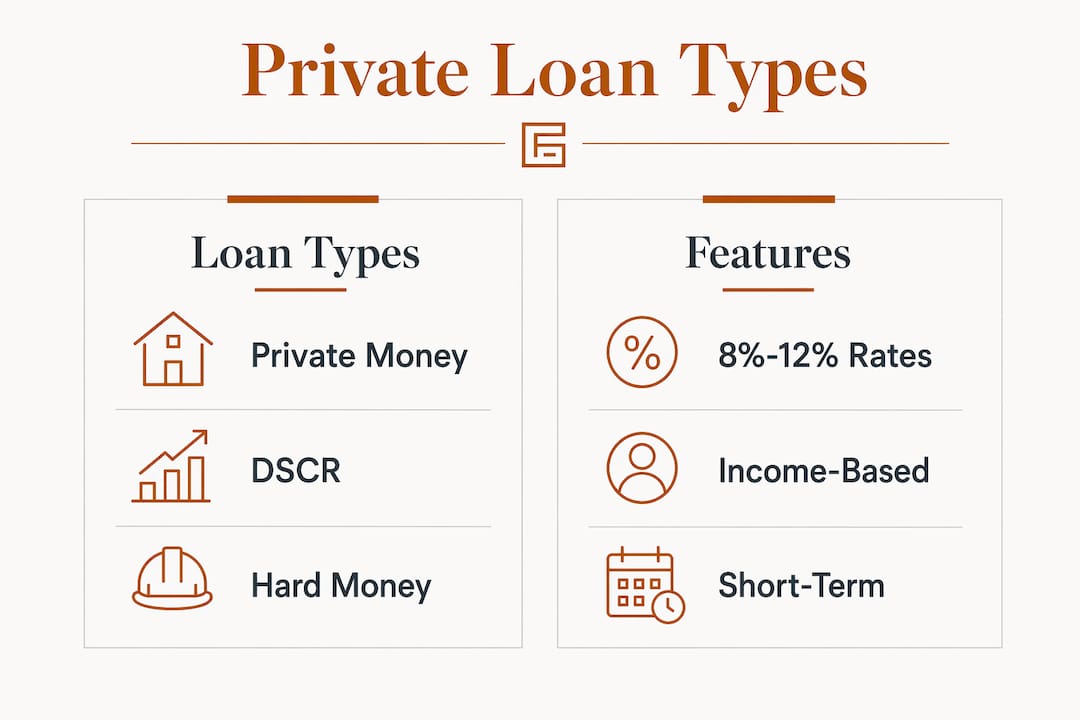

Private financing is not a single product. It is a category of capital with meaningfully different structures depending on your deal, your credit, and your timeline.

Private money loans

Private money loans come from high-net-worth individuals seeking returns better than certificates of deposit or bonds. These lenders charge 8%–12% interest with points varying by deal and relationship. Loan terms typically run 6–24 months, though some extend to 5–10 years with balloon payments. The qualification bar is relationship-driven rather than formula-driven, which gives experienced investors real room to negotiate.

DSCR loans

Debt Service Coverage Ratio loans qualify you based on the property's income, not your W-2 or tax returns. Most DSCR lenders require a 660+ FICO score and cap loan-to-value at 75%–80%. Interest rates typically land between 7%–9% with 30-year amortization. A minimum DSCR of 1.0–1.25 is standard, meaning the property must generate at least as much income as it costs to service the debt. DSCR loans are increasingly popular for self-employed investors who cannot easily document personal income.

Hard money loans

Hard money loans are short-term, asset-based products designed for speed and flexibility. Rates run 10%–14%, and these loans close in days rather than weeks. They work best for acquisitions where you need to move fast, or for rehab projects where a property does not yet qualify for income-based underwriting. The higher cost is the price of speed and access.

| Loan Type | Typical Rate | Down Payment | Best Use Case |

|---|---|---|---|

| Private money loan | 8%–12% | 10%–35% | Relationship-based deals, flexible terms |

| DSCR loan | 7%–9% | 20%–25% | Income-producing rentals, self-employed investors |

| Hard money loan | 10%–14% | 25%–35% | Fast acquisitions, rehab projects |

Once a property reaches five or more units, underwriting shifts to commercial standards. Lenders then focus on NOI and DSCR rather than personal income, and down payments typically rise to 25%–35%.

What prerequisites and documentation do you need to qualify?

Qualifying for private financing on a multi-unit property requires preparation across three areas: your financial profile, the property's financials, and your legal documentation.

Your financial profile. DSCR lenders require a 660+ credit score, while private money lenders vary by deal and relationship. Conventional investment loans typically require a 620–680+ credit score with 15%–25% down. The stronger your credit and cash reserves, the better the rate you negotiate.

The property's financials. You need a current appraisal and a clear Net Operating Income calculation. NOI equals gross rental income minus operating expenses, before debt service. Lenders use NOI to calculate DSCR, so any errors in your income or expense figures directly affect your approval and rate.

Legal documentation. Every private loan requires a promissory note, a mortgage or deed of trust, and proof of insurance. Legal expenses for these documents typically run $500–$1,500 per loan. Proper contracts protect both parties and prevent disputes that can derail a deal months after closing.

- Pull your credit report and resolve any errors before approaching lenders.

- Prepare a full rent roll showing current leases, monthly rents, and vacancy history.

- Calculate NOI using actual trailing 12-month income and expense data.

- Order a property appraisal from a licensed appraiser familiar with multi-family assets.

- Retain a real estate attorney to draft or review the promissory note and deed of trust.

Pro Tip: If your DSCR falls below 1.0, increase your down payment to reduce the debt load rather than chasing a higher-rate private money loan. A larger equity position often unlocks better terms across all loan types.

How do you find and build relationships with private lenders?

Private lenders rarely respond to cold calls. The most effective path to securing private funding is consistent, relationship-based networking over time.

The best places to find private lenders include:

- REIA meetings. Real Estate Investor Association chapters attract both active investors and passive capital providers looking for deal flow.

- Professional associations. Attorneys, CPAs, and financial advisors often know clients with capital to deploy in real estate.

- Family offices. High-net-worth families managing their own capital frequently allocate a portion to private real estate loans for yield.

- Online investor communities. Platforms and forums focused on multi-family investing surface both deal partners and private capital sources.

When you pitch a deal, lead with the numbers. Show the property address, purchase price, your equity contribution, projected NOI, and your exit plan. Private lenders are individuals seeking returns, not institutions running automated underwriting. They invest in people as much as properties.

Maintaining the relationship after funding matters as much as winning the first deal. Make every payment on time. Send brief monthly updates on occupancy and any capital improvements. Lenders who trust you will fund your next deal faster and on better terms.

Pro Tip: Bring a one-page deal summary to every networking event. Investors who can articulate their deal in 60 seconds and hand over a clean summary close private funding far faster than those who rely on verbal pitches alone.

Step-by-step process for securing private financing on a multi-unit property

A clear process prevents the most common mistakes and keeps your deal moving from offer to close.

- Define your investment plan. Know your target property type, price range, and hold period before you approach any lender. Lenders read confidence in how well you know your own deal.

- Assess your capital and property financials. Calculate NOI and DSCR for the target property. If DSCR exceeds 1.25, a DSCR loan is likely your most cost-effective path. If you need to close in under two weeks, private money or hard money is the right tool.

- Choose your financing type. Match the loan type to your primary constraint. Documentation issues favor DSCR loans. Speed needs favor private or hard money. Liquidity problems may point toward a bridge loan as a short-term solution.

- Prepare your documentation package. Compile your credit report, rent roll, NOI statement, appraisal, and entity documents if purchasing through an LLC. Present this as a professional package, not a collection of emails.

- Submit and negotiate. Private lenders negotiate. Push back on points if your equity contribution is strong. A lower rate with higher points may cost more than a higher rate with no points, depending on your hold period.

- Close and manage the relationship. Private money financing closes in fewer than 7 business days in many cases, compared to 30–60 days for traditional commercial loans. Use that speed as a competitive advantage when making offers.

| Step | Key Action | Common Mistake |

|---|---|---|

| Define your plan | Set hold period and target returns | Approaching lenders without a clear exit |

| Assess financials | Calculate NOI and DSCR accurately | Using projected rather than actual income |

| Choose loan type | Match loan to your primary constraint | Defaulting to hard money when DSCR qualifies |

| Prepare documents | Compile a professional package | Submitting incomplete or inconsistent data |

| Negotiate terms | Push back on points and fees | Accepting the first term sheet without review |

| Close and manage | Communicate proactively post-close | Going silent until the next deal |

Experienced investors stack financing sources across their portfolio, using conventional loans for early properties, DSCR to scale, and private or hard money for quick closes or rehab deals. This approach to portfolio financing strategies keeps capital moving without over-relying on any single lender type.

What are the common pitfalls when financing multi-unit rentals privately?

The most expensive mistakes in private financing are not the ones investors expect. They are the ones hiding in the fine print.

- Underestimating total loan cost. A 9% interest loan with 1 point may cost less overall than an 8% loan with 3 points, depending on how long you hold the property. Use mortgage cost calculators to compare true all-in costs before signing.

- Ignoring documentation rigor. Skipping proper legal contracts to save $1,000 in attorney fees can cost tens of thousands in disputes. Every private loan needs a promissory note and deed of trust.

- Failing to communicate with lenders. Private lenders are people. Silence signals trouble. Regular updates build the trust that gets you funded again.

- Having no exit strategy. Private and hard money loans are short-term by design. Know before you close whether your exit is a refinance, a sale, or a DSCR loan conversion.

"Calculating all-in loan costs, including interest, points, and fees, is the single most important step investors skip. The cheapest-looking rate is rarely the cheapest loan."

What I've learned about private financing after years in the field

The investors who consistently win at private financing share one trait: they treat lenders like long-term partners, not one-time transactions. That sounds obvious, but most investors only call their private lender when they need money. The ones who send deal updates, share market observations, and check in between deals get the first call when a lender has capital to deploy.

I have also seen investors destroy their margins by fixating on the interest rate while ignoring points and fees. A deal that looks profitable at 9% can bleed cash at 9% plus 3 points if your hold period is short. Run the full cost calculation every time, not just the rate.

The other thing most articles will not tell you: your first private loan is the hardest. After that, your track record does the selling. Pay on time, communicate clearly, and deliver what you projected. That behavior compounds faster than any interest rate.

Private financing for multi-unit rentals is not a shortcut. It is a tool. Used with discipline and transparency, it gives you the speed and flexibility that traditional lenders simply cannot match. The investors who treat it that way build portfolios. The ones who treat it as easy money usually learn an expensive lesson.

— Brian

Fast private lending for your next multi-unit rental deal

Gannlending funds multi-unit rental property acquisitions and refinances in as few as 5–7 business days, with no appraisal requirement and financing up to 75% LTV. The approval process focuses on the asset, not a stack of personal financial documents.

Gannlending has funded over $50 million in real estate loans, working with investors who need capital that moves as fast as their deals. Whether you are acquiring a new property or protecting one from foreclosure, private lending options at Gannlending are built around your timeline and your deal, not a bank's underwriting calendar.

Key Takeaways

Private financing for multi-unit rental properties works best when investors match the loan type to their primary constraint, whether that is speed, documentation, or cost.

| Point | Details |

|---|---|

| Match loan to your constraint | Use DSCR for documentation issues, hard money for speed, private money for flexibility. |

| Know your total loan cost | Compare interest plus points across options; the lowest rate is not always the cheapest loan. |

| Build lender relationships | Consistent communication and on-time payments unlock faster funding on future deals. |

| Prepare complete documentation | Every private loan needs a promissory note, deed of trust, and current property financials. |

| Stack financing sources | Combine DSCR, private money, and hard money across your portfolio to keep capital moving. |

FAQ

What credit score do I need for private financing on a multi-unit property?

DSCR loans typically require a 660+ FICO score, while private money lenders vary based on the deal and relationship. Stronger credit unlocks better rates across all private loan types.

How fast can I close with private financing?

Private money and hard money loans close in fewer than 7 business days in many cases. That speed contrasts sharply with the 30–60 days typical for traditional commercial loans.

What is a DSCR loan and how does it qualify me?

A DSCR loan qualifies you based on the property's income rather than your personal income. Most lenders require a minimum DSCR of 1.0–1.25, meaning the property's income must cover its debt payments.

How much do I need to put down for a private loan on a multi-unit rental?

Down payments range from 10%–35% depending on the loan type and lender. Commercial properties with five or more units typically require 25%–35% down under private financing terms.

What documents do I need to apply for a private real estate loan?

You need a promissory note, mortgage or deed of trust, proof of insurance, a current rent roll, and an NOI statement. Legal documentation costs typically run $500–$1,500 per loan.