A rental property loan is a mortgage designed to finance real estate you plan to rent to tenants rather than occupy yourself. The industry also calls these investment property loans or, in some markets, buy-to-let mortgages. Understanding the difference between this product and a standard home loan shapes every decision you make as an investor, from the down payment you save to the lender you choose.

What is a rental property loan, and how does it work?

A rental property loan is a mortgage issued for properties intended purely to generate rental income, not for the borrower's personal residence. Lenders treat these loans as higher risk because a vacant unit or a difficult tenant can interrupt payments. That risk shapes every term: the rate, the down payment, and the documentation required.

The core mechanics mirror a standard mortgage. You borrow a lump sum, secure it against the property, and repay principal plus interest over an agreed term. What changes is the lender's scrutiny. Agencies like Fannie Mae and Freddie Mac set conforming loan standards that most conventional lenders follow, and those standards are noticeably stricter for investment properties than for owner-occupied homes.

Rental income itself factors into the equation. Lenders count up to 75% of projected rental income when calculating your qualifying income. That 25% haircut accounts for vacancies, repairs, and management costs. Knowing this figure before you apply tells you exactly how much rental revenue you need to support the loan.

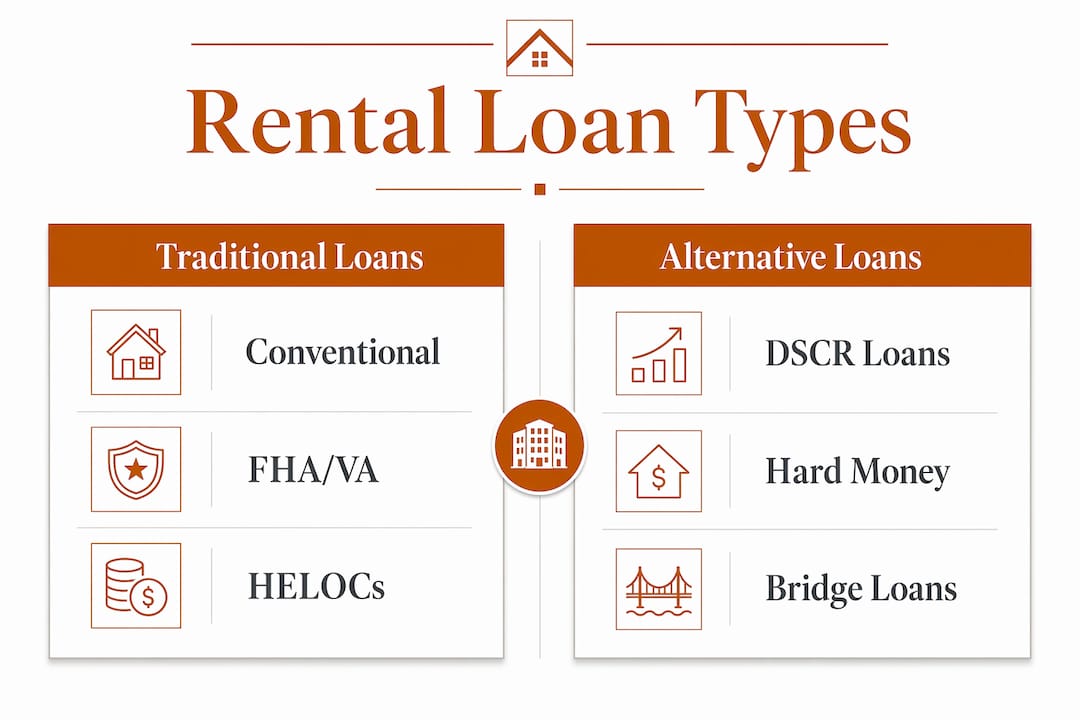

What financing options are available for rental property loans?

Rental property financing options span a wide range, from government-backed programs to private asset-based lending. Each type suits a different investor profile and deal structure.

Conventional mortgages follow Fannie Mae and Freddie Mac guidelines. Conventional loans require credit scores of 680–700+ and down payments of 15–25%. They offer competitive long-term rates and work best for investors with strong W-2 income and clean credit files.

DSCR loans (Debt Service Coverage Ratio loans) qualify you based on the property's cash flow rather than your personal income. Typical DSCR requirements range from 1.1 to 1.25, meaning the property's gross rent must cover 110–125% of the monthly mortgage payment. DSCR loans accept credit scores as low as 620 and suit investors who are self-employed or already carry multiple mortgages.

Hard money and bridge loans are asset-based products that close fast. Typical rates run 8–12%, and funding can happen in 5–10 days. The speed matters more than the rate when you are competing for a property in a tight market. Read more about securing bridge financing before you need it, not after.

FHA and VA loans open the door through house hacking. You buy a two-to-four-unit property, live in one unit, and rent the others. FHA loans require as little as 3.5% down, and VA loans require zero down for eligible veterans. The rental income from the other units can offset your mortgage payment immediately.

HELOCs and home equity loans let you tap equity in a property you already own. These options preserve your first mortgage rate while pulling cash for a down payment or renovation on a new acquisition. They work well for investors who have built equity but want to avoid refinancing a low-rate primary mortgage.

| Loan type | Min. credit score | Down payment | Best for |

|---|---|---|---|

| Conventional mortgage | 680–700 | 15–25% | Strong W-2 borrowers |

| DSCR loan | 620 | 20–25% | Self-employed or portfolio investors |

| Hard money / bridge | Flexible | Varies by LTV | Fast acquisitions, fix-and-flip |

| FHA (house hack) | 580 | 3.5% | First-time investors |

| VA (house hack) | Varies | 0% | Eligible veterans |

| HELOC / home equity | 620+ | N/A (uses existing equity) | Investors with built-up equity |

Pro Tip: Match the loan type to your exit strategy first, then worry about the rate. A 10% hard money loan that closes in seven days beats a 7% conventional loan that takes 45 days when the seller has competing cash offers on the table.

What are the requirements for a rental property loan?

Qualifying for an investment property loan is more demanding than qualifying for a primary residence mortgage. Lenders apply stricter standards because the income stream depends on tenants, not your paycheck.

Credit score is the first filter. A score of 660 or higher clears most conventional lenders. DSCR and private lenders may accept 620, but the rate you receive will reflect the added risk. Improving your score before applying by 20–30 points can meaningfully lower your interest cost over a 30-year term.

Down payment requirements are firm. Rental property loans generally require 15–25% down. Lenders rarely waive this because the down payment is their first layer of loss protection. The only common exceptions are FHA and VA house-hack scenarios.

Income verification follows a dual track. Conventional lenders want W-2s, tax returns, and bank statements. They will also count up to 75% of projected or actual rental income from the subject property. DSCR lenders skip personal income entirely and focus on the rent-to-mortgage ratio instead.

Reserve requirements catch many investors off guard. Most lenders require 6–12 months of mortgage payments held in liquid accounts after closing. If you are financing multiple properties, each one may carry its own reserve requirement. That cash cannot be borrowed; it must be verifiable savings or investment account balances.

Common documentation lenders request:

- Two years of federal tax returns

- Two months of bank statements

- Lease agreements or market rent analysis for the subject property

- Schedule E from your tax return if you own other rentals

- Entity documents if you are purchasing through an LLC

Pro Tip: If you own rentals that show paper losses on Schedule E due to depreciation, ask your lender how they handle that before applying. Some lenders add depreciation back to your income; others do not. The difference can change your qualifying income by thousands of dollars.

How do rental property loans differ from primary residence mortgages?

The gap between investment property loans and owner-occupied mortgages is wider than most first-time investors expect. Four differences define the comparison.

- Higher interest rates. Rental loans carry rates 0.5–0.75% above primary residence loans for the same credit profile. On a $300,000 loan, that difference adds roughly $100–$150 per month to your payment.

- Larger down payments. Owner-occupied buyers can put down 3–5% with conventional financing. Investment property buyers start at 15% and often need 20–25% to get competitive rates.

- Stricter debt-to-income limits. Lenders apply tighter debt-to-income ratios and demand larger cash reserves because rental income is less predictable than a salary.

- Loan term flexibility. Rental property loan terms range from 15 to 40 years with fixed, adjustable, or interest-only structures. Primary residence loans rarely offer 40-year or interest-only terms at competitive rates.

These differences affect your cash flow math from day one. A higher rate and larger down payment mean your break-even rent is higher. Running the numbers before you make an offer, not after, protects you from buying a property that cannot cover its own costs.

What strategies can investors use to optimize rental property financing?

Experienced investors rarely rely on a single loan type. They mix financing methods based on deal speed, property condition, and portfolio stage.

House hacking with FHA or VA loans is the lowest-cost entry point. Buying a duplex or triplex, living in one unit, and renting the others lets you use owner-occupied loan terms on what is functionally an investment property. The rental income from the other units can cover most or all of your mortgage.

DSCR loans for portfolio scaling remove the income ceiling that stops many investors after two or three properties. Because qualification depends on the property's cash flow rather than your personal debt-to-income ratio, you can build your rental portfolio beyond the limits conventional lenders impose.

HELOCs as a funding source let you recycle equity from appreciated properties into new acquisitions without selling. You draw from the line, use it as a down payment, close on the new property, and repay the HELOC from rental cash flow over time.

Fixed vs. adjustable rate selection depends on your hold period. Fixed rates protect long-term buy-and-hold investors from rate increases. Adjustable-rate mortgages offer lower initial payments for investors who plan to refinance or sell within five to seven years.

Mixing short-term and long-term financing is a proven approach for value-add deals. Use a hard money loan to acquire and renovate a property quickly, then refinance into a 30-year fixed mortgage once the property is stabilized and appraised at its improved value. This strategy, called BRRRR (Buy, Rehab, Rent, Refinance, Repeat), lets you recycle capital across multiple deals. Explore short-term real estate loans to understand the full range of bridge and hard money structures available in 2026.

Pro Tip: Lock in a fixed rate when you plan to hold a property for more than seven years. Adjustable rates look attractive at origination, but a rate reset in year five can erase your cash flow margin on a property you intended to hold long-term.

Key Takeaways

A rental property loan is a distinct mortgage product with stricter terms than owner-occupied financing, and matching the right loan type to your deal structure determines whether an investment generates cash flow or drains it.

| Point | Details |

|---|---|

| Definition matters | Rental property loans are investment mortgages with higher rates and down payments than owner-occupied loans. |

| Loan types vary widely | Conventional, DSCR, hard money, FHA, VA, and HELOC options each suit different investor profiles and timelines. |

| Qualification is stricter | Lenders require 660+ credit scores, 15–25% down, and 6–12 months of cash reserves in most cases. |

| Rental income counts | Lenders apply up to 75% of projected rental income toward your qualifying income, improving approval odds. |

| Strategy beats rate | Mixing loan types across a portfolio, such as hard money for acquisition and conventional for stabilization, maximizes returns. |

What I have learned about picking the right rental loan

After watching investors make the same financing mistakes repeatedly, the pattern is clear: most people shop for the lowest rate instead of the right structure. A 6.5% conventional loan sounds better than a 10% hard money loan until you realize the conventional loan takes 50 days to close and the seller accepted a competing offer on day 30.

The second mistake is underestimating reserves. Lenders require them, but investors also need them operationally. A roof replacement, an HVAC failure, or a three-month vacancy can wipe out a year of cash flow if you close with nothing left in the account. I have seen investors qualify on paper and then struggle through their first year because they treated reserves as a closing requirement rather than a real financial buffer.

DSCR loans changed the game for self-employed investors and portfolio builders. The ability to qualify on property cash flow rather than personal income removes a ceiling that stops many investors after their second or third property. If you are self-employed or your tax returns show heavy deductions, a DSCR loan deserves serious consideration before you assume conventional financing is your only path.

The investors who scale successfully treat financing as a tool, not a hurdle. They understand each loan type, know when to use each one, and build relationships with lenders before they need capital. That preparation is what separates investors who close deals from those who lose them.

— Brian

Gannlending: fast financing for rental property investors

Real estate deals do not wait for slow approvals. Gannlending provides hard money loans that close in as few as 5–7 business days, with financing up to 75% LTV across residential and commercial properties. No appraisal delays. No mountains of paperwork. The focus is on the asset, not your tax returns.

Gannlending has funded over $50 million for real estate investors who needed speed and certainty. Whether you are acquiring a rental property, expanding a portfolio, or protecting a property from foreclosure, Gannlending structures financing around your deal. Contact Gannlending directly to discuss your next rental property acquisition and get a prequalification decision fast.

FAQ

What is a rental property loan?

A rental property loan is a mortgage used to purchase real estate you intend to rent to tenants rather than live in yourself. Lenders apply stricter credit, down payment, and reserve requirements than they do for owner-occupied home loans.

What credit score do I need for a rental property loan?

Most conventional lenders require a credit score of 660 or higher for investment property loans. DSCR and private lenders may approve borrowers with scores as low as 620, though the interest rate will be higher.

How much do I need to put down on a rental property?

Rental property loans typically require a down payment of 15–25%. The main exceptions are FHA and VA house-hack purchases, where down payments can be as low as 3.5% or zero for eligible veterans.

Can rental income help me qualify for a loan?

Yes. Most lenders count up to 75% of projected or actual rental income from the subject property toward your qualifying income. That 25% reduction accounts for vacancies and operating expenses.

What is a DSCR loan and who should use it?

A DSCR loan qualifies borrowers based on the property's rental income covering the mortgage payment rather than personal income. It suits self-employed investors and portfolio builders who face conventional income limits after acquiring multiple properties.