After Repair Value (ARV) is defined as the projected market value of a property after all planned renovations are complete. Every serious fix-and-flip decision, rehab budget, and hard money loan approval runs through this single number. Get it right and you protect your profit margin. Get it wrong and you can lose money on a deal that looked solid on paper. This guide explains ARV meaning in real estate, how to calculate it accurately, and how it drives financing decisions in 2026.

What is ARV in real estate and why does it matter?

ARV is the foundation of profitable fix-and-flip projects, guiding every subsequent decision from your initial offer to your exit strategy. It is not what a property is worth today. It is what the property will be worth once renovations match the quality and condition of comparable sold homes in the same area.

Lenders, investors, and appraisers all rely on ARV for different reasons. Hard money lenders use ARV to set maximum loan amounts, not the current as-is value. Investors use ARV to calculate their maximum allowable offer and renovation budget. Property owners use ARV to decide whether a renovation project pencils out before spending a dollar on materials.

ARV sits at the center of every major investment calculation. Without a reliable ARV, you are pricing deals on guesswork. Tools like Deal Run and Flip Analyzer Pro help investors build ARV estimates faster, but the underlying method is the same regardless of the platform you use.

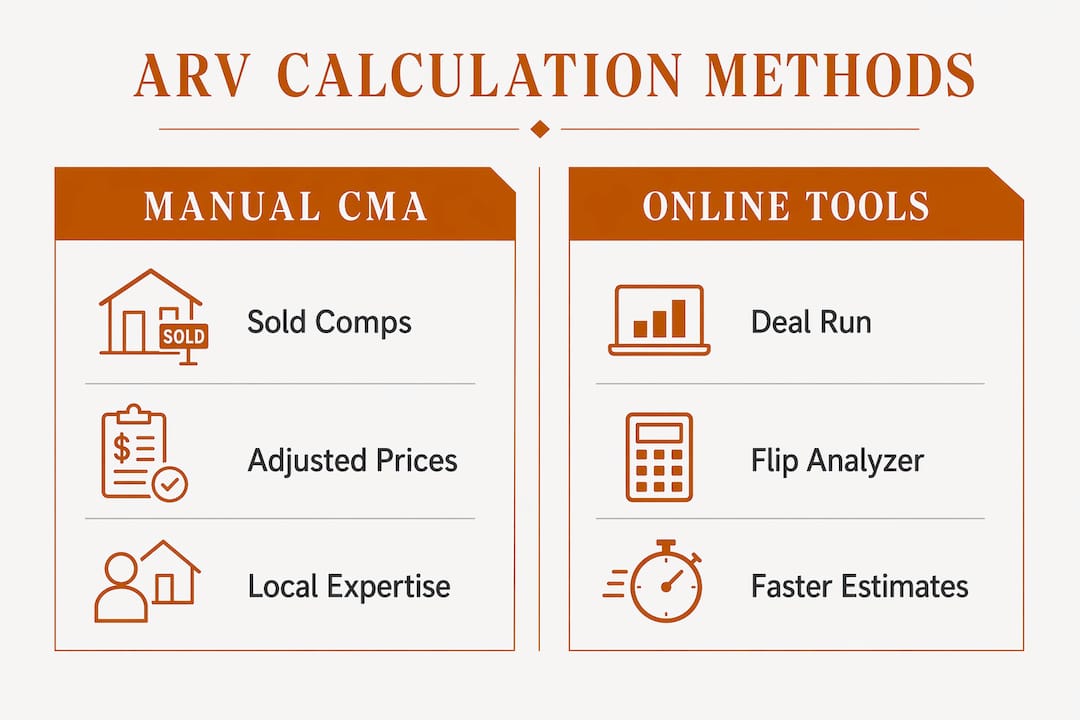

How to calculate ARV using comparable sales

Calculating ARV accurately requires a comparable sales analysis, often called a CMA (Comparative Market Analysis). The process is methodical and the quality of your output depends entirely on the quality of your inputs.

Follow these steps:

- Identify 3–5 recent sold properties. Select recent, nearby comps within a 0.5–1 mile radius that sold within the last 90 days. Properties sold more than 90 days ago may not reflect current market conditions.

- Match the finished condition. Comps must reflect the intended finished condition of your property, not its current state. A renovated 3-bedroom home should be compared to other renovated 3-bedroom homes, not distressed ones.

- Adjust for differences. No two properties are identical. Adjust each comp's sale price up or down for differences in square footage, lot size, bedroom count, bathroom count, garage, and renovation quality. A standard adjustment for a full bathroom, for example, is typically a few thousand dollars depending on the market.

- Average the adjusted values. Once you have adjusted each comp, calculate a simple or weighted average. That figure is your ARV estimate.

- Apply a safety buffer. Subtract a 5% margin from your ARV to account for appraisal gaps, market shifts, or slower seasonal sales.

Pro Tip: Never use active listings as comps. Only sold properties represent what buyers actually paid. Active listings are asking prices, not market reality.

The manual CMA method produces the most defensible ARV. Online tools like Deal Run and Flip Analyzer Pro can speed up the process, but they still require you to input and validate the comps manually. Automated shortcuts without human review introduce error.

ARV vs market value: what is the real difference?

ARV and current market value measure the same asset at different points in time. Current market value is what a buyer would pay for the property today, in its present condition. ARV is what a buyer would pay after renovations are complete and the property matches the quality of comparable finished homes.

Automated Valuation Models (AVMs) like Zillow's Zestimate add another layer of confusion. AVMs do not account for planned renovations or the condition of comparable properties. A Zestimate reflects current market data, not the future value of a renovated asset. Relying on a Zestimate for ARV calculation is one of the most common and costly mistakes new investors make.

The differences matter in practice:

- Current market value reflects the as-is condition and is used for traditional purchase transactions.

- ARV reflects the post-renovation condition and is used for investment underwriting, rehab loans, and exit strategy planning.

- Tax assessed value is set by local government and often lags market conditions by one to three years. It has no reliable relationship to ARV.

- AVM estimates aggregate recent sales data but ignore renovation scope, condition adjustments, and comp selection criteria.

For investors, ARV in property valuation is the only number that matters when evaluating a deal. Tax assessments and AVMs are useful for general reference, but neither can replace a properly conducted comparable sales analysis.

Common pitfalls that destroy ARV accuracy

Most bad deals trace back to a flawed ARV estimate. The mistakes are predictable, and knowing them in advance protects your capital.

- Confusing renovation cost with value added. A $100,000 renovation budget does not guarantee a $100,000 increase in ARV. Market comparables set the ceiling on achievable value, not your spending. Spending $50,000 on a kitchen in a neighborhood where finished homes sell for $180,000 will not push your ARV to $230,000.

- Over-improving for the neighborhood. Renovation scope must align with market standards. Luxury finishes in a working-class neighborhood do not add proportional value. Buyers in that market will not pay for upgrades that exceed neighborhood norms.

- Using outdated or mismatched comps. Comps older than 90 days or located more than one mile away introduce significant error. A comp from a different school district or zip code may reflect a completely different buyer pool.

- Skipping the safety buffer. Ignoring the 5% deduction leaves no room for appraisal variability or market softening. Deals with zero margin fail when the appraisal comes in lower than expected.

- Relying solely on automated models. Poor data quality in AVMs can cause ARV estimates to vary by 10–20% compared to a manually validated analysis. That variance can turn a profitable deal into a loss.

Pro Tip: Validate your ARV estimate with a local real estate agent or licensed appraiser before committing to a purchase price. A second opinion from someone who knows the micro-market costs very little and can save tens of thousands of dollars.

Experienced investors also track why real estate deals fall through to identify patterns in their own ARV errors. Reviewing failed deals is one of the fastest ways to sharpen your estimation skills.

How ARV drives investment decisions, financing, and exit strategies

ARV is the input that powers every major investor calculation. Once you have a reliable ARV, the rest of the deal math follows a clear structure.

The 70% and 75% rules

The 70% rule states that an investor should pay no more than 70% of ARV minus estimated repair costs. The 75% rule applies the same logic at a slightly higher threshold, often used by investors with lower cost structures or in competitive markets. ARV is fundamental to both rules and determines the maximum allowable offer price.

For example: if ARV is $300,000 and repairs cost $50,000, the 70% rule sets your maximum offer at $160,000. Paying more than that compresses your profit margin below a level that justifies the risk.

ARV in hard money lending

Lenders base maximum loan amounts on ARV, not the current as-is value of the property. This is the defining feature of rehab and hard money loans. A lender offering 75% loan-to-value (LTV) on a property with a $300,000 ARV will lend up to $225,000, regardless of what the property is worth today. Understanding LTV ratios in real estate is the natural next step once you have a solid ARV in hand.

Renovation budget and profit calculation

| Metric | Formula | Example |

|---|---|---|

| Maximum offer (70% rule) | (ARV × 0.70) minus repair costs | ($300,000 × 0.70) minus $50,000 = $160,000 |

| Maximum offer (75% rule) | (ARV × 0.75) minus repair costs | ($300,000 × 0.75) minus $50,000 = $175,000 |

| Projected gross profit | ARV minus purchase price minus repair costs | $300,000 minus $160,000 minus $50,000 = $90,000 |

| Lender max loan (75% LTV) | ARV × 0.75 | $300,000 × 0.75 = $225,000 |

ARV also shapes exit strategy. Investors holding a property as a rental use ARV to determine refinance potential after renovation. A property that appraises at or above ARV after rehab allows the investor to pull equity out through a cash-out refinance and recycle capital into the next deal.

Key takeaways

ARV is the single most important number in any fix-and-flip or rehab deal, and every offer price, loan amount, and renovation budget should trace directly back to a defensible ARV estimate.

| Point | Details |

|---|---|

| ARV definition | ARV is the projected market value of a property after all planned renovations are complete. |

| Calculation method | Use 3–5 sold comps within 0.5–1 mile, adjust for condition and features, then average the results. |

| ARV vs AVMs | Zillow Zestimate and similar tools do not reflect planned renovations and should not be used for ARV. |

| Safety buffer | Subtract 5% from your ARV estimate to protect against appraisal gaps and market shifts. |

| Financing link | Hard money lenders base loan amounts on ARV, not as-is value, making accurate ARV critical for funding. |

Why I think most investors underestimate how market-driven ARV really is

The biggest misconception I see is that ARV is a renovation number. Investors spend weeks planning a kitchen remodel or a bathroom upgrade and then assume the ARV will reflect every dollar they put in. It does not work that way. The market sets the ceiling, not your contractor's invoice.

I have watched investors pour $80,000 into a property in a neighborhood where the best comparable sales topped out at $220,000. No amount of granite countertops or new HVAC changes what buyers in that zip code will pay. The ARV was $220,000 before the renovation started, and it was $220,000 after. The renovation just ate the profit.

The investors who get ARV right treat it as a market research exercise, not a math exercise. They spend time in the field, talk to local agents, and look at what buyers actually paid for finished homes in the last 60 days. They apply a conservative buffer and build their offer around that number. They also use tools like private loans for rental repairs to keep renovation costs from ballooning beyond what the market will support.

Conservative ARV estimates feel uncomfortable when you are competing for deals. But the investors who survive long enough to build real wealth are the ones who would rather lose a deal than overpay for one.

— Brian

Gannlending finances deals built on real ARV numbers

Real estate investors need a lender who understands ARV, not one who slows the deal down with appraisals and paperwork.

Gannlending is a hard money lender built specifically for fix-and-flip and rehab investors. Gannlending closes in as few as 5–7 business days and bases financing on ARV rather than the as-is condition of the property. With financing up to 75% LTV and over $50 million funded, Gannlending gives investors the speed and structure to act on deals before the competition does. If you have a solid ARV and a deal worth funding, apply for hard money financing and get a decision fast.

FAQ

What does ARV stand for in real estate?

ARV stands for After Repair Value. It is the estimated market value of a property after all planned renovations are complete.

How is ARV different from current market value?

Current market value reflects what a property is worth today in its present condition. ARV reflects what it will be worth after renovations match the quality of comparable finished homes in the area.

Can I use Zillow to calculate ARV?

Zillow's Zestimate does not account for planned renovations or comparable property condition, making it unreliable for ARV calculation. Use a manual comparable sales analysis with recently sold, fully renovated properties instead.

What is the 70% rule and how does ARV apply?

The 70% rule states that your maximum offer should be no more than 70% of ARV minus estimated repair costs. ARV is the anchor for this calculation and determines whether a deal is worth pursuing.

How do hard money lenders use ARV?

Hard money lenders set maximum loan amounts based on ARV rather than the as-is property value. A lender offering 75% LTV uses ARV as the base, which means a higher and more accurate ARV directly increases your available financing.