A title company is defined as a neutral third party that verifies legal ownership of a property and facilitates its secure transfer from seller to buyer. The role of title company in real estate goes far beyond paperwork. Title companies conduct title searches, manage escrow accounts, issue title insurance, and coordinate the entire closing process. For homebuyers and real estate investors alike, understanding how title companies work is the difference between a smooth closing and a costly legal dispute. This guide breaks down every function, cost, and consideration you need to know in 2026.

What does a title company do in real estate?

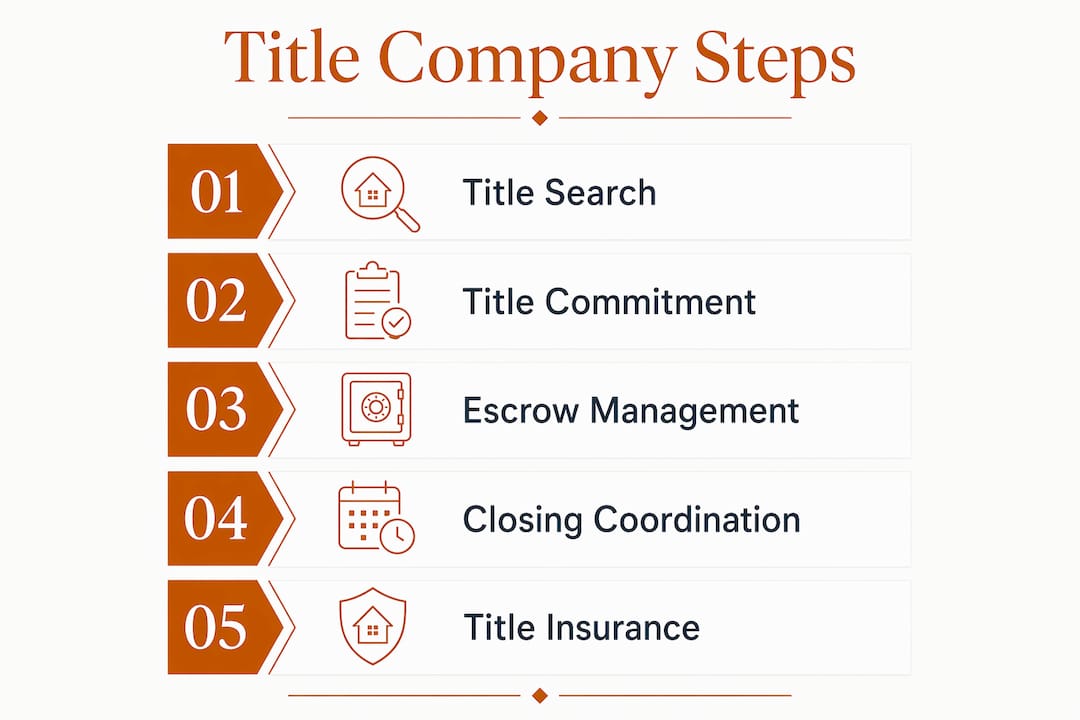

A title company performs five core functions: title search, escrow management, title commitment issuance, closing coordination, and post-closing recording. Each step protects the buyer, the lender, and the seller from ownership disputes that could surface years after the transaction.

The title search is the foundation. A title agent reviews public records going back decades to confirm the seller legally owns the property and that no outstanding liens, judgments, or claims exist against it. This search uncovers problems like unpaid contractor bills, unresolved divorces, or tax liens that would follow the new owner if left unchecked.

After the search, the title company issues a title commitment. This document lists any exceptions to coverage and gives all parties a clear picture of what the title insurance policy will and will not cover. Buyers and their attorneys should review this document carefully before closing.

Title companies act as neutral escrow agents holding all funds until every contract condition is satisfied. Escrow funds remain inaccessible to both buyer and seller until financing is confirmed and inspections are approved. That protection prevents either party from accessing money prematurely.

Pro Tip: Ask your title company for a copy of the title commitment at least five business days before closing. Reviewing exceptions early gives you time to resolve issues without delaying your closing date.

On closing day, the title company prepares and manages all documents, collects signatures, disburses funds to the seller, pays off existing liens, and sends the deed and mortgage to the county recorder. Even a small error in the disbursement schedule can delay county recording, leaving the property in legal limbo with unresolved liens after possession transfers. Accuracy at this stage is non-negotiable.

Title companies also function like project managers for transactions, coordinating lenders, real estate agents, attorneys, and buyers to keep every moving part on schedule. That coordination role is often underestimated but is one of the most valuable services they provide.

How does title insurance work and why does it matter?

Title insurance is a one-time premium paid at closing that provides retroactive protection against title defects existing before the purchase date. This is fundamentally different from homeowner's insurance or auto insurance, which protect against future events. Title insurance covers problems that already existed but were not discovered during the title search.

Two types of policies exist. The lender's policy protects the mortgage lender and is typically required by every bank or hard money lender. The owner's policy protects the buyer and is strongly recommended even when not required. Both policies are issued at closing and remain in force for as long as the insured party holds an interest in the property.

| Policy Type | Who It Protects | Required? | Coverage Basis |

|---|---|---|---|

| Lender's policy | Mortgage lender | Almost always required | Loan amount |

| Owner's policy | Buyer/investor | Recommended, not always required | Purchase price |

| Extended coverage | Investors, commercial buyers | Optional | Negotiated terms |

Costs vary by state and purchase price. Total title-related closing costs typically range from 0.67% to 1% of the purchase price. On a $150,000 transaction, that means $1,000–$1,500 in title fees. That figure is modest compared to the legal costs of defending an ownership dispute without coverage.

Understanding the difference between a title agent and a title underwriter matters here. The title agent performs research and manages the transaction, while the underwriting company assumes the actual insurance risk. This separation provides financial security. If the title agency closes or faces financial trouble, the underwriter still backs the policy. That distinction reassures buyers who worry about the long-term validity of their coverage.

Pro Tip: Most buyers receive their final owner's title insurance policy weeks or even months after closing. Store it permanently with your property records. Discarding the policy risks losing your evidence for claims against pre-existing defects discovered years later.

How do title company functions vary by state?

Title company authority and scope vary significantly across the United States. In about a dozen states, licensed real estate attorneys rather than title companies handle closings. Georgia, South Carolina, Massachusetts, and New York are examples of attorney-closing states. In these jurisdictions, buyers should anticipate additional attorney fees and procedural differences that affect both timing and cost.

| Closing Type | Who Manages Closing | Additional Costs | Common States |

|---|---|---|---|

| Title company closing | Title agent | Title fees only | Texas, Florida, California |

| Attorney closing | Real estate attorney | Attorney fees plus title fees | Georgia, New York, Massachusetts |

| Hybrid closing | Both title company and attorney | Varies | Some Midwest and Southeast states |

For real estate investors, these differences carry real consequences. An investor doing a double closing or an assignment in Georgia faces attorney requirements that add both time and cost compared to the same deal in Texas. Knowing your state's rules before you contract is part of sound deal underwriting.

Investors also encounter title-specific challenges that typical homebuyers do not. Assignment closings require the title company to handle simultaneous transfers between three parties. Double closings require two separate HUD-1 or ALTA settlement statements and two sets of recording fees. Not every title company has experience with these structures. Choosing one that does prevents delays at the worst possible moment.

Experienced title companies with strong communication are critical to resolving title "clouds" before settlement. A title cloud is any document, claim, or lien that creates uncertainty about ownership. Common examples include old mortgages never properly released, forged deeds in the chain of title, and boundary disputes. Resolving these issues requires both legal knowledge and proactive follow-through from your title team. For investors moving fast, a slow or inexperienced title company can kill a deal entirely. You can learn more about closing deals quickly in Gannlending's investor guide.

What should you look for when choosing a title company?

The right title company protects your investment. The wrong one costs you time, money, and sometimes the deal itself. Here is what to evaluate before you commit.

- Experience with your transaction type. A company that handles standard residential purchases may not know how to manage a simultaneous double closing or a short-sale with multiple lien holders. Ask directly whether they have closed deals like yours in the past 12 months.

- Licensing and underwriting partnerships. Verify the company holds a current state license and confirm which underwriters back their policies. Major underwriters include Fidelity National Title, First American Title, Old Republic National Title, and Stewart Title. A title agent backed by a financially strong underwriter provides more durable protection.

- Communication speed. The quality of communication often determines the smoothness of closing. If a title company takes two days to return a call during the contract phase, expect the same behavior when a problem surfaces three days before closing.

- Transparent fee schedules. Request an itemized fee estimate before signing. Compare title search fees, escrow fees, document preparation charges, and recording fees across two or three companies. Fees are negotiable in many states.

- Investor-friendly processes. For investors, look for title companies that offer fast funding coordination and understand lender requirements for hard money or private loans.

Pro Tip: Ask every title company you interview: "Have you handled a double closing in the past 90 days?" Their answer tells you immediately whether they are investor-ready or primarily a retail operation.

Red flags include vague answers about underwriting relationships, reluctance to provide itemized fee estimates, and staff who cannot explain the title commitment exceptions clearly. These signals predict problems at closing.

Key Takeaways

A title company is the legal and financial backbone of every real estate transaction, protecting buyers, lenders, and investors from ownership defects that standard due diligence alone cannot catch.

| Point | Details |

|---|---|

| Core title company functions | Title search, escrow management, title insurance issuance, closing coordination, and deed recording. |

| Title insurance cost | Total title-related costs typically range from 0.67% to 1% of the purchase price at closing. |

| Agent vs. underwriter | The title agent manages the deal; the underwriter backs the insurance policy for long-term security. |

| State variations matter | About a dozen states require attorneys to handle closings, adding fees and changing timelines. |

| Choosing wisely | Verify licensing, underwriter partnerships, and experience with your specific transaction type before committing. |

Why I think most buyers underestimate title companies

Most buyers treat the title company as a commodity. They accept whoever the real estate agent recommends, sign the documents, and move on. That approach works fine until it does not.

I have seen transactions fall apart two days before closing because a title company failed to catch an unreleased mortgage from 1987. I have also watched investors lose earnest money because their title company had never handled a double closing and froze when the second transaction hit. These are not rare edge cases. They are predictable outcomes of choosing a title company based on convenience rather than competence.

The separation between title agents and underwriters is something most buyers never think about. But it matters. If your agent's office closes down, your owner's policy is still valid because the underwriter, not the agent, carries the risk. That structural protection is built into the system, but only if you chose a company backed by a reputable underwriter like Fidelity National Title or First American Title.

My advice: treat title company selection the same way you treat lender selection. Interview at least two companies. Ask about their underwriting relationships. Request a sample title commitment so you can see how they present exceptions. And keep your owner's policy permanently. It is the one document that can save you from a six-figure legal battle over a defect that existed before you ever signed the purchase contract.

— Brian

How Gannlending supports your real estate deals

A smooth closing depends on two things working together: a competent title company and reliable financing that arrives on time. Gannlending provides hard money loans for investors with funding in as few as 5–7 business days, no appraisal required, and up to 75% LTV on residential and commercial properties. Gannlending has funded over $50 million in real estate transactions and understands exactly what title companies need from lenders to keep closings on schedule. Whether you are buying a fix-and-flip, closing a double deal, or protecting a property from foreclosure, Gannlending moves at the speed your deals require. Contact Gannlending today to discuss your next transaction.

FAQ

What is the main role of a title company in real estate?

A title company verifies legal ownership, conducts a title search for liens and claims, manages escrow funds, issues title insurance, and coordinates the closing process to ensure a secure property transfer.

How much does a title company charge at closing?

Total title-related closing costs typically range from 0.67% to 1% of the purchase price. On a $150,000 purchase, expect to pay between $1,000 and $1,500 in combined title fees.

Do I need both a lender's and an owner's title insurance policy?

The lender's policy is almost always required by your mortgage lender. The owner's policy is separate and protects your personal ownership interest. Buying both at closing is strongly recommended since the combined premium is significantly lower than purchasing them separately.

What is a title cloud and how does it affect closing?

A title cloud is any unresolved claim, lien, or document in the ownership history that creates uncertainty about who legally owns the property. Title clouds must be resolved before closing can proceed, which can delay or cancel a transaction if not caught early.

Do all states use title companies for real estate closings?

No. In about a dozen states, including Georgia, Massachusetts, and New York, licensed real estate attorneys are required to handle closings instead of or alongside title companies. This adds attorney fees and can change the closing timeline compared to title company-led states.